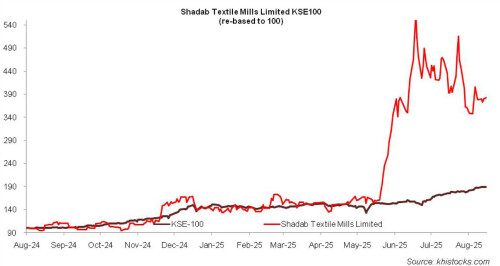

Shadab Textile Mills Limited (PSX: SHDT) was incorporated in Pakistan as a public limited company in 1979. The principal activity of the company is manufacturing, buying, selling and dealing in all kinds of yarn.

Pattern of Shareholding

As of June 30, 2024, SHDT has a total of 16.60 million shares outstanding which are held by 456 shareholders. Local general public has the majority stake of 50 percent in the company followed by Directors, CEO, their spouse and minor children holding 44.49 percent shares. NIT & ICP accounts for 3.14 percent shares of SHDT while joint stock companies hold 2.31 percent shares. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-24)

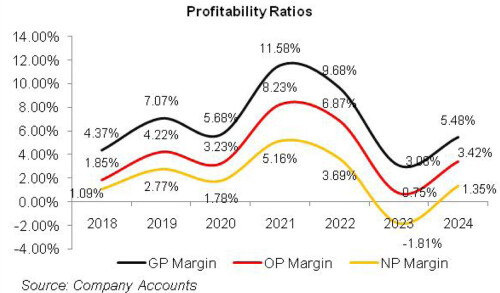

Except for a year-on-year decline in 2020, SHDT’s topline has registered growth over the period under consideration. Its bottomline plunged in 2020 and 2023 with net loss recorded in the latter year. SHDT’s margins which posted significant improvement in 2019, slid back in 2020. This was followed by a whopping rebound in 2021. In the subsequent two years, the margins considerably shrank to record their lowest values in 2023. In 2024, SHDT’s margins picked up. The detailed performance review of the period under consideration is given below.

In 2019, SHDT’s net sales grew by 23.86 percent to clock in at Rs.2813.43 million. This was on account of improved sales volume, better yarn prices and continuous supply of electricity to the textile sector. The government also notified the reduced electricity rate of 7.5 cents/kwh for zero rated textile industrial consumers.

This greatly reduced the energy cost. Overall cost of sales surged by 20.36 percent in 2019 on the back of higher prices of raw materials coupled with Pak Rupee depreciation. Gross profit strengthened by 100.38 percent in 2019 with GP margin climbing up to 7.07 percent from GP margin of 4.37 percent posted in 2018. Distribution expense escalated by 28.98 percent in 2019 on account of higher freight & other expense incurred on local sales.

Administrative expense multiplied by 27.80 percent in 2019 primarily due to higher payroll expense on account of inflation and also because SHDT expanded its workforce from 1084 employees in 2018 to 1092 employees in 2019. Other expense magnified by 188.27 percent in 2019 due to higher provisioning done for WWF and WPPF. Conversely, other income slid by 35.49 percent in 2019 due to lower gain recognized on the sale of operating fixed assets in 2019 and also because no office rent was received and no balances were written off during the year.

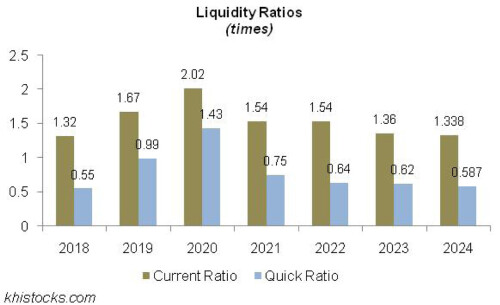

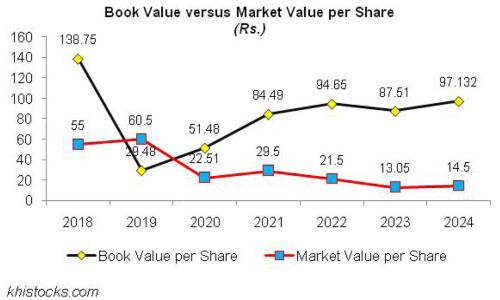

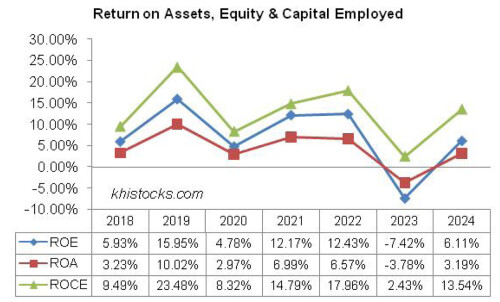

SHDT’s operating profit improved by 182.82 percent in 2019 with OP margin clocking in at 4.22 percent in 2019 versus OP margin of 1.85 percent posted in 2018. Finance cost escalated by 34.29 percent in 2019 which was on account of higher discount rate as the company considerably reduced its outstanding borrowings during the year. This is evident from the gearing ratio of 8 percent recorded by SHDT in 2019 versus gearing ratio of 29 percent posted in 2018. Net profit picked up by 215.93 percent in 2019 to clock in at Rs.78.045 million with EPS of Rs.24.31 versus EPS of Rs.8.23 recorded in 2018. NP margin also improved from 1.09 percent in 2018 to 2.77 percent in 2019.

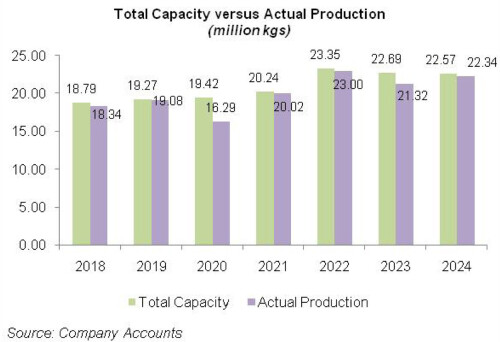

In 2020, SHDT’s topline contracted by 18.59 percent to clock in at Rs. 2290.54 million. This was on account of outbreak of COVID-19. The company’s production was reduced by 14.65 percent in 2020 to clock in at 16.287 kilograms due to lockdown imposed during the year (see the graph of production capacity versus volume). High cost of raw materials coupled with Pak Rupee depreciation resulted in 34.60 percent thinner gross profit in 2020 with GP margin inching down to 5.68 percent.

Lower sales volume translated into lesser freight charges. This drove down distribution expense by 6.19 percent in 2020. Administrative expense ticked up by 6.46 percent in 2020 due to higher payroll expense. This was despite the fact that the workforce was considerably streamlined to 1069 employees in 2020. Lower profit related provisioning resulted in 37.72 percent decline in other expense in 2020.

Conversely, other income posted a whopping 1008.73 percent rise in 2020 due to hefty profit recognized on bank deposits. Operating profit tapered off by 37.74 percent in 2020 with OP margin moving down to 3.23 percent. Finance cost posted a paltry growth of 4.53 percent in 2020 due to increased short-term borrowings. Net profit narrowed down by 47.66 percent to clock in at Rs.40.85 million in 2020 with EPS of Rs.3.27 and NP margin of 1.78 percent.

In 2021, SHDT’s net sales recorded a robust comeback with year-on-year growth of 44.3 percent to clock in at Rs.3305.217 million. This was the result of improved demand from value-added textile sector post global pandemic coupled with better sales price of yarn. Capacity utilization was recorded at 98.92 percent in 2021 with actual production clocking in at 20.017 kilograms, up 22.90 percent year-on-year. While raw materials price was on the higher side, local currency remained relatively stable compared to last year. This resulted in 194.14 percent higher gross profit recorded in 2021 with GP margin attaining its highest level of 11.58 percent.

Higher sales volume drove distribution expense up by 29.62 percent in 2021. Administrative expense also surged by 33.71 percent in 2021 due to higher payroll expense as workforce was expanded to 1194 employees. Other expense mounted by 256.78 percent in 2021 on the back of higher profit related provisioning. Conversely, other income slid by 55.97 percent in 2021 due to lower gain recognized on bank deposits due to monetary easing and also because the company en-cashed its TDRs worth Rs.236 million in 2021.

Operating profit strengthened by 267.83 percent in 2021 with OP margin climbing up to 8.23 percent. Finance cost mounted by 206.54 percent in 2021 due to long-term loan worth Rs.328.677 million obtained under TERF scheme for the import of gas generators. SHDT also acquired greater short-term borrowings during the year to meet its working capital requirements. Net profit progressed by 317.73 percent in 2021 to clock in at Rs.170.64 million with EPS of Rs.10.28 and NP margin of 5.16 percent.

In 2022, SHDT’s topline boasted the highest year-on-year growth of 60.28 percent to clock in at Rs.5297.44 million. This was the consequence of higher demand and improved prices. Production stood at 22.998 million kilograms, up 14.89 percent year-on-year.

Despite upward price revision, elevated raw material prices, conversion cost and Pak Rupee depreciation drove down SHDT’s GP margin to 9.68 percent in 2022. Gross profit in absolute terms grew by 34 percent in 2022. Higher freight on local sales drove distribution expense up by 41.58 percent in 2022.

Higher payroll expense on account of inflationary pressure pushed up administrative expense by 26.68 percent in 2022. Number of employees was squeezed to 1173 during the year. Higher profit related provisioning drove up other expense by 22.13 percent in 2022. Other income couldn’t support either as it slid by 42.23 percent in 2022 on account of thin profit earned on bank deposits.

Operating profit enhanced by 33.83 percent in 2022, however, OP margin moved down to 6.87 percent. 119.69 percent higher finance cost incurred by SHDT in 2022 was due to elevated discount rate coupled with higher short-term borrowings to meet working capital requirements.

Higher finance cost together with the imposition of super tax contained the bottomline growth to 14.42 percent in 2022. SHDT net profit was recorded at Rs.195.255 million in 2022, up 14.42 percent year-on-year. This culminated into EPS of Rs.11.76 and NP margin of 3.69 percent in 2022.

SHDT’s net sales ticked up by 12.56 percent in 2023 to clock in at Rs.5962.78 million. While textile demand was suppressed across the world due to global recession, topline growth was the result of higher prices. In accordance with shrunken demand, the company produced 21.322 kilograms of yarn, down 7.29 percent year-on-year. This translated into capacity utilization of 93.96 percent in 2023. Lesser capacity utilization resulted in low absorption of fixed cost.

This culminated into 64.20 percent lower gross profit in 2023 with GP margin hitting its lowest level of 3.1 percent. Lower sales volume also translated into 79.19 percent decline in distribution expense in 2023. Conversely, administrative expense inched up by 12.83 percent in 2023 due to higher payroll expense despite rationalizing workforce to 1125 employees. The company didn’t book any profit related provisioning during the year. Lower gain recognized on the disposal of fixed assets also pushed down other income by 58.15 percent in 2023. SHDT’s operating profit registered 87.79 percent year-on-year plunge in 2023 with OP margin moving down to 0.75 percent. Finance cost enlarged by 91.19 percent in 2023 due to monetary tightening. SHDT incurred net loss of Rs.107.742 million in 2023 with loss per share of Rs.6.49.

In 2024, SHDT recorded 22.10 percent year-on-year growth in its topline which clocked in at Rs.7280.768 million. Overall demand remained suppressed due to higher prices of raw materials, Pak Rupee depreciation and elevated energy tariff. However, during the 2nd and 3rd quarter of FY24, Pak Rupee began to gain momentum. The company increased the prices of its products to absorb high cost. This resulted in 117.29 percent higher gross profit in 2024 with GP margin moving up to 5.48 percent.

Distribution expense shrank by 81.28 percent in 2024 on account of lower freight expense on local sales. Administrative expense posted 9.74 percent uptick in 2024 on account of inflationary pressure which drove up the payroll expense. This was despite bringing down the number of employees to 1083 in 2024. The company recorded other expense of Rs.36.03 million in 2024, of which Rs.27.513 million represented loss recorded against the theft of machinery parts. Other income also enhanced by 1258.13 percent in 2024 due to insurance claim of Rs.27.68 million recorded in 2024. Operating profit magnified by 459.48 percent in 2024 with OP margin clocking in at 3.42 percent. Finance cost tumbled by 2.29 percent in 2024 due to lower outstanding borrowings. SHDT recorded net profit of Rs.98.47 million in 2024. EPS stood at Rs.5.93 while NP margin was recorded at 1.35 percent in 2024.

Recent Performance (9MFY25)

During the nine-month period of FY25, SHDT recorded 12.10 percent uptick in its topline which clocked in at Rs.5928.614 million. Improvement in macroeconomic indicators not only allowed the company to improve its sales volume but also bring down its cost. This coupled with the installment of 1.75 MW solar power plant enabled the company to attain 49.38 percent stronger gross profit in 9MFY25 with GP margin clocking in at 7 percent versus GP margin of 5.26 percent recorded in 9MFY24. Higher sales volume resulted in 81.96 percent surge in distribution expense in 9MFY25. Administrative expense also escalated by 16 percent in 9MFY25 due to higher payroll expense on account of inflationary pressure. 173.23 percent spike in other expense in 9MFY25 appears to be the consequence of higher profit related provisioning done during the period. However, it was greatly offset by 31.44 percent stronger other income recorded in 9MFY25 seemingly on the back of exchange gain. SHDT’s operating profit multiplied by 63.78 percent in 9MFY25 with OP margin clocking in at 4.90 percent versus OP margin of 3.36 percent posted in 9MFY24. Finance cost tumbled by 27.19 percent in 9MFY25 on the back of monetary easing and considerable reduction in short-term and long-term borrowings. Net profit posted a staggering year-on-year growth of 87.41 percent to clock in at Rs.145.084 million in 9MFY25. This translated into EPS of Rs.8.74 in 9MFY25 versus EPS of Rs.4.66 posted in 9MFY24. NP margin also picked up from 1.46 percent in 9MFY24 to 2.45 percent in 9MFY25.

Future Outlook

Stability in the value of local currency off-late and improved economic fundamentals which include controlled inflation and the onset of monetary easing cycle are the positive factors for SHDT and for the overall economy. The government has also recently announced the reduction in electricity tariff which will pave way for further cost reduction for SHDT. The company should also diversify its geographical presence to enhance its volumes and margins and also to hedge against fluctuations in the value of Pak Rupee.

Comments

Comments are closed for this article.