Complexity in law: the sectoral and transactional maze

The complexities are not limited to administration; they are deeply embedded in the tax law itself. The system has morphed from one based on universal income to a sectoral and transactional tax maze.

Consider the simple question a foreign client posed: “What is the income tax applicable on the service sector in Pakistan?”

A simple answer is impossible. The response requires a series of qualifying questions:

• Is the service rendered from outside or within Pakistan?

• Is the service provider a tax resident of a country with a Double Taxation Treaty (DTT)?

• If rendered within Pakistan, is it through an individual/sole proprietor, Partnership or a corporate person?

• If corporate person whether through a branch office or a local subsidiary?

• What is the nature of the service?

• What is the status of the recipient (e.g., are they a withholding agent which in itself is a series of qualifying questions in certain cases)?

Depending on the answers, the tax regime could involve different DTT rates (e.g. 10 percent, 12 percent, 15 percent), varying withholding rates (e.g., 4 percent, 6 percent, 8 percent, 15 percent), and different rates for non-corporates (based on slab rates) and corporate tax rates (for small vs. regular companies) besides having minimum tax on annual turnover and Alternative Corporate Tax based on accounting profits.

Simplification of Pakistan’s income tax system—I

There are various kinds of minimum taxes whilst some of which can be carried forward, some are not adjustable. In the end, a taxpayer’s liability is computed under various such basis, and he has to pay the highest of all amounts.

This was just one example within the services sector. If one keenly observes the provisions and structure of income tax law, it is clear that the system is so complex that each economic or business sector has its own specific provisions.

Some of these were perhaps aimed at providing incentives (such as builders, developers, IT exports, etc.), whilst others were necessary due to economic considerations or specialized nature of businesses (e.g. banking, insurance, oil exploration, etc.)

However, all these fixes have resulted in a situation where there is no single income tax regime. Instead, there are various regimes, and the income tax incidence and compliances vary significantly depending upon the business, the type of entity, and the business segment one is operating in.

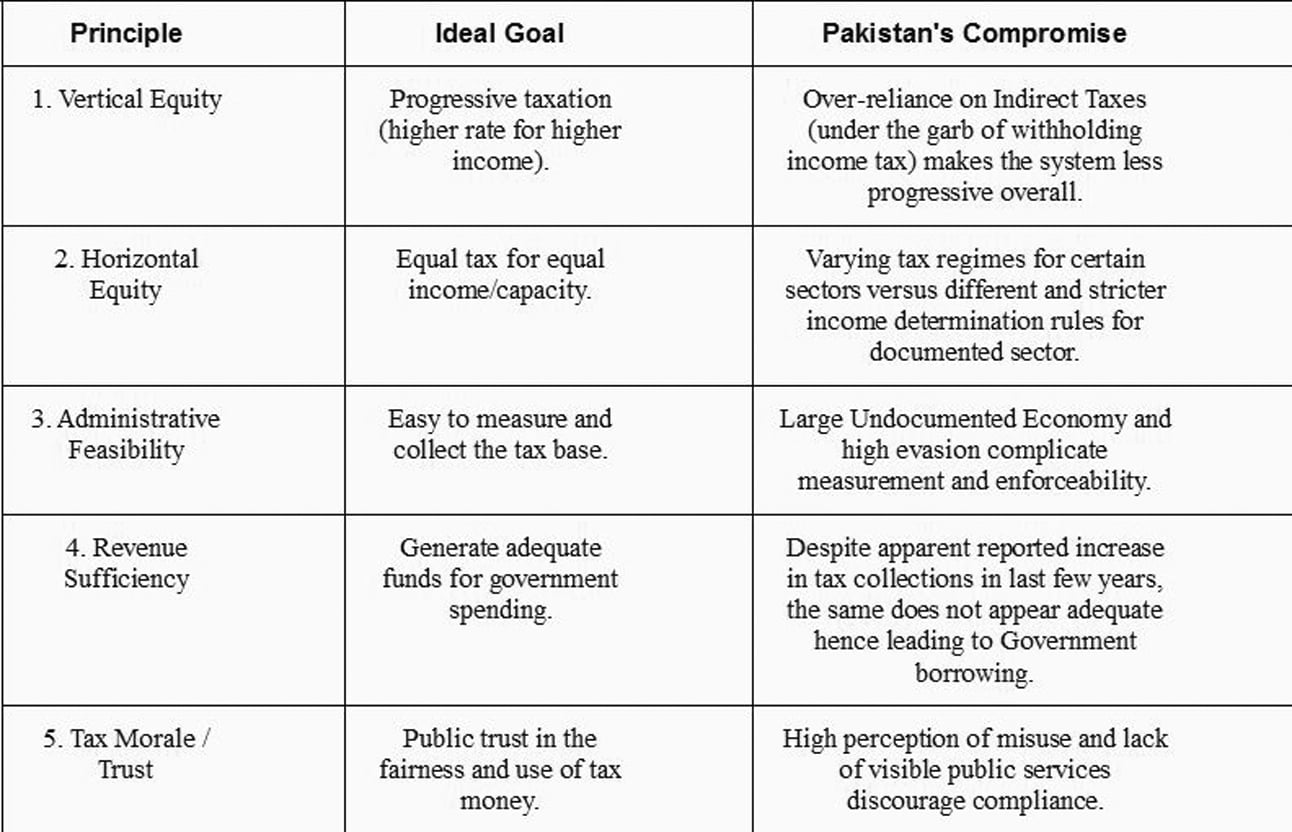

The erosion of core tax principles

This complex, sector-specific system completely compromises the fundamental principles that define a fair direct tax like income tax:

The true purpose of income tax, i.e., to ensure a fair contribution from those who can afford it, has been replaced by a singular focus: not to compromise on annual tax collection targets. The system has become a de facto indirect tax where withholding taxes (often on a minimum tax basis) are merely factored into the cost of goods and services and ultimately passed on to the customer.

In fact, in certain cases, withholding taxes are collected from people who may not eventually be liable to pay income tax (due to below or no taxable income) and hence there is never a claim for an adjustment or refund, e.g., taxes collected on telephone bills and internet users, transactions carried out through credit or debit cards, cash withdrawals, functions and gatherings, etc.

Needless to say, filing a refund claim can lead to a lengthy and complex process, often leaving taxpayers feeling stuck and uncertain about the outcome.

Beyond the law: the principle of exchange fairness

Ultimately, the sustainability of any tax system hinges on the tax morale of its citizens. Tax compliance is not just a legal obligation; it is a social contract based on the principle of Exchange Fairness, the quid pro quo between the taxpayer and the State.

For voluntary compliance to flourish, the documented taxpayer must perceive a tangible return on their contribution. Taxation for the State is about collection, but for the taxpayer, it is about delivery.

Ensuring that the State efficiently delivers its duties in terms of providing high-quality public goods, security, infrastructure, and basic services (particularly to the underprivileged classes) is as vital to tax revenue growth as drafting a perfect law. If the taxpayer sees his hard-earned contribution failing to translate into better public services or redistribution of wealth, no amount of legal complexity or punitive enforcement can guarantee lasting compliance.

The roadmap: back to basics and fair resolution

With the above background, the challenge for the proposed IMF-mandated simplification strategy is immense. The roadmap for true simplification and long-term economic stability must involve:

-

Drastic reduction in withholding tax provisions: Move away from hundreds of different rates and classifications to a few, broad categories.

-

Abolishing the minimum tax regime: Revert to the core principle of taxing actual income, not gross turnover or value of imports, etc. thereby restoring the principle of Ability to Pay.

-

Clearly delineating administrative powers: Enforce the Universal Self-Assessment and comprehensive Audit model by removing the power of direct amendment and multiple proceedings, ending the endless procedural debates.

-

Fundamental reform of Tax Dispute Resolution (TDR): The appellate system must be made effective and fair:

o Effective use of Alternate Dispute Resolution (ADR): For interpretational or classification issues before lengthy litigation.

o Ensuring independence: Of initial appellate forums to reduce the automatic reliance on higher courts.

o Tax specialist benches: Establishing specialist benches in higher courts to decide tax specific cases quickly and efficiently.

Conclusion: beyond the law – building a fiscal ecosystem

Whilst the outlined measures represent the necessary procedural steps, simplification is not just about writing shorter laws. It is about restoring the integrity and fairness of the system so that the purpose of income tax aligns once again with the universally accepted principles of a direct tax.

However, legal simplification cannot work in a vacuum. The political economy of taxation in Pakistan reveals that the law is often a reflection of underlying structural imbalances. A truly simplified code will remain ineffective if it is overlaid upon a massive undocumented economy that escapes the net, forcing the State to continually burden the documented sector with ad-hoc, complex measures to meet revenue targets.

True simplification requires a whole-of-ecosystem approach. The State must move beyond tactical revenue-raising and adopt a clear, long-term tax policy anchored to sustainable economic principles. This shift requires both parties to act in unison under a renewed social contract:

• For the State: Reform must evolve into a strategic pillar of economic management. This means providing a stable, predictable environment that incentivizes formalization and ensures the accountable utilization of public funds — the essence of Exchange Fairness.

• For the taxpayer: The reciprocal obligation is one of unconditional compliance. The taxpayer must recognize that a fair, transparent, and simplified system is only sustainable if the duty to pay correctly is met by all, not just a few.

Without this foundational change, coupled with a commitment to bringing the informal sector into the light, simplification will remain an elusive dream. Success demands the necessary patience of linking tax policy to the long-term prosperity of the nation, rather than the short-term pursuit of immediate, fragmented results.

(Concluded)

Copyright Business Recorder, 2025

The writer is a seasoned Chartered Accountant, based in Karachi, with over 23 years of post- qualification experience in taxation

Comments

Comments are closed for this article.