Constitutional right: sales tax on wholesale and retail trade services

The author, when he was the Partner in a professional accounting firm, was the motivator of the view that after the 18th Amendment to the Constitution there should be proper mechanism for the collection of Value Added Tax (VAT), which is called Sales Tax in Pakistan in the provinces.

Accordingly, over time, till 2025, a reasonable apparatus has emerged in all the Provinces and Islamabad Capital Territory for the collection of VAT on services. Furthermore, corrections have been made in the respective laws that whole input tax adjustment, wherever paid, against that tax is available. This means that Provinces are only entitled to tax the ‘value addition’ which represents services under the VAT regime. There is no confusion on this subject. However, the journey is not complete.

The Chairman of Pakistan People Party Bilawal Bhutto-Zardari in the commemorative gathering for Shaheed Benazir Bhutto in Larkana on December 27,2025 has made an important statement that the Sindh Government is ready to assist the Federal Government in the collection of taxes where there has been lack of success or failure in the past.

At the outset, the author is extremely happy that political leadership at that level is discussing real economic issues of the country instead of useless rhetoric. This shows the maturity of the political thought process in Pakistan.

As a person involved in tax practice for over forty (40) years and one who has been on the other side of the table would like to clarify certain points which in his view are extremely relevant for moving forward on this matter. The timing is also relevant as discussions are on for the next National Finance Commission (NFC) award.

Bilawal has rightly said that the right to tax wholesale and retail trade under VAT lies with the Provinces under the Constitution of Pakistan and what is presently being done is not entirely in line with the specific Article of the Constitution.

The Federal Legislative List of the Constitution states as under:

- Taxes on the sales and purchases of goods imported, exported, produced, manufactured or consumed, except sales tax on services

This leads to the question of classification of goods and services. In the present world this classification has by and large been standardised. The modern system of classification has been laid down in the Central Product Classification (CPC). The United Nations’ Central Product Classification (CPC) is a global standard system for categorizing all goods and services, providing a framework for collecting and comparing economic data like production, trade, and national accounts, closely linked with ISIC (International Standard Industrial Classification) and HS (Harmonized System) to cover all outputs of economic activity and ensure consistent statistics.

Division 61 and 62 of CPC states as under:

Division 61 Wholesale trade services

611 Wholesale trade services, except on a fee or contract basis This group includes:

- services of wholesalers that purchase goods in large quantities and sell them to other businesses, sometimes after breaking bulk and repacking the product into smaller packages

612 Wholesale trade services on a fee or contract basis This group includes:

- services of commission agents, commodity brokers and auctioneers and all other types of traders who negotiate wholesale commercial transactions between buyers and sellers for a fee or a commission services of electronic wholesale agents and brokers services of wholesale auctioning houses

Division 62 Retail trade services

621 Non-specialized store retail trade services This group includes:

- retail sales services of non-specialized stores, such as supermarkets and department stores that carry a wide range of goods, new or second-hand, that are displayed on racks or shelves for the customer to make their own choice and carry up to the cashier to make payment services of retail auctioning houses

622 Specialized store retail trade services

This group includes: - retail sales services of specialized stores that carry a narrow range of related new or second-hand goods and where assistance is often provided to the customer by the sales staff or owner of the store

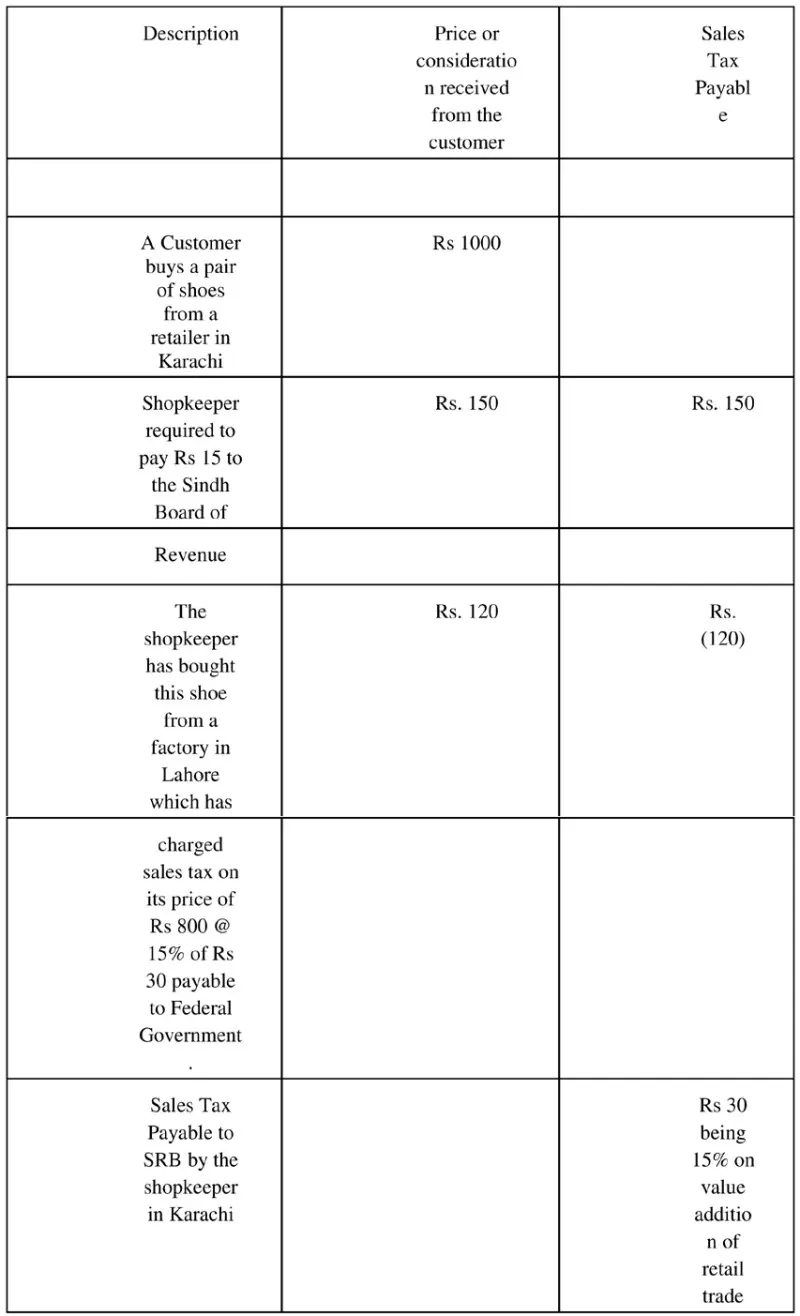

Wholesale and retail trade services are services not goods. The classification for VAT purposes has to be done under a method where the full credit is available for input against the output tax payable. When retail and wholesale trade are taxable as services then whole credit is available to input tax paid either to the Federal Government on goods acquired or to the Provincial Government services procured. This means that the jurisdiction having right to tax collection VAT on retail or wholesale trade is entitled to recover tax only on value addition being its earning on its services. This can only be done when all inputs are allowed. This can be illustrated as under:

Under the Constitution the Sindh Government has the right to receive Rs 30 as Sales Tax on Services. This is their direct right. Furthermore, they are also entitled to share under the NFC of the Federal Sales Tax recovered of Rs 120 under the formula agreed under NFC. For the shopkeeper the authority constitutionally entitled to receive VAT is SRB, not FBR.

In order to cater for this principle an important change has occurred in this respect in the Sindh Sales Tax Act, 2011. By the Sindh Finance Act 2025 the whole VAT regime on services has been revamped. SRB has rightly adopted CPC under the law. Now all classifications under CPC are applicable. If it is so then SRB has the right to tax those persons who are engaged in wholesale and retail in the Province of Sindh. There is no caveat in that. However, keeping in view the legacy of FBR, Sindh Sales Tax Act,

2011 by way of Entry 2 and 3 of the First Schedule has exempted wholesale and retail trade from Provincial Sales Tax Act, 2011. This is a concession provided to the Federal Government; otherwise, legally SRB’s jurisdiction exists to the extent of value addition in Sindh.

In this regard, it is important to consider that the Federal Sales Tax Act, 1990 is not based on negative lists concept; and under correct application its ambit is restricted to goods. If the correct and internationally-accepted practice, as also noted by CPC for wholesale and retail trade, are taken then there can be valid questions regarding the Federal Government’s right to recover sales tax on wholesale and retail trade services as identified above.

In the light of above it is suggested that:

a. The exemption from levy of Sales Tax on Services under the Sindh Sales Tax Act, 2011 be removed and all retailers and wholesalers be subjected to Sindh Sales Tax Act, 2011;

b. The jurisdiction of Federal Sales Tax Act, 1990 on such wholesalers and retailers be finished and their registration be transferred to the Provinces;

c. All input taxes, wherever paid are to be allowed without any restriction;

d. There is a general threshold of exemption under the Sindh Sales Tax on Services Act, 2011 as under which can be appropriately revised:

The exemption shall be available to the services provided by a person whose total annual turnover does not exceed rupees four million in a financial year.

e. The whole system at the Provincial level is undertaken through IT.

f. These principles be adopted in other Provinces also.

Whatever has been stated may look completely different from what has been done for the last seventy five (75) years. However, the author after a detailed review of laws, practices and constitutional position is firm in his view that this is the only practical way to handle the subject if Pakistan really wants reforms in the taxation system and adheres to a constitutional framework. This is the part of the 18th Amendment which has not yet been completed. The economic significance of this picture can be easily identified when there is a calculation of taxes collected from retail and wholesale trade, which is depicted at around 25% of GDP of the country.

Copyright Business Recorder, 2025

Comments

Comments are closed for this article.