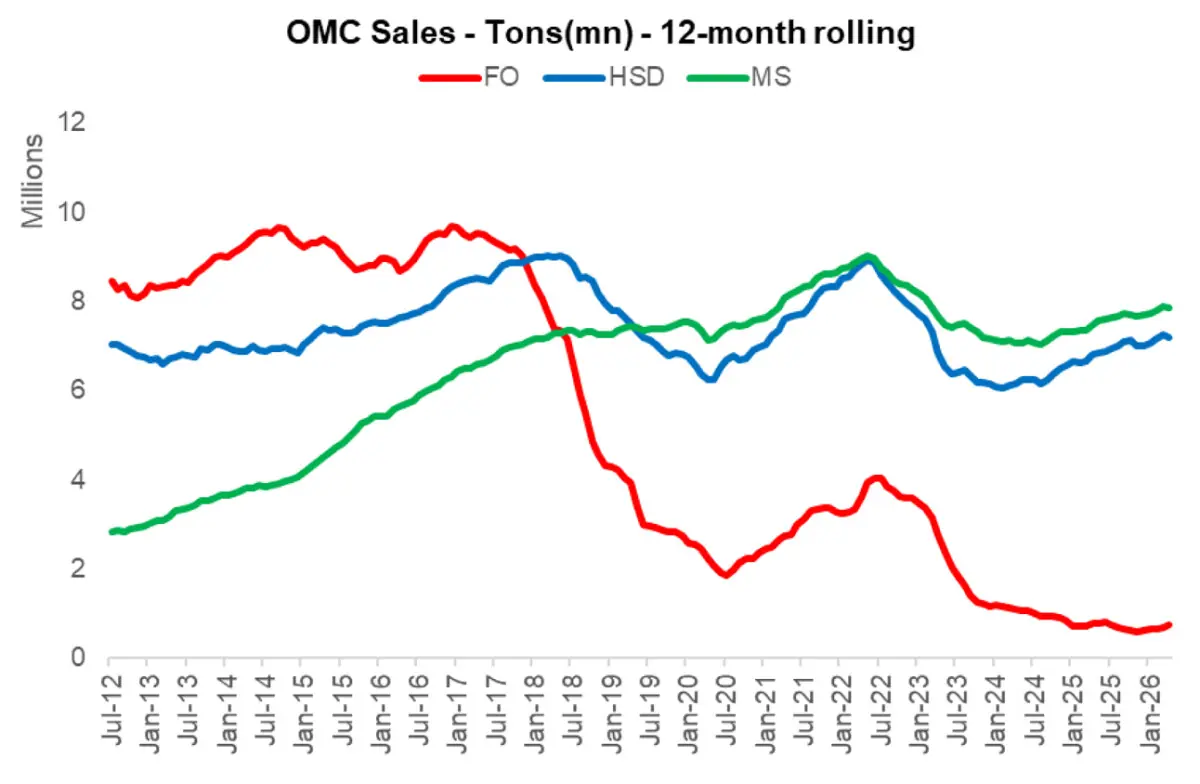

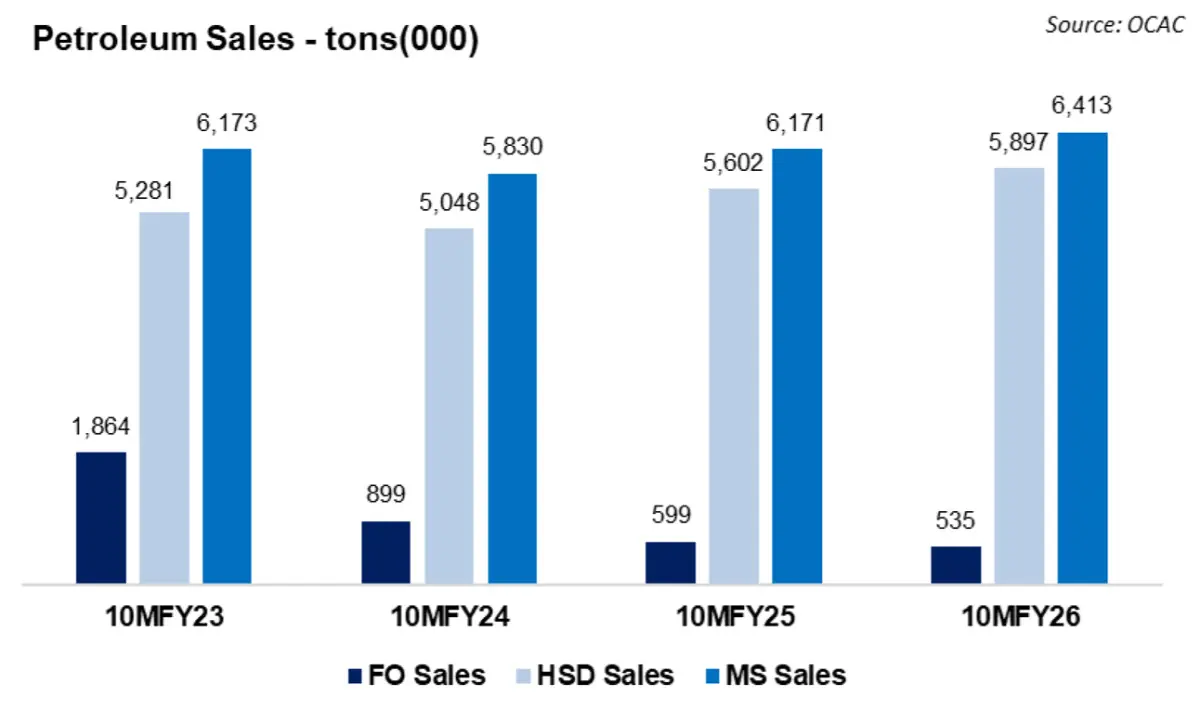

While on a cumulative basis, the OMC sector is still in recovery mode, the Monthly figures have started to show stress from the sky-rocketing petroleum product prices due to the global supply impasse. Total petroleum sales in 10MFY26 rose 4.1 percent year-on-year, with ex-furnace oil volumes up 5 percent year-on-year.

Motos Spirit sales increased 4 percent year-on-year, and HSD sales rose 5.3 percent during the 10MFY26, primarily due to the weak base of FY25. Furnace oil remained the exception, falling 11.3 percent year-on-year in 10MFY26 to 0.53, despite the late spike in March-April.

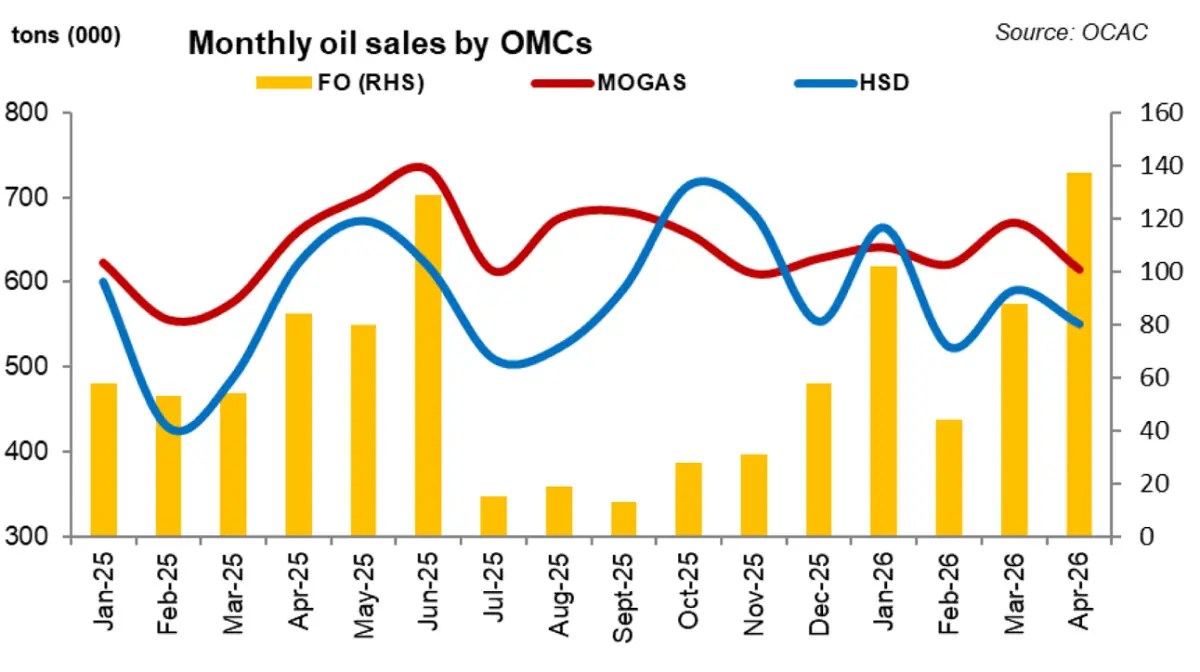

April, however, was weak. Total OMC volumes fell 6.7 percent year-on-year and 5.8 percent month-on-month.

The weakness was sharper in core fuels in Apr-26: ex-FO volumes dropped 11 percent year-on-year and 9.8 percent month-on-month. MS sales declined 6.9 percent year-on-year, while HSD fell 11.6 percent during Apr-26.

The immediate drag was pricing. Petrol and diesel prices rose sharply in April with MS prices up 24 percent and HSD up 19 percent month-on-month which has brought discretionary travel, small transport activity, agriculture-linked diesel demand, and lower-income consumption under pressure.

FO was the only clear outlier. FO sales jumped 63 percent year-on-year and 56 percent month-on-month in Apr-26, driven by higher FO-based power generation due to RLNG supply disruptions. It is basically a sign of stress in the fuel mix.

The refinery side adds an important supply dimension. Refinery upliftment rose around 13 percent year-on-year in Apr-26, with HSD uplift up 11 percent and FO uplift up 26 percent.

Stronger HSD uplift was due to greater OMC demand, HSD import disruptions, tighter curbs on Iranian inflows and higher utilization.

In 10MFY26, refinery upliftment rose 12.6 percent supported by higher MS and HSD offtake. This helped domestic availability, but it also shows that the market is operating in a more constrained import environment.

With rising petroleum product prices expected further, MS is likely to remain the most exposed to household purchasing power, while HSD will depend on transport activity, agriculture demand, industrial movement, and the direction of diesel prices.

The global supply situation remains the biggest risk. The Middle East conflict and disruption around the Strait of Hormuz have kept oil and LNG markets fragile. This indicates three pressures simultaneously for the Pakistan: higher landed fuel costs, uncertainty over product availability, and shifts in the power fuel mix if LNG flows continue to be disrupted.

FO demand may therefore remain volatile — rising when power-sector gas availability tightens but not necessarily reflecting sustainable demand.

Comments