For the first time in forty months, FE-25 deposits held with commercial banks have crossed $7 billion. On surface, that looks like a vote of confidence.

In reality, it confirms what exporters, importers, and banks have all been signaling for months: money is choosing to wait.If the story of foreign bill discounting was about exporters slowly losing confidence in currency stability, the story of FE-25 deposits is about everyone else doing the same: just more discreetly.

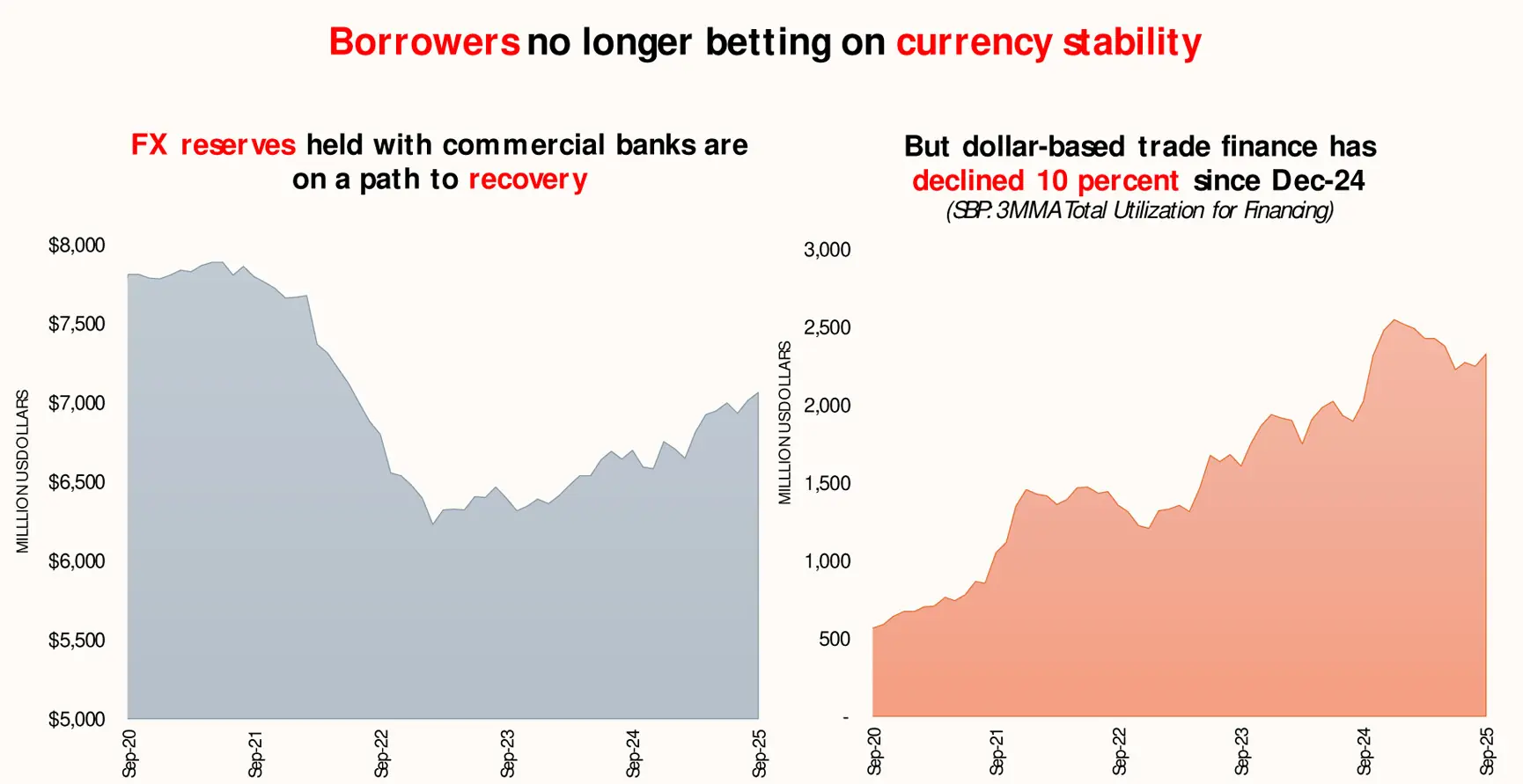

At their last peak in June 2021, FE-25 deposits stood at $7.9 billion, the highest level since August 1998. Between then and May 2023, through the worst of the external and inflation crises, commercial banks lost roughly $1.6 billion in these balances (FE-25 deposits) as the exchange rate collapsed from Rs157 to Rs286 in Jun 2023.

Since that bottom, deposits have crawled back from $6.3 billion in October 2023, finally breaching$7 billion in September 2025, a gain of barely $30 million per month. Of this, most of the recent acceleration has come over the past six months, as SBP finally signaled a break in its easing cycle and the interest-rate differential between PKRV and the Fed funds rate stabilized around 8 percentage points.

That spread, along with recovery in commercial banks’ FE balances, should have revived dollar-denominated trade finance. It did not. In fact, FE-based lending has shrunk by $222 million since December 2024. Import finance is down $277 million, with export finance barely recovering by just $55 million.

Commercial banks may not exactly be awash with dollars; but even the marginal recovery in dollar liquidity has few local avenues of deployment.

The psychology is simple. When currency management replaces price discovery, every participant learns to wait. Borrowers see little point in taking exposure when the exchange rate is frozen by policy, not by fundamentals.

Lenders prefer the comfort of passive deposits over the risk of repricing loans after the inevitable adjustment. The result is a financial system that looks liquid on paper but remains inert in practice.

This is what happens when stability outlives credibility. Two years of a near-static exchange rate have trained market participants to assume that any eventual correction will be abrupt. Until then, they shall sit tight.

Deposit growth becomes the mirror image of lending paralysis. The same dynamic visible in foreign bill discounting: exports growth in statis and proceeds slowdown - is now slowly extending to all sides of foreign exchange intermediation.

The policy establishment is likely to read the seven-billion-dollar mark as proof of regained confidence. It is anything but. A stockpile of idle deposits that is neither fueling trade nor financingworking capital expansion is no different from cash under the mattress. The nominal rise in FE-25 balances reflects preservation instincts, not optimism.

Unless the underlying signals change through credible currency market reform; predictable policy; and a real shift in growth expectations, this buildup will remain what it already is: a waiting room. Liquidity will stay parked, trade finance will stay thin, and the currency will remain stable only in name.

If the first act of this story was exporters holding their bills, the second act is depositors holding their breath. The curtain may not fall yet,but the system is simply frozen in time, watching the rate board for the move everyone knows is coming, sooner or later.

Comments

Comments are closed for this article.