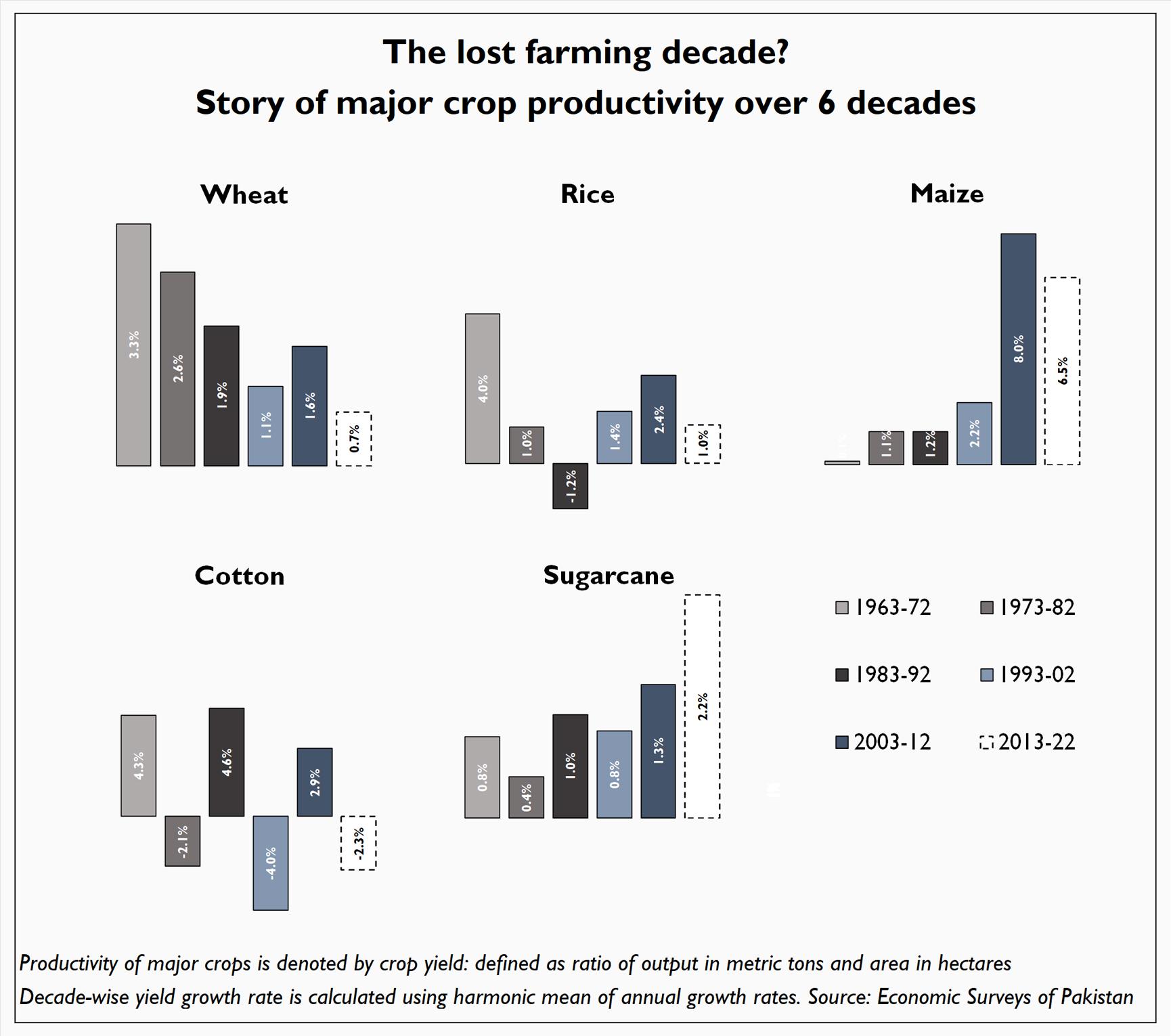

Revival of Pakistan’s agriculture is talk of town after major crops noted significant rebound during FY22. At 4.4 percent, the growth rate is highest in 17 years, and one of the few feathers in PTI’s cap. However, farming sector’s performance during the ongoing fiscal hardly masks its abysmal show over the last decade. In fact, the last 10 years (2013 – 22) could very well be dubbed the lost decade of Pakistan’s farming sector; at least the first since the 1960s.

Remarkably, the credit for this abysmal show goes equally to both PML-N and PTI, both of which draw electoral support from country’s farming heartland: Punjab. Out of five major crops, the three most important: wheat, rice and cotton – recorded their slowest decade growth rate in productivity. The productivity improvements have been so embarrassing that the share of these three crops in the Important Crops Index fell from 80 percent under old base to a little under 65 percent under the rebased GDP.

The two crops that did perform well and marked major leaps in productivity – maize and sugarcane – now occupy an oversized 35.2 percent share in the Index of Important Crops – in turn helping to pull sectoral GDP growth rate out of the woods during FY22 (under the new base). Farming sector’s flagship crops – wheat, cotton, and rice –now represent a major drag on agricultural productivity. Consider that out of the gross 17.5 million hectares cultivated under 5 major crops, 82 percent of land is utilized by the former three, while maize and sugarcane occupy just 2.9 million hectares. Sadly, those hardly aware of farming sector’s dynamics regularly vilify the latter two crops for replacing the traditional acres that formerly cultivated cotton.

Yet, even maize – which is now the biggest star of Pakistan’s farming sector and growers’ new darling crop – saw decade average productivity growth rate slowdown from 8 percent per annum during 2003 – 2012 to 6.5 per annum during 2013 – 2022. For all its bad rap, sugarcane remains the only crop which recorded highest decade average growth rate since 60s, rising to 2.2 percent per annum from 1.3 percent during the preceding decade – marking its supremacy in the era of climate change.

Before those in the corridors of power make promotion of pulses and oilseeds the focus of policymaking for the next decade, it remains imperative that they first focus on improving productivity in traditional crops. Pakistan’s largest crop wheat - which occupies 9 million hectares every year – saw its slowest decade average growth rate of just 0.7 percent p.a. during the last 10 years. The country may very well be able to switch from cotton to cane or maize. But future of food security in a 230 million headstrong nation will remain perpetually insecure unless it prioritizes investment in cereal/grain productivity on war footing basis.

Comments

Comments are closed for this article.