After a robust 22 percent year-on-year jump in electricity generation in April 2025, May barely moved the needle—posting a muted 0.8 percent growth. Yet, the headlines didn’t hold back. Some clung to the seemingly impressive 21 percent month-on-month rise—an arguably meaningless metric in power sector analysis, where seasonal heating demand between April and May is anything but constant.

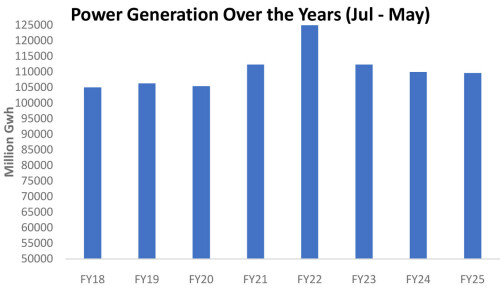

A bit of context puts things into perspective. May 2025’s power generation clocked in at 12.3 billion units—lower than FY21, just 5 percent above the Covid-lockdown nadir of FY20, a mere 1 percent ahead of the FY19 slump, and a full 13 percent—or nearly 2 billion units—below the FY22 peak.

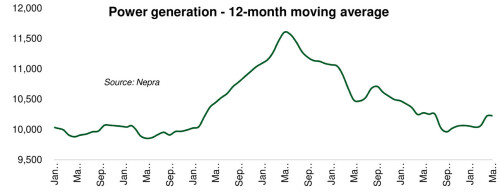

The cumulative 11MFY25 tally stands at 110 billion units, the lowest since FY20 and 12 percent off the high-water mark of FY22. The 12-month rolling average, now at 10.2 billion units, offers little consolation—this level was first reached back in March 2021.

A notable drop in average tariffs across the board appears to have done little to reignite demand from last year—even with May recording its second warmest nights in history. Any signs of recovery must be viewed with caution: average household consumption per connection had plunged to a 20-year low in 2024. What’s likely propping up generation now is not a demand boom, but the slow and steady return of captive power users to the national grid.

It’s early days for hard numbers, but the policy intent is clearly taking hold. With higher gas prices and added levies, captive generation is fast becoming uneconomical. At current cost structures, staying off-grid is no longer viable for most industrial users—the switch to grid electricity now appears inevitable. The government’s core objective is unmistakable: reallocate scarce natural gas toward more efficient, centralized power generation.

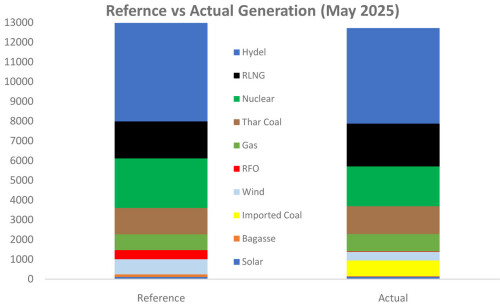

Actual power generation once again lagged behind reference benchmarks, with imported coal posting the widest gap. While no output was scheduled from imported coal plants in May 2025, the grid still leaned on them for nearly 800 million units—largely to offset shortfalls from wind, hydel, and nuclear sources.

Neelum-Jhelum remains offline, and an unusually dry season has further dented hydel prospects. With the added spectre of Indian water aggression, the outlook for hydropower is bleak—forcing greater reliance on expensive thermal generation.

May marked the second consecutive month of a positive Fuel Charge Adjustment (FCA), breaking a long streak of negative revisions. But this shift has less to do with rising fuel costs and more to do with wide variances from reference generation figures.

The FY26 generation plan underpinning the base tariff appears pragmatic and should help contain volatility in future adjustments. The real wildcard is demand resurgence. With solar steadily shaving off grid demand during daylight hours, much now hinges on the pace of industrial recovery—especially from users returning to the grid under the revised captive generation policy.

Comments

Comments are closed for this article.