As Pakistan’s imports begin rising again, some analysts take this as a sign of industrial revival, arguing the resulting deficits will ultimately translate into greater productive capacity.

This interpretation is both incomplete and misleading. It overlooks Pakistan’s underlying structural realities: a shrinking manufacturing base, weak export performance, declining investment, low domestic savings, and, most critically, an import basket increasingly dominated by non-industrial goods.

In economies with strong institutions, competitive manufacturing, and rising productivity, temporary external deficits are typically offset by export growth and industrial expansion. Pakistan, however, diverges from this model. It has run persistent current account (C/A) deficits while industrial capacity has eroded and the export-to-GDP ratio has fallen to one of the lowest in the region, undermining the notion that higher imports necessarily translate into higher exports.

In fact, non-industrial imports have exceeded industrial imports in most years, driven by demographic pressures and rising dependence on imported food while foreign exchange inflows remain constrained.

This imbalance requires a structural policy response, and that is the restoration of export competitiveness.

Structural shifts in import composition:

Over the past two decades, Pakistan’s imports have grown at a compound annual growth rate of 7.3 percent, rising from USD 13.5 billion to USD 59 billion, while exports increased just 4.7 percent annually. This widening gap has created two interconnected pressures: an export base unable to generate sufficient foreign exchange and a persistent struggle to finance a rising import bill.

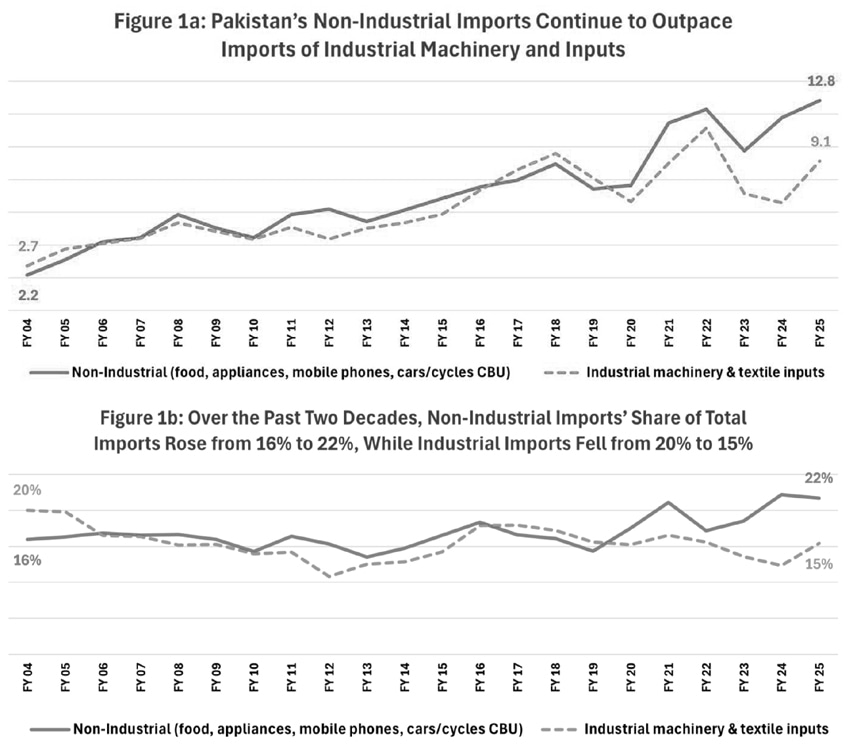

The trend is concerning as non-industrial imports have grown at more than twice the pace of industrial imports, including machinery critical for manufacturing. In 2025, for example, Pakistan imported USD 13 billion worth of non-industrial items, including palm oil, tea, home appliances, mobile phones, and completely built-up (CBU) cars and motorcycles, compared to USD 9 billion in machinery for power generation, construction, agriculture, and essential textile machinery and inputs such as cotton (Figure 1a).

During this time, the shift has become more pronounced as the share of non-industrial imports has risen from 16 percent to 22 percent of total imports, while the industrial share has fallen from 20 percent to 15 percent (Figure 1b).

This transition in Pakistan, where manufacturing machinery loses ground to non-industrial imports, reflects a broader pattern of deindustrialization and a consumption-led economic structure.

The consumption trap:

Proliferating imports are reinforced by Pakistan’s rapidly expanding population, which continues to drive demand for food, electronics, and construction materials. Major non-industrial imports exacerbate this trend as they lock Pakistan into a high import bill: palm oil, tea, and petroleum products are largely price inelastic, while imports of cars and mobile phones are characteristically income elastic and surge whenever household incomes rise, often fueled by remittances.

Data from July to October FY2026 shows that remittances have grown year on year for the past three fiscal years, with imports rising in parallel. Our earlier analysis of remittance inflows underscored a strong correlation between remittances, consumption and imports as a share of GDP in Pakistan, suggesting that non-industrial import demand will remain elevated and pressure on the current account will continue.

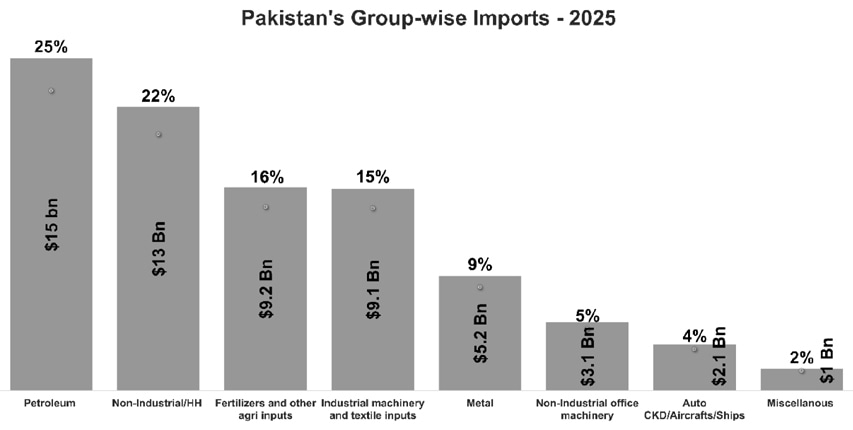

Pakistan’s dietary and consumption patterns further intensify this pressure. It is the world’s largest importer of tea, the highest per-capita consumer of sugar, and among the largest importers of edible oils. In FY2025, palm oil alone accounted for 6 percent of total imports, around USD 3.4 billion, while home appliances, mobile phones, and CBU cars and motorcycles contributed USD 5.2 billion, roughly 9 percent of the import bill.

Imported fertilizers, insecticides for domestic crop production, and other food-related items, excluding palm oil, such as spices, dry fruits, milk, and pulses, collectively made up 23 percent of total imports, or about USD 13.5 billion.

Structural vulnerabilities in Pakistan’s current account:

Extensive research shows that the sustainability of current account deficits depends on their underlying drivers. According to IMF economist Lazaros E. Molho, deficits tied to investment may be manageable, while those resulting from declining savings and rising consumption are not.

The export-to-GDP ratio is equally important. Countries running persistent deficits alongside falling export-to-GDP ratios inevitably face external instability (Wong, Khan and Nsouli, IMF, 2002). Vulnerabilities worsen when growth in non-tradables closely tracks widening trade deficits.

Pakistan underperforms across all these indicators. Its export-to-GDP ratio has fallen from a peak of 17.2 percent in 1993 to around 10 percent today. Many exporting firms, constrained by high costs of doing business, have diverted capital from tradables to non-tradables rather than expanding export-oriented production.

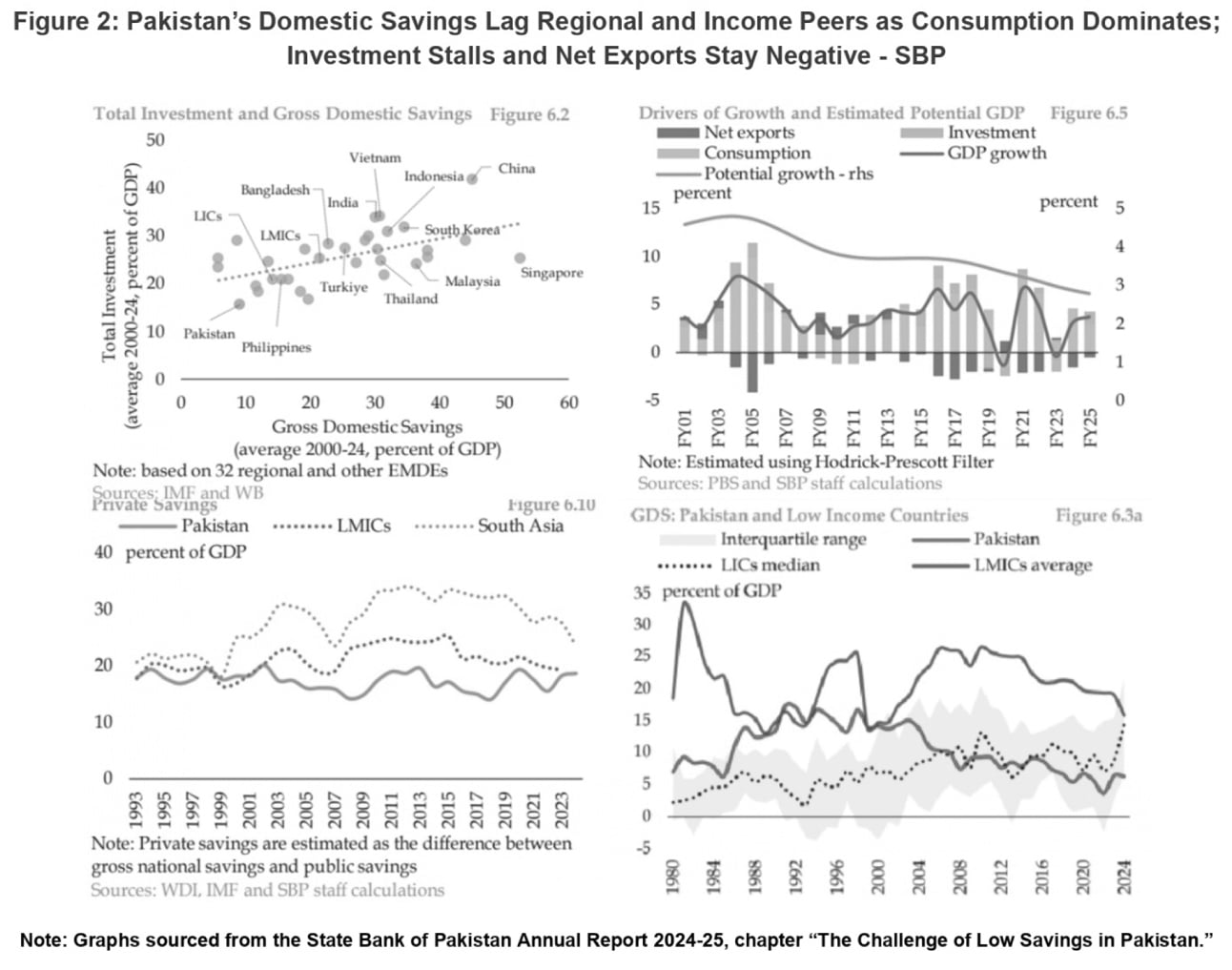

Pakistan’s investment and gross domestic savings as a share of GDP are the lowest among 32 regional and emerging economies, including India, Bangladesh, Vietnam, and Türkiye, according to the SBP (Figure 2).

Domestic savings even remain below the median of Low-Income Countries and economies with high inflation averaging 8 to 15 percent, high youth dependency, high informality, and low financial development. Pakistan’s marginal propensity to save is 0.18, significantly lower than India’s 0.28 and Bangladesh’s 0.25 (Khalid et al., 2015).

The SBP further notes that households tend to “spend first and save later”, a pattern observed even among higher-income groups. This aligns with Pakistan’s predominantly consumption-oriented economy, where private consumption has consistently accounted for nearly 92 percent of GDP for the last four decades, while investment remains negligible and net exports stay negative (Figure 2) (The State of Pakistan’s Economy, 2025).

These vulnerabilities have turned Pakistan’s current account deficits from cyclical to structural, persisting even as remittances rise.

Building exports is the only sustainable path:

Exporting businesses have repeatedly warned about high business costs and the growing risk of industrial decline. Combined with rising protectionism in Pakistan’s key markets and shrinking profit margins, prospects for robust export growth remain limited.

At the same time, non-industrial imports are expected to continue increasing in line with Pakistan’s population growth of 2.55 percent. Data from July to October FY 2026 already show that imports have risen year on year for at least three consecutive fiscal years.

The conclusion is clear. Sustained export growth is the only long-term remedy for Pakistan’s external vulnerabilities. Achieving this requires revitalizing large-scale manufacturing, strengthening SMEs, generating domestic employment for the country’s expanding youth population rather than over-relying on remittances, reforming the energy sector, and ensuring that exports are profitable enough to attract both reinvestment and new entrants into the tradable economy.

Under the IMF programme, the Fund should create some breathing space for Pakistan’s export-oriented industries. Currently, Pakistan is the only country taxing its export-oriented production at rates even higher than those applied to domestic production. Unless such irrational measures are reversed and export competitiveness is restored, rising domestic consumption will continue to destabilize Pakistan’s current account, eroding what little stability the economy has left.

Copyright Business Recorder, 2025

PUBLIC SECTOR EXPERIENCE: He has served as Member Energy of the Planning Commission of Pakistan & has also been an advisor at: Ministry of Finance Ministry of Petroleum Ministry of Water & Power

PRIVATE SECTOR EXPERIENCE: He has held senior management positions with various energy sector entities and has worked with the World Bank, USAID and DFID since 1988. Mr. Shahid Sattar joined All Pakistan Textile Mills Association in 2017 and holds the office of Executive Director and Secretary General of APTMA.

He has many international publications and has been regularly writing articles in Pakistani newspapers on the industry and economic issues which can be viewed in Articles & Blogs Section of this website.

Sarah Javaid is an Economist by education and practice, with experience in the Ministry of Commerce, the textile sector, and think tanks. She has participated in the monitoring mission of the Pakistan Regional Economic Integration Activity for USAID. Her writings focus on international trade and export competitiveness. Currently, she serves as a Trade Economist at the All Pakistan Textile Mills Association

Comments

Comments are closed for this article.