BR RESEARCH: Power tariffs flatten; focus should move to investment

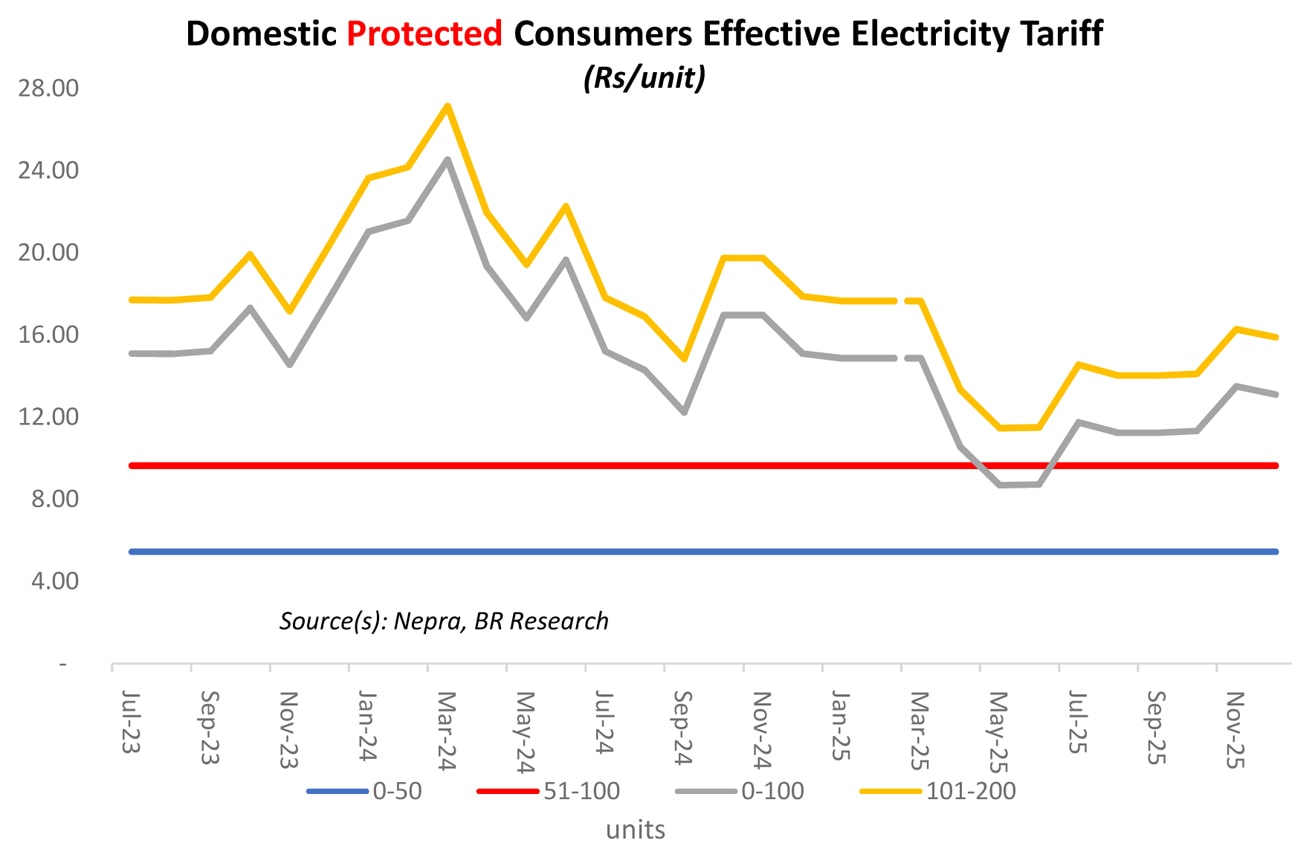

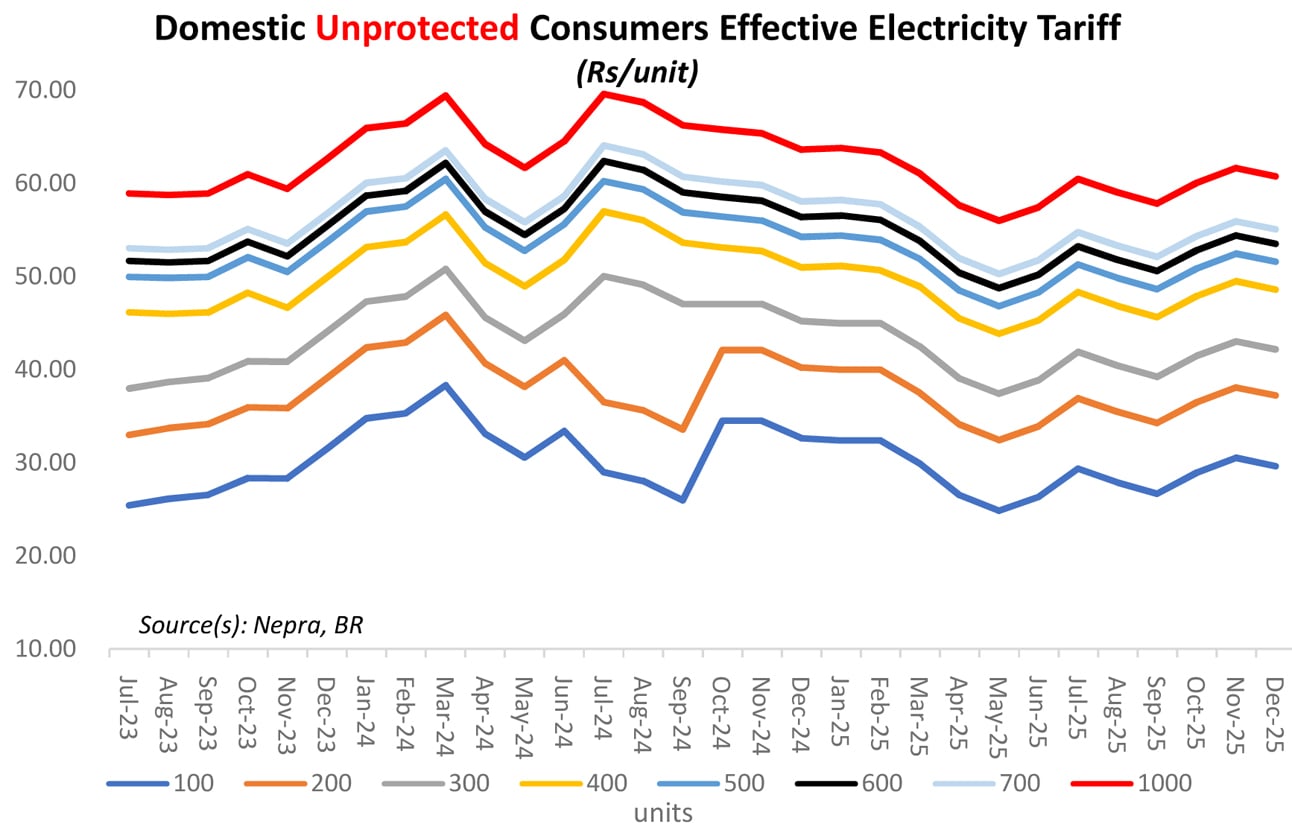

The power regulator Nepra announced both the quarterly and monthly Fuel Charges Adjustment last week, offering a collective Rs0.73/unit relief in December 2025, month-on-month. Recall that November 2025 effective consumer end tariffs had jumped month-on-month as the previous Quarterly Tariff adjustment (QTA) lapsed in October – and there was none in effect for November.

With negative Rs0.33/unit in lieu of QTA for December-February period now in place, respite is on the cards. The monthly FCA for December 2025 has been decided at negative Rs0.88/unit – adding another Rs0.4/unit cushion. On a year-on-year basis, every single month of 2025 will have returned negative change. For most month and most consumption slabs, 2025 effective tariffs have also stayed lower than 2023.

With the upcoming annual rebasing exercise pulled back from July to January – base tariff increase – if any will not be felt that hard, given the consumption profile for most consumers. The January rebasing is a part of many items on the reform agenda, on which phasing out the cross subsidy remains key. The IMF sets 2027 for the complete phase out of cross-subsidy, which could be a little optimistic, given it falls towards the end of the ongoing program. If history is any guide, following up on any reform measures almost always never happens, once the program ends (unless there is another one right after the current one).

The tariff program takes care of most cost pass-on, and in time too, as evident from negligible buildup in circular debt stock. The underperformance on account of distribution losses and billing recovery continues to be the key contributor towards inefficiencies. A large part of circular debt stock is planned to be serviced by the Debt Servicing Surcharge for the next six years. In all essence, circular debt going out of control, with full cost pass-on, phased subsidy rollout and high DSS, should take an unbelievable level of ineptitude.

The focus then shifts on to demand management to keep the financial health of the power sector on strong footings. On one hand, the transition of captive power plants to the grid has been a rather smooth process – with up to 40 percent increase in consumption reported from the industries year-on-year. This brings back the best paying consumers to the grid – and also improves the load profile. There is the incremental consumption incentive package to top it off, that goes into effect from the ongoing month for three years. While the industries have shared the reservations on a number of issues – it should still lead to increased demand from industries.

On the other hand, there is the rapidly changing demand dynamics from the domestic sector. With solar boom in full swing, the grid faces immense pressure on technical grounds. The electricity reform agenda demands a shift from pricing front to transmission investment and demand management fronts. The authorities must ensure sufficient investment goes in the system to keep the grid from being a victim of sudden sharp fluctuations in demand and generation profiles. There is also a need to push for more electricity usage, outside the usual demand centers.

Copyright Business Recorder, 2025

Comments