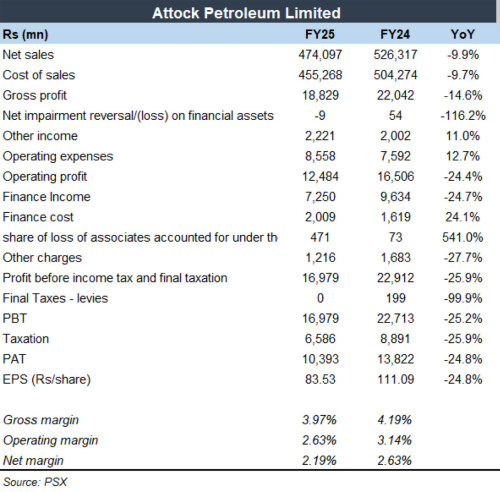

Attock Petroleum Limited (PSX: APL) had a slower year in FY25 after a very strong FY24.Earnings fell 25 percent year-on-year as the topline contracted 10 percent. Dividend payout for the year totalled Rs25.5 per share, including a Rs13 final. The revenue decline was driven by softer average refined petroleum prices and a weaker product mix: motor gasoline prices eased, fuel oil offtake slumped, and overall volumes stayed under pressure despite a seasonal lift late in the year.

The company still benefited from a healthier fourth quarter—net sales rose double-digits quarter-on-quarter with volumes up amid Kharif sowing—yet this was not enough to offset the full-year drag. Gross profit slipped about 15 percent with the gross margin easing to 3.97 percent for FY25, reflecting muted inventory gains in a year of relatively stable international prices; that said, the fourth-quarter margin improved versus the same quarter last year on smaller inventory losses.

The cost and expense mix also moved up. Operating expenses were up by roughly 13 percent year-on-year, while finance costs increased 24 percent. Finance income fell about 25 percent year-on-year as interest rates declined. A brighter spot was the share of profit from associates, helped by a better refining environment in parts of the year that provided some cushion to the core operations.

Underlying volumes and market position explain much of the narrative shift. APL’s total offtake is estimated at around 1.4 million tons for FY25, down 6 percent year-on-year, which pulled annual market share to about 8.8 percent from roughly 9.9 percent in FY24.

The weakness was concentrated in fuel oil (down nearly 48 percent year-on-year), while ex-fuel-oil volumes grew about 2 percent. This composition change and softer retail prices translated into lower inventory gains than the prior year’s peaks, capping gross profitability.

APL’s profits now clearly depend on interest income and inventory changes, while its falling market share shows how competitive the OMC sector is in a weak demand cycle.

Even so, it ends FY25 with a solid balance sheet, steady dividendsand better contributions from associates. Growth from LPG and EV-related projects is possible, but the near term will depend on demand recovery, price swings, and interest rates

Comments

Comments are closed for this article.