In early 2026, Pakistan seemed to have turned a corner, but this was only a short-lived encouraging moment. By April 2025, inflation had dropped to a historical low of 0.3 percent, having hit a peak of about 38 percent in 2023.

In January 2025, the State Bank’s foreign exchange reserves had reached a record of USD 16 billion. The rupee was stabilized.

The IMF has had a 25th Extended Fund Facility of USD 7 billion in Pakistan since 1958, and it is on track. The country’s policymakers, after years of crisis-to-crisis lurching, were, for the first time in a generation, tentatively planning to grow rather than to cope with collapse.

All those gains are in acute danger by May 2026. A war on Iran by the US and Israel, and its energy crisis, the devastating 2025 monsoon floods, and the unresolved specter of a new wave of military conflict between India and Pakistan are dissolving and rebuilding, and Pakistan cannot afford to lose.

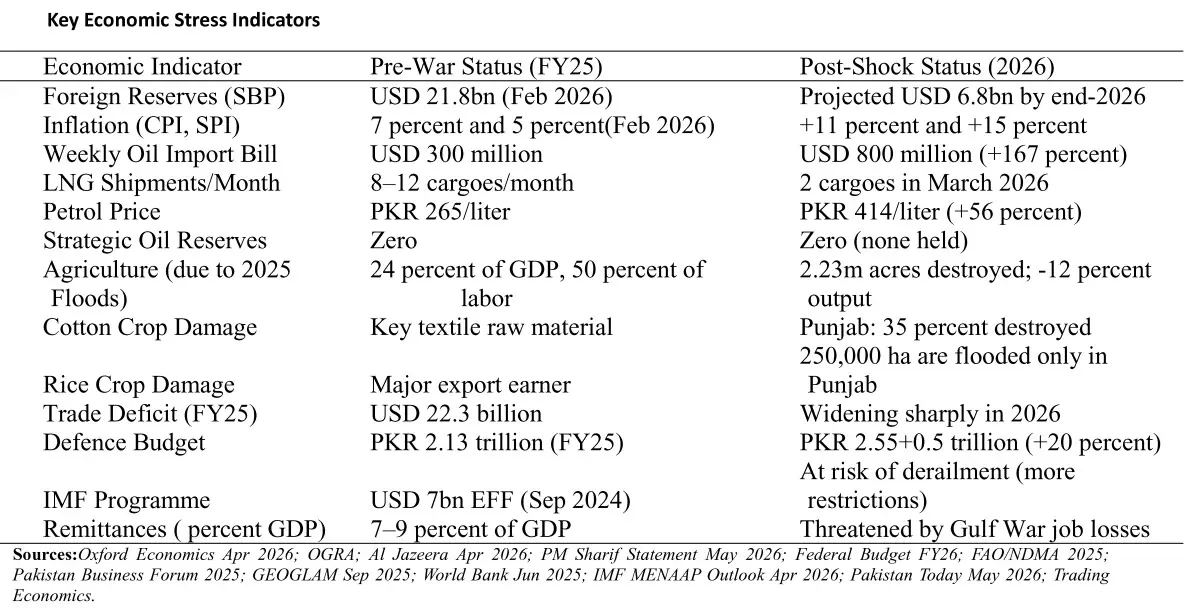

As of March 4, Iran had virtually closed the Strait of Hormuz, through which about 20 percent of the world’s oil trade and about one-fifth of global LNG flows pass. The Brent crude price had shot up to near USD 120 per barrel and is now around USD 110 per barrel.

In Asia, LNG spot prices increased by more than 140 percent. Qatar and the UAE account for 90 percent to 99 percent of Pakistan’s total LNG imports and approximately 80 percent of its crude oil imports. This was a serious external shock to most economies, while for Pakistan it was structural exposure at its death knell.

As recently as January 2026, Pakistan had been operating a surplus of LNG – demand had dropped three years in a row as cheap solar panels flooded the market, and the government had been diverting surplus cargoes to other nations. That excess wilted away in weeks.

In January, Pakistan received 12; in March, the month the war started, it only received 2 shipments of LNG. The management of the National Electric Power Regulatory Authority (NEPRA) has expressed concern about the near-zero LNG stock levels in the coming months. Given that LNG accounts for almost 25 percent of Pakistan’s electricity, its impacts on industrial and agricultural production are immediate and dire.

The weekly oil import bill of Pakistan, as the Prime Minister (PM) Shehbaz Sharif himself has said this week, has increased almost 167 percent compared to its level before the war, from USD 300 million to USD 800 million.

The government had to declare extensive emergency austerity measures, a 4-day workweek, mandatory work-from-home rules, school closures, and limits on social gatherings. “Pakistan does not have any strategic reserves, even a day of in stock, and is fully reliant on commercial stocks” (Pakistan Federal Petroleum Minister Ali Malik, May 2026).

On 26 June 2025, Punjab experienced severe monsoon floods, resulting in agricultural production losses of USD 4.2 billion. The national crop production fell by more than 12 percent, and a total of 2.23 million acres of farmland were destroyed. Damage covered about 60 percent of rice and 30 percent of sugarcane crops, and around 35 percent of cotton area.

Since agriculture accounts for 50 percent of the labour force and contributes 23 percent to GDP, the shock had far-reaching economic effects.

Cotton shortages are holding back the textile industry, sugar mills are not running at full capacity, and broken irrigation systems are threatening next crop planting. On the energy side, industrial electricity shortages are being exacerbated by LNG supply disruptions and a more than doubling of furnace oil prices.

The services sector, which accounts for more than 59 percent of GDP, is also affected by rising petrol prices, higher transport and food costs, and a decline in consumer demand in the informal sector, which provides almost 75 percent of Pakistan’s non-agricultural labour force.

Consequently, FY26 GDP growth will now be reduced to 2.5 percent-3.0 percent, down from the target of 4.2 percent.

To make matters worse, there is a risk to remittances, the cornerstone of the Pakistani external account. In 2025, the country’s current account entered into surplus for the first time in 14 years due to high inflows of Pakistani workers from GCC countries, equivalent to about 5 percent of GDP. This support is now squarely under threat due to war. Hundreds of thousands of Pakistani workers might not be able to travel to GCC countries this year, and others are returning home earlier. A re-entry diaspora simultaneously reduces remittance inflows and strains a local labour market already facing over 8 percent youth unemployment.

Pakistan’s GDP growth in FY2026 is expected to be between 2.5 percent and 3.0 percent, given the shock across all productive sectors of the economy. In the event of severe crop losses, agriculture not only suffers but also leads to shortages of raw materials for textile industries and sugar factories, and to decreased exports as total import costs rise.

As the energy crisis worsens, so do the costs of inputs for industrial production, and thus, there is no motivation for investors to invest in the industry.

The situation is no better about service sector, which accounts for almost 60 percent of GDP, because rising fuel costs also raise transportation and food prices, thereby lowering consumer purchasing power.

Remittances from workers in the Gulf region would decrease due to the US-Iran conflict, which would reduce employment opportunities, weakening the sector that had served as an insurance mechanism against Pakistan’s trade deficit.

The rising cost of imported oil will push the government to impose austerity measures rather than increase expenditure. This way, when agriculture experiences shocks, energy costs increase, industries pull back, and people do not consume, leaving no room for the government to intervene.

Copyright Business Recorder, 2026

The writer is an Associate Director Research, School of Management Sciences, Beaconhouse National University, Lahore

Comments