Attock Petroleum Limited's (PSX: APL) has become quite focused in its strategy. The oil marketing company has been concentrating its efforts and investments in the retail fuel segment, which is just the right approach at this time not only because of rising demand for petrol and diesel, but also because of a high probability of furnace oil losing its shine over the next few years; with over 6000 MW of power supply coming from gas and coal sources by FY19-20, FO-based power generation should take a back seat.

APL's improving profitability over the last three to four years also speaks volumes of the OMC's rising retail presence and growing network. Increasing volumetric sales too have been of HIgh Speed Diesel and Petrol, which has promted the OMC to expand its retail network, capacity and storage infrastructure. According to Elixir Secuities research note on APL, the firm has grown its retail network at around 50 outlets per annum over the past five years. It has also entered into some long term contracts with the government and the Pakistan Army for jet fuel and HOBC, respectively.

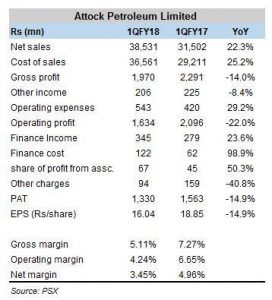

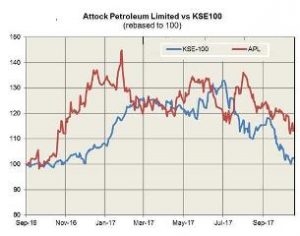

FY17 was a great year for APL where the firm saw a jump in not only its earnings but also its revenues, brought by strong growth in volumetric flows and better oil prices. While the growth in revenues was continued in the first quarter of FY18, the earnings announced yesterday fell short of 1QFY17 profit-after-tax. However, it didn't look as if it fell short too of the investors' expectations as the scrip gained around three percent, closing in at Rs607.06

The earning announcement was also higher than the market's expectations; even though on a year-on-year basis, 1QFY18 gross margins were lower (5.11% vs 7.27%), higher than expected earnings likely emanated from improved gross margins on a quart-on-quarter inventory gains that lifted the gross margins (5.11% in 1QFY18 vs 3.79% in 4QFY17).

A key factor that gives APL an edge over its competitors is its relatively leaner balance sheet and convenient receivables turnover, and hence low sensitivity to the circular debt. It gives APL more room for expansion. All this is reflected in the stock's target price by the brokerage industry ranging between Rs745-751 against yesterday's close at Rs607.

Comments

Comments are closed for this article.