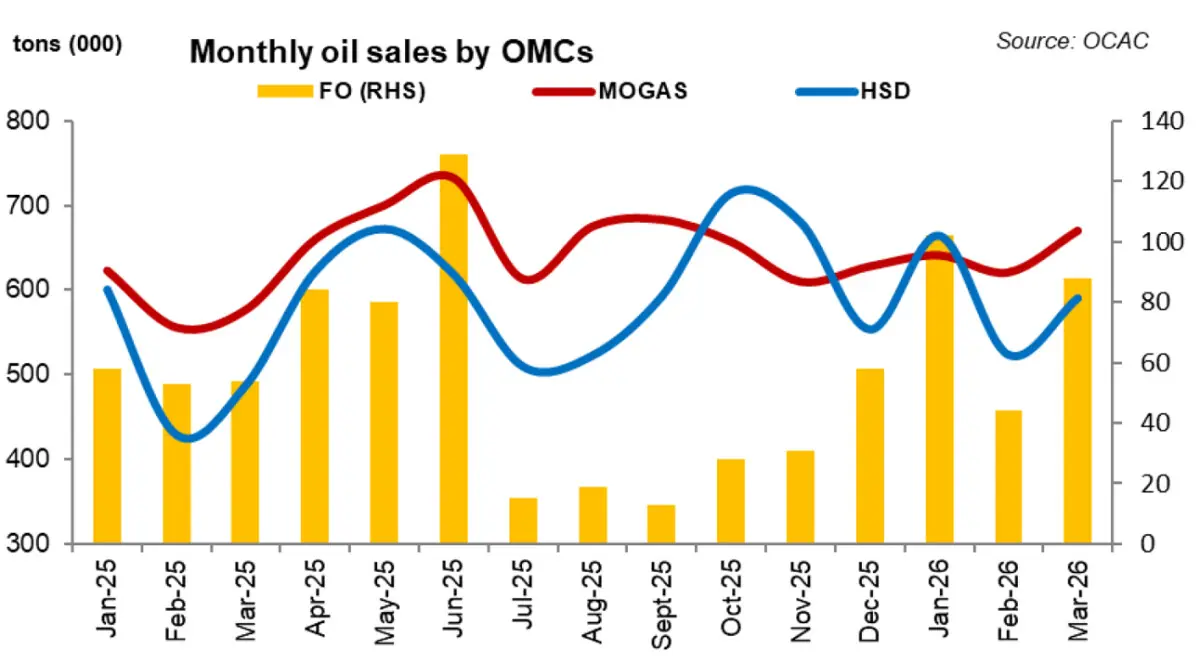

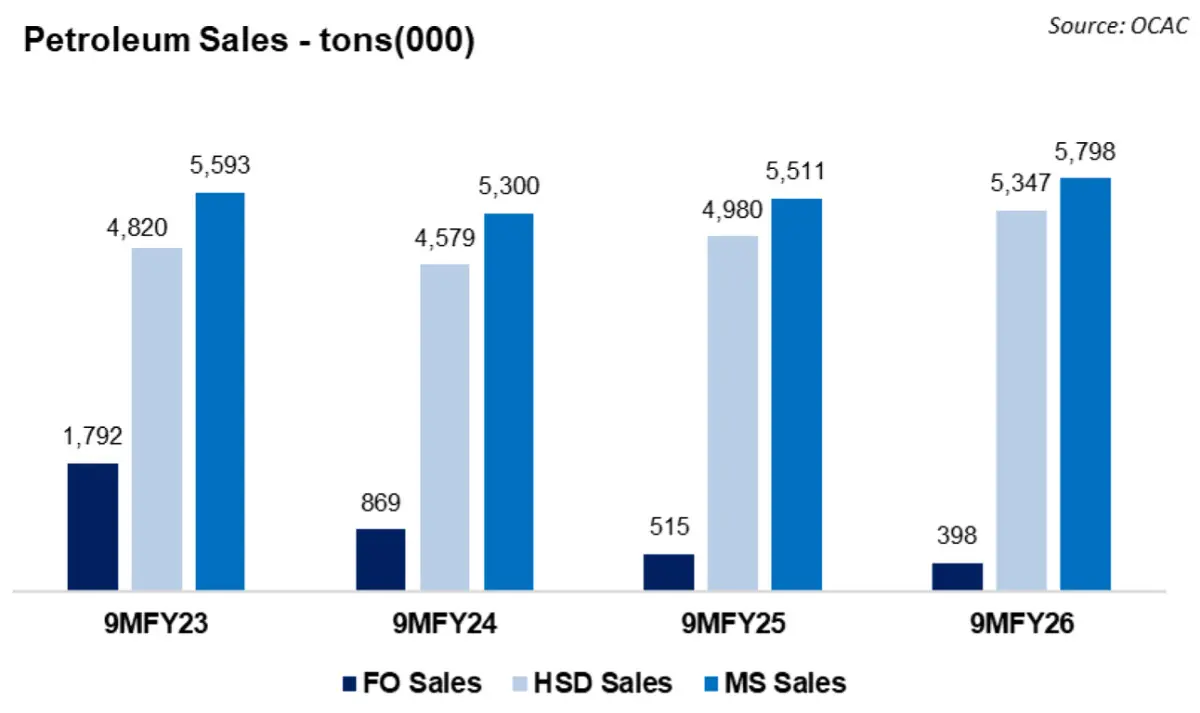

Pakistan’s oil marketing sales posted a sharp jump in March 2026, with total OMC volumes rising to 1.44 million tons, up around 19 percent year-on-year and 13 percent month-on-month. For 9MFY26, cumulative sales reached 12.40 million tons, up 5 percent over the same period last year. Excluding furnace oil, March sales also showed solid growth over both last year and the previous month.

At first glance, March looks like a strong month for petroleum demand. Motor spirit sales were up 16 percent year-on-year, while high-speed diesel climbed 21 percent. Over 9MFY26, MS and HSD volumes increased by a modest 5 percent and 7 percent, respectively, showing that white-oil demand remained fairly steady through most of the year.

But the March jump needs to be read with some caution. Demand did not necessarily improve materially; the rise in OMC volumetric sales was largely driven by panic buying and hoarding ahead of expected price hikes, fuelled by the Strait of Hormuz closure, supply concerns, and rumours of gasoline shortages.

In other words, some of the month’s offtake was likely timing-related: fuel was bought earlier, not necessarily used more.

Furnace oil sales rose sharply in March 2026, up nearly 62 percent year-on-year and 98 percent month-on-month, even though 9MFY26 FO sales were still down more than 23 percent overall.

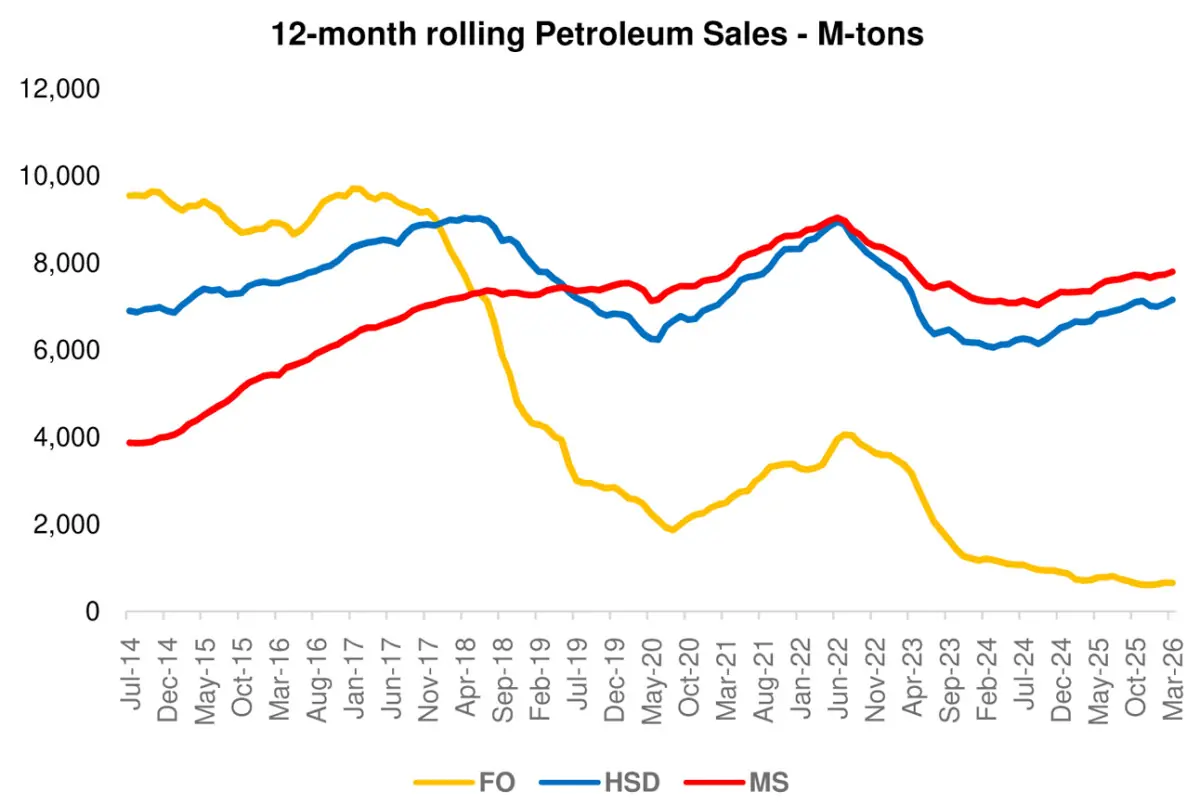

The likely explanation is not a structural recovery, but stress in the energy system. This appears to have been driven by RLNG disruptions and greater reliance on FO-based power generation during the ongoing geopolitical crisis. The 12-month rolling sales trend tells the same broader story: Pakistan’s petroleum market is now clearly white-oil led. MS and HSD remain the main demand drivers, while FO continues to decline structurally despite this temporary monthly spike.

The refinery side also suggests that the recent rise in demand was backed by real physical offtake. Overall refinery upliftment rose 13 percent year-on-year, while refinery production increased 13.9 percent, according to a research note by AHL Research. The note also highlighted an improvement in industry utilization in March 2026, with HSD and MS leading the increase.

However, this growth in consumption, especially in retail fuels, may not last. If high international prices continue to be absorbed through subsidies instead of being passed on to consumers, strong sales will come at the cost of a wider import bill, larger fiscal slippages, and rising macroeconomic stress.

The government will eventually have to withdraw the price differential claim subsidy, which would push fuel prices higher and weigh on volumes. One factor that could still provide some support to HSD sales, however, is the start of the wheat harvesting season.

Comments