For the second quarter running, MCB Bank Limited’s (MCB) Investment-to-Deposit Ratio (IIDR) and coverage ratio stayed neck to neck. This is a rare occurrence, but such has been the reluctance to lend to anyone other than the government that virtually all increase in deposits is parked in government securities.

And when that doesn’t satiate the appetite, there are always borrowings to be had from the open market operations.

Not that anyone is complaining. The shareholders walked away with another interim cash dividend to the tune of Rs9/share – taking the year-to-date payout to Rs27/share. The Bank posted a near 8 percent year-on-year decline in pre-tax earnings for 9MCY25, which is remarkable given the pace of monetary easing that took a big chunk out of net markup income – which slid nearly 6 percent year-on-year.

The decline was arrested by a staggering deposit mobilization drive – that yielded an exceptional 29 percent increase in current account deposits over December 2024 – and 21 percent higher on an average basis.

The 16 percent increase in the overall deposit base was singlehandedly carried by current accounts – that made up almost 90 percent of all deposit increases during 9MCY25 – adding Rs272 billion.

Exceptionally improved CASA ratio led to further improvement in the cost of deposits – which proved critical, especially as non-core income growth remained subdued.

The non-markup income moderated 3 percent year-on-year, primarily on account of stiffer competition in the remittance business. Branch banking, card business, dividend income, and foreign exchange income all reported healthy year-on-year growth.

On the cost side, a 15 percent year-on-year increase, mainly attributed to talent development and technology, did dent the cost-to-income ratio from a year ago to nearly 38 percent.

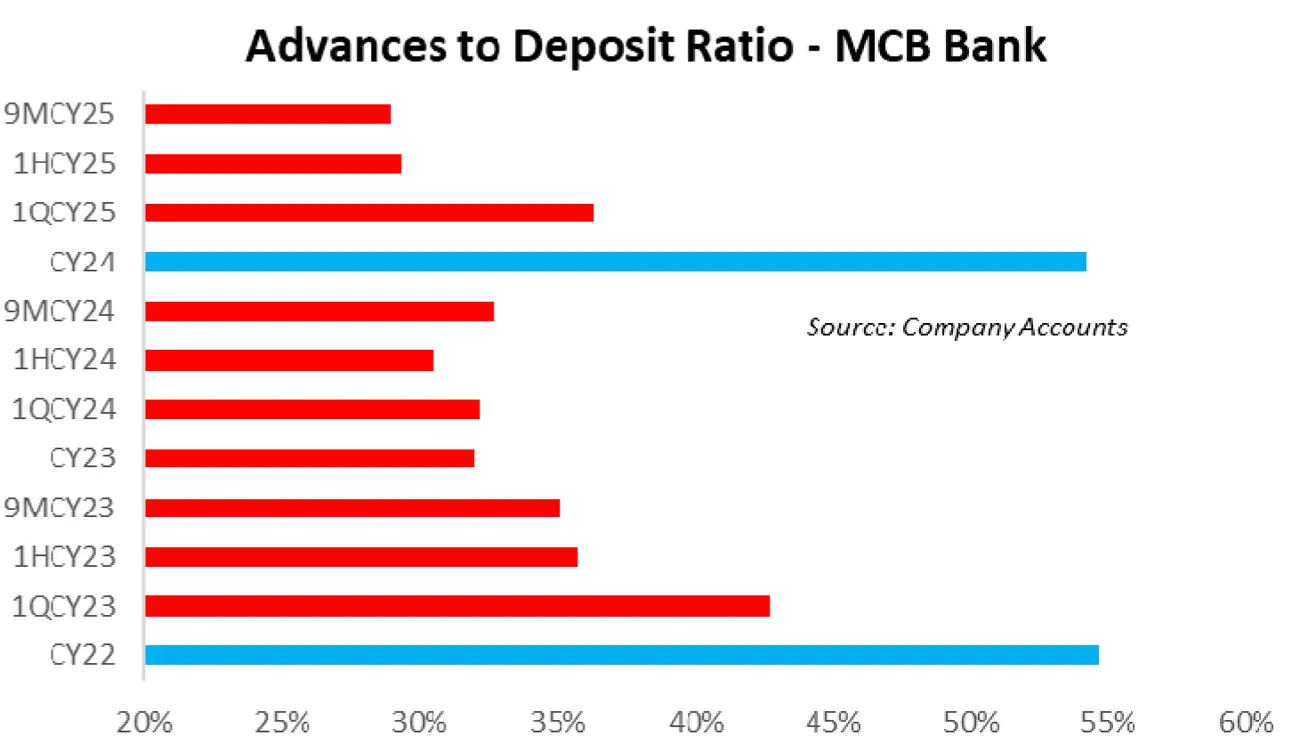

The balance sheet reprofiling has been at the center this quarter – and keeping up with the industry-wide trend, MCB intensified its exposure in government securities – with the investment portfolio jumping a massive 72 percent over December 2024. That is a small matter of over Rs840 billion more parked in T-bills and PIBs over December 2024. Keep in mind, deposits grew by a little over Rs300 billion all this while.

More investments also meant less lending to businesses. The gross advances portfolio at the end of September 2025 is even lower than three years ago – as the ADR slipped to a low 29 percent. The 4QCY24 advances boost was never going to last given the composition – and it has played out exactly as expected.

What happens in 4QCY25 is guesswork, but MCB and others have pulled a turnaround before, and there’s no reason they can’t pull it again to avoid the higher tax incidence in case of missing the 50 percent target. The lesser said about the quality of the 4QCY25 lending, the better. Nevertheless, the profits keep coming, and this is all that matters to those invested.

Comments

Comments are closed for this article.