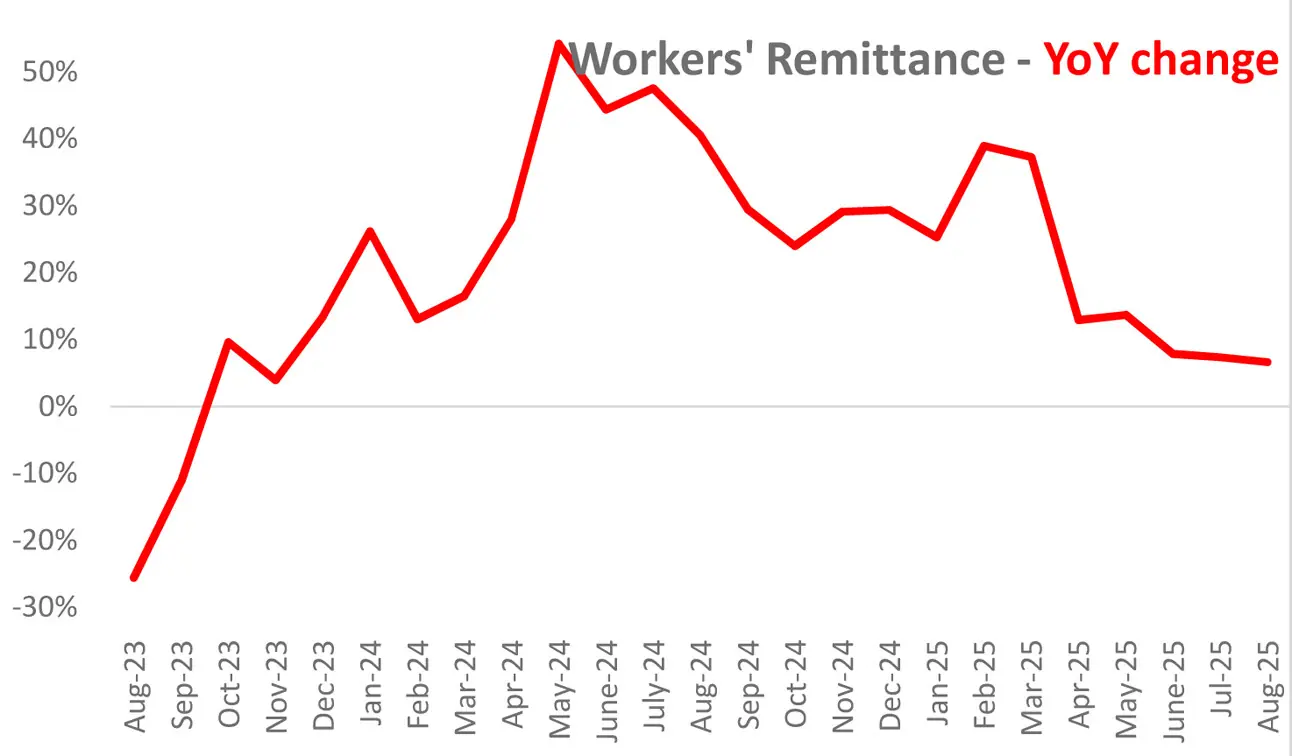

Workers’ remittances may well have already peaked. After an exceptional run-up through FY24, inflows are showing signs of fatigue.

The past three months have seen year-on-year growth slip into single digits, a stark contrast to the blistering pace witnessed earlier when inflows were growing north of 40–50 percent.

Part of the slowdown is explained by the high base effect, as remittances had surged to record levels last year. But market observers also caution that much of the “juice” from the crackdown on hundi/hawala channels may already have been squeezed out, leaving little room for further easy gains.

The policy backdrop is equally telling. The government last month approved a supplementary grant of Rs30 billion in lieu of the remittance subsidy, a scheme that has been instrumental in nudging inflows toward formal channels.

However, this year’s allocation is significantly smaller than the support extended in FY25. The reduced cushion raises questions over how aggressively banks will continue to push remittance mobilization, especially when overall momentum is softening. Industry players remain puzzled at the stop-go nature of the incentive, with repeated assurances from policymakers about continuity failing to fully settle nerves.

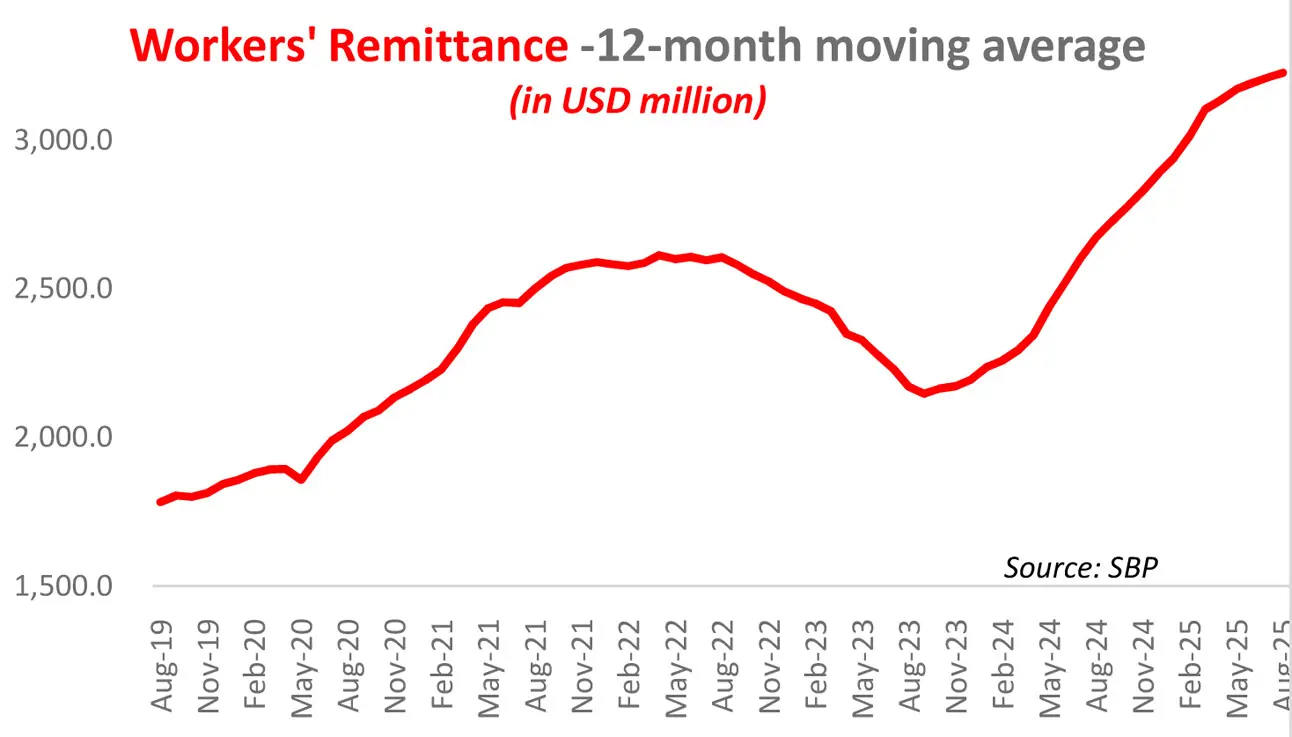

On a 12-month rolling basis, the trajectory is still pointing upwards, with average monthly inflows now above the $3 billion mark — an unprecedented milestone. Yet the curve itself appears to be flattening, suggesting that sustaining this momentum will take considerable effort. Without further policy clarity or structural tailwinds, the risk of plateauing looms large.

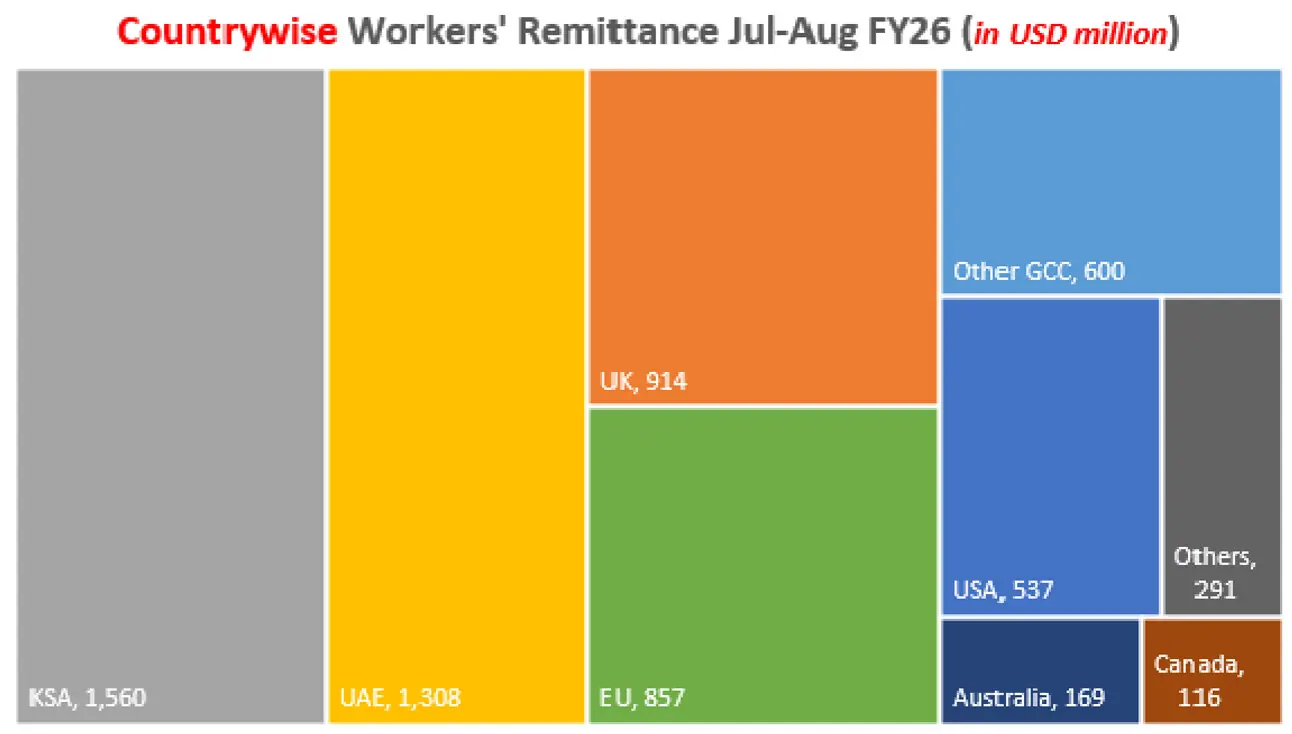

The country-wise breakdown for July–August FY26 reinforces the familiar narrative of dependence on the Gulf, with Saudi Arabia and the UAE contributing a combined $2.9 billion — nearly half of all inflows. What is noteworthy, however, is the relative weakness from the US and UK, despite their large expatriate bases. Instead, inflows from the EU (outside the UK), Australia, and Canada have begun to creep higher.

Together, these “non-traditional” destinations contributed nearly as much incremental growth as Saudi Arabia and the UAE combined — a rarity that signals the gradual broadening of Pakistan’s remittance footprint.

Looking ahead, much will depend on labor market demand in the Gulf, which remains tied to oil prices and fiscal spending in host economies.

Exchange rate stability will also play a crucial role, as even small gaps between official and informal channels can quickly divert flows. Just as important will be clarity on incentives, where stop-start subsidies undermine long-term planning for banks and money transfer operators.

The near-term picture is finely balanced. While remittances remain at historic highs, the momentum has clearly slowed. With imports expected to rise in FY26 and external account pressures unlikely to abate, policymakers will be hoping that the remittance engine does not stall just when the economy needs it the most.

Comments

Comments are closed for this article.