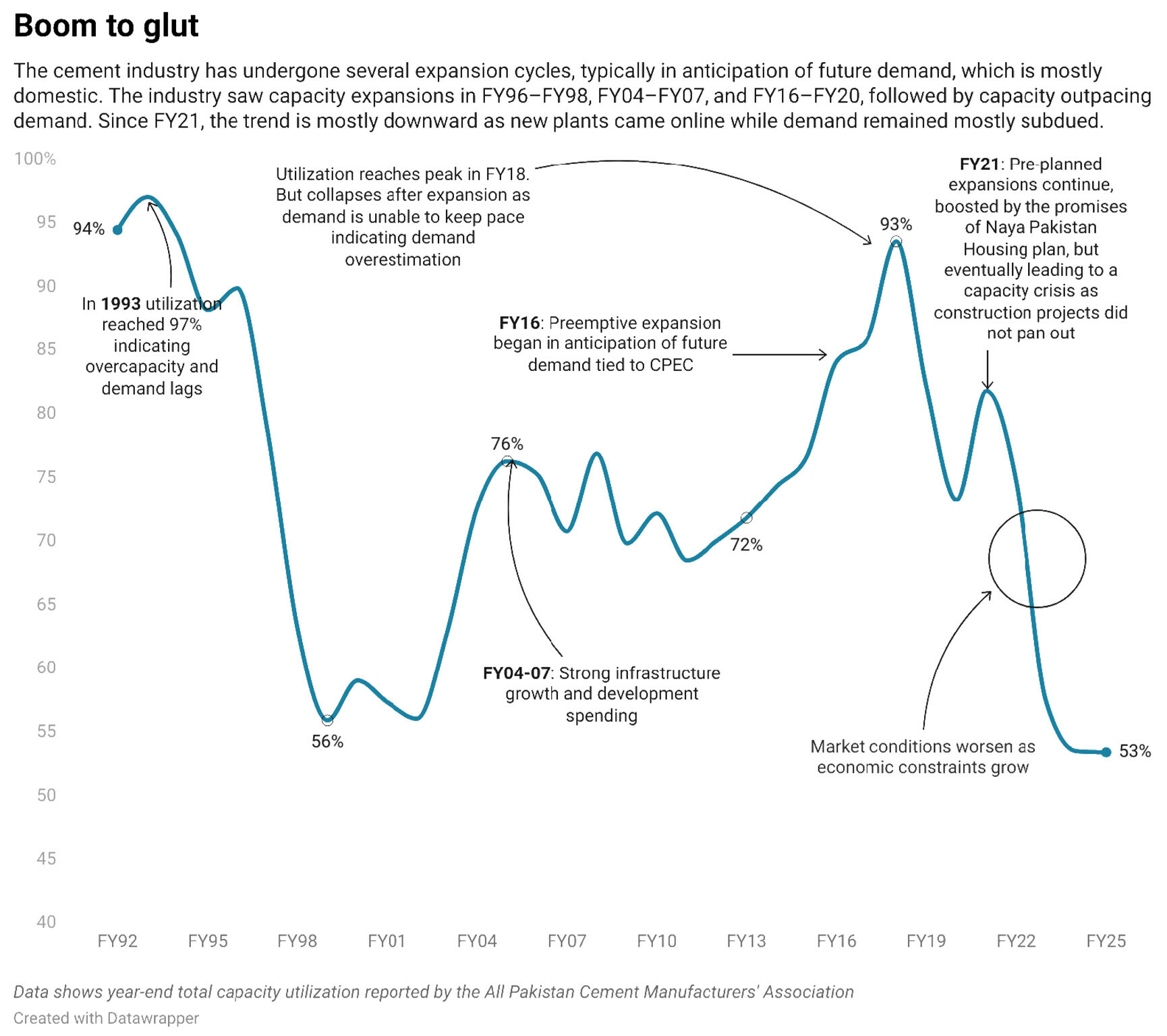

At record low capacity utilization, trailing somewhere below 53 percent, the cement industry is set to grow profits in double-digits during FY25.

In 9MFY25, profitability was up 57 percent cumulatively for listed cement companies and in the fourth quarter, market expectations are that the industry will experience earnings expansionbetween 14 and 30 percent.

This is despite a nominal growth in total offtake of 2 percent; bolstered by a 30 percent growth in cement exports and a 3 percent decline in domestic sales of cement in the full year.

The profitability is enabled not only by robust exports but domestic pricing power and a cost discipline that is unparalleled.

This can be corroborated by industry’s financial performance in 9M where revenue per units sold grew 6 percent year on year, while costs only rose 1 percent. This similarly coincides with average pricing data from Pakistan Bureau of Statistics (PBS) that shows in FY25, average cement prices in the north portions of the country rose 6 percent, while they were up 21 percent in the southern locations.

Domestic producers enjoy a persistent pricing power in the domestic markets with close association and tacit agreement on price directions that gives the industry a significant advantage over market dynamics. It is for this reason that even at such low levels of utilization, companies have not entered into price wars to sell off excess cement which is the typical modus operandi in a competitive market.

Instead, when domestic demand becomes saturated, the new strategy is to cast their net wider into exporting markets where Pakistani cement can gain acess—though at much more competitive prices than cement makers are used to at home.

It is no surprise then that exports contributed to 20 percent of the sales mix in FY25, which was 16 percent and 10 percent in the years prior. Even at these levels of exports contribution though, the capacity utilization of less than 60 percent is concerning for demand.

One that has been marred by continued macroeconomic challenges and cuts in development spending. That cement manufacturers are still turning profits is a testament to not only strong retention pricing (prices have risen 2.2x since FY21) but a control over their energy costs that have been curtailed through investments in effeciency enhancing energy projects.

At the same time, controls over overheads, and financial costs being covered by other income and investments also buttresses post-tax income.

In FY26, while price trajectories are expected to remain the same (upward looking), recent government policies to boost real estate and construction activity through tax measures and housing subsidies will revive demand in the short-run. This will allow cement manufacturers to keep their utilization at reasonable levels and cover their fixed costs. With no new major expansions on the horizon, FY26 may be the time for investors to enjoy the spoils of their labor past.

Comments

Comments are closed for this article.