The government chose shock therapy. Petrol prices were raised by Rs137 per liter, a 43 percent jump. High Speed Diesel went up by Rs184 per liter, or 55 percent. For context, less than four years ago, the entire retail price of HSD was lower than this single increase. The move was always coming. Subsidies had spiraled past Rs130 billion in just one month. The arithmetic was untenable. Ending the price suppression was necessary and widely prescribed.

But necessity does not excuse execution.

Within minutes of the notification, the fine print told a different story. The Petroleum Levy was jacked up to Rs160 per liter, up by Rs55 in a week. The price differential claim, effectively the subsidy, was scrapped. That part was expected and justified. The problem was the simultaneity. The policy intent, as argued by sanest voices, was to eliminate an unsustainable subsidy. Not to do so while slapping record taxation on top.

For a brief window, Pakistan’s petrol prices climbed into the upper tier globally. Not because of market dynamics alone, but because the tax component was pushed to extremes. The logic appears to have been tactical. HSD, even without taxes, saw a massive increase. Diesel feeds directly into transport and food inflation. The indirect pass-through is far stronger than petrol. To cushion that impact, the government leaned on petrol consumers to compensate for lost revenue. It was a fiscal offset masquerading as pricing policy.

The IMF likely loomed large in the background. The Fund has little tolerance for slippages, particularly on the Petroleum Levy, which has become a key revenue anchor. But even by those standards, the sequencing was clumsy. Within 24 hours, the decision was partially reversed. The levy was halved. Yet even after the largest announced reduction, petrol prices remain at record highs. The episode leaves behind confusion rather than credibility.

Diesel pricing raises a different, older question. The current formula once again delivered windfall gains to domestic refineries. Nearly three quarters of HSD demand is met locally. When international premiums spike, the pricing mechanism passes that through regardless of local cost structures. The result is extraordinary margins in periods like this. Critics have long argued that the formula overcompensates in such scenarios. Defenders counter that refiners also absorb downside risks when margins compress. That is true. But it does not fully address the asymmetry during extreme spikes.

Which leads to a broader structural question. Why not fully deregulate OMC pricing and use taxation as the shock absorber? In theory, that would allow prices to reflect market realities while the state intervenes only to smooth volatility or protect revenues. In practice, the government’s hands remain tied.

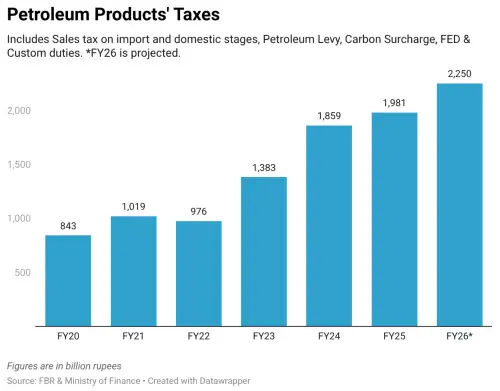

The dependence on petroleum taxation is entrenched. Over the past two decades, taxes on POL products, including GST at various stages, customs duties, federal excise, carbon surcharges and the Petroleum Levy, have averaged around 15 percent of total federal revenues, tax and non-tax combined. This is not a marginal stream. It is one of the largest revenue spinners available to the federal government.

That dependence distorts policy choices. It also sharpens the debate on tax equity. Sectors with significant GDP weight, such as wholesale and retail trade, contribute a negligible share to federal revenues. Estimates from FY25 place their contribution at around 0.38 percent. The imbalance is stark. Consumption taxes, particularly on fuels, continue to do the heavy lifting because broadening the base has proven politically and administratively difficult.

In such a setting, every pricing decision is overburdened. It is not just about cost recovery or subsidy rationalisation. It is about plugging fiscal gaps in real time. That is why the government reached for a record levy in the middle of a crisis. The fiscal side operates without buffers and under constant external scrutiny. When adjustments are needed, development spending is often the first casualty. Beyond that, there is little room.

Compounding the problem are the optics. Austerity is easier to sell when it is visible. Instead, the signal from the expenditure side remains weak. High profile spending, VVIP protocols, luxury private jets, and episodic symbolic gestures do little to build credibility. Temporary salary cuts or headline-grabbing announcements do not substitute for structural restraint.

The result is policy theatre. Big announcements. Abrupt reversals. Complex justifications. Limited trust.

The latest episode underscores a familiar conclusion. Pakistan’s fiscal architecture is overly reliant on a narrow set of easy-to-collect taxes. Petroleum sits at the center of that system. Until the tax base is broadened in a meaningful way, and until expenditure discipline becomes more than cosmetic, pricing decisions will continue to carry a burden they were never designed to bear.

The levy can be tweaked. Subsidies can be turned on and off. Formulas can be defended or criticised. None of that changes the underlying constraint. The state needs revenue, and it keeps going back to the pump to get it. That cycle has to break.

Comments