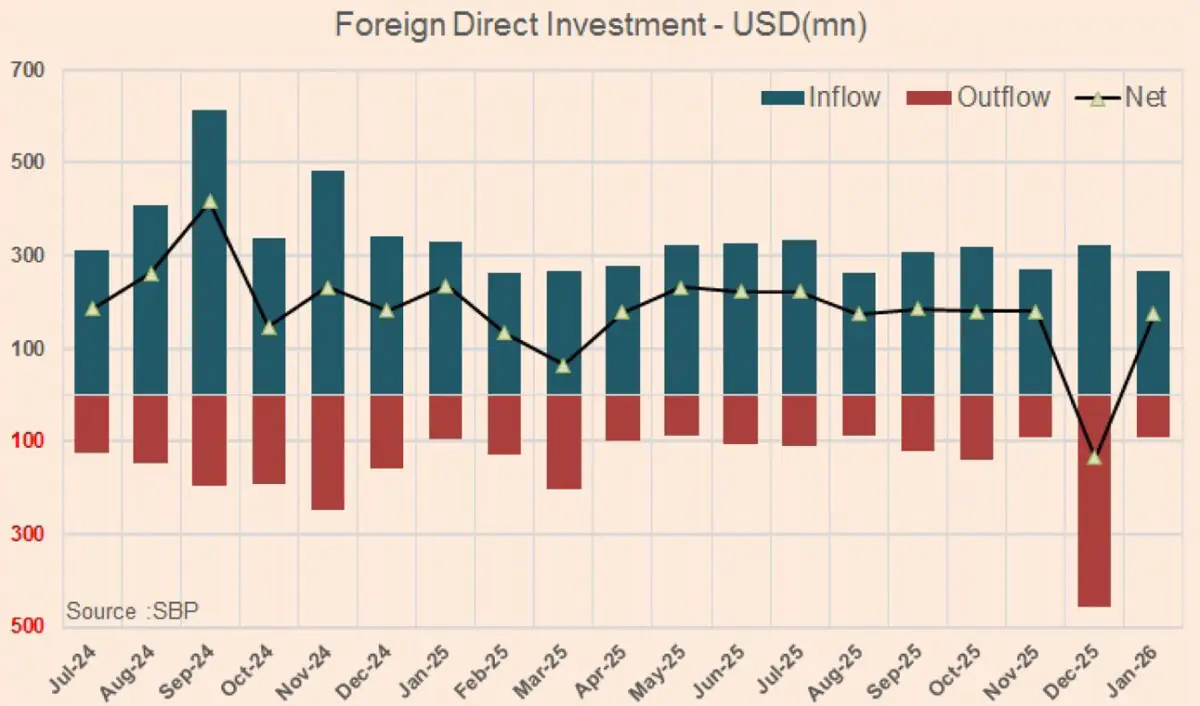

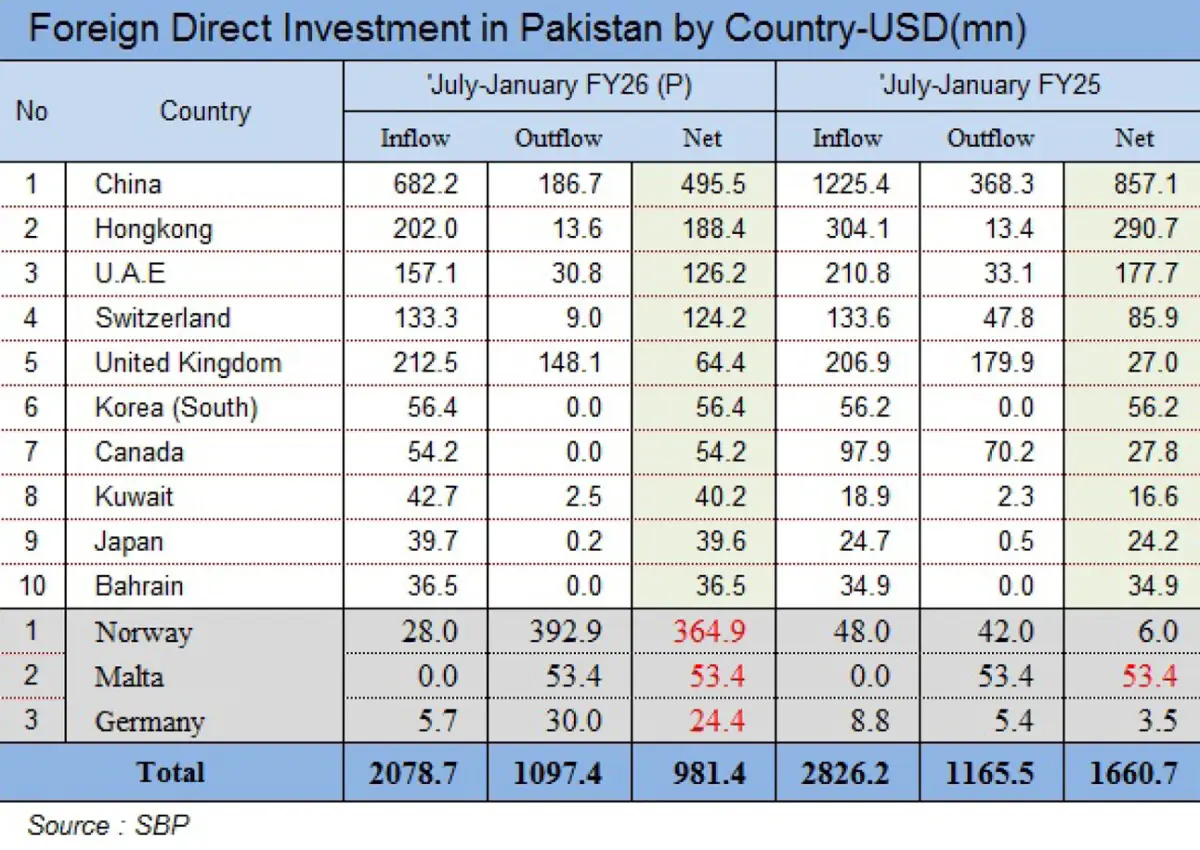

Pakistan’s net foreign direct investment (FDI) came in at $173 million in January 2026, down 27 percent year-on-year, as per SBP data. On a cumulative basis, net FDI stood at $981 million in 7MFY26, sharply lower than $1,661 million in 7MFY25, reflecting a 41 percent decline.

The broader trend remains unchanged: FDI is weakening, concentrated, and undiversified, with no meaningful momentum visible in recent months. Pakistan’s inflows continue to depend on a narrow set of countries and sectors, making the overall profile fragile.

Country-wise, China remained the largest source in 7MFY26 at $496 million, but well below $857 million last year. Other key contributors were Hong Kong, UAE, and Switzerland, but the list thins out quickly beyond the top few.

Meanwhile, net outflows were recorded from countries such as Norway, Malta, and Germany, showing that Pakistan is not only attracting less capital but also seeing exits.

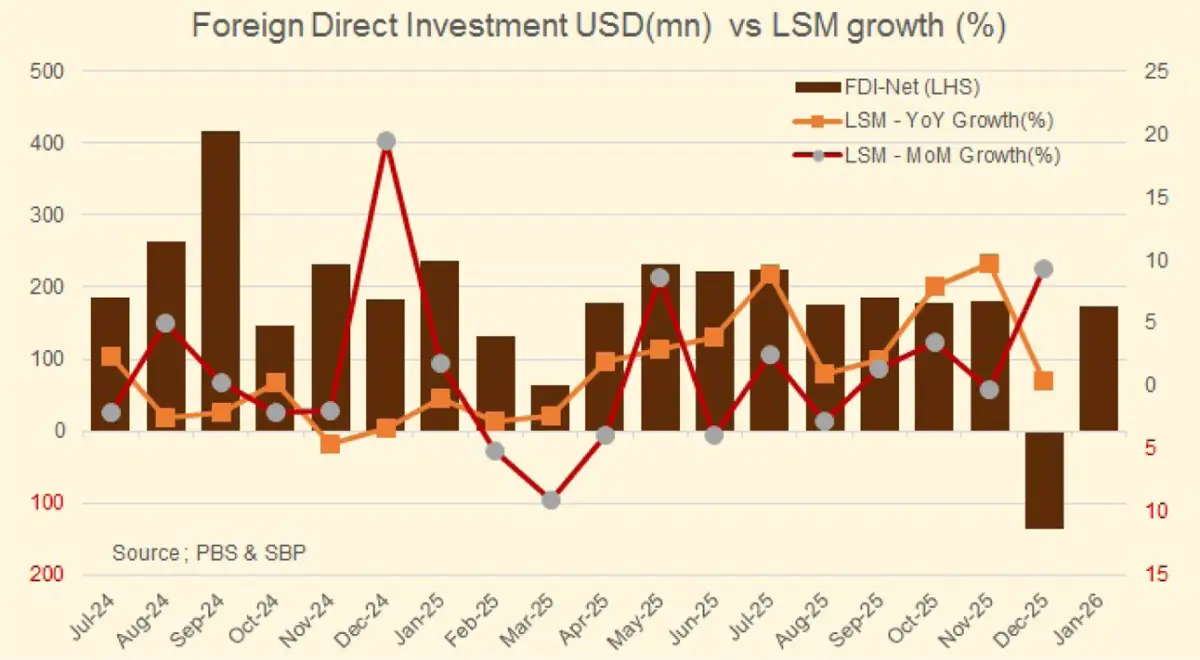

The divergence between LSM and FDI is now a defining feature. Industrial activity has started improving, with LSM growing 6 percent in Jul–Nov FY26, and Nov-25 alone up 10.4 percent year-on-year.

In contrast, FDI continues to fall, suggesting the industrial recovery is being driven mainly by domestic demand and local manufacturing, not fresh foreign capital. Foreign investors appear to remain cautious due to a persistent geopolitical risk premium, despite signs of stabilization.

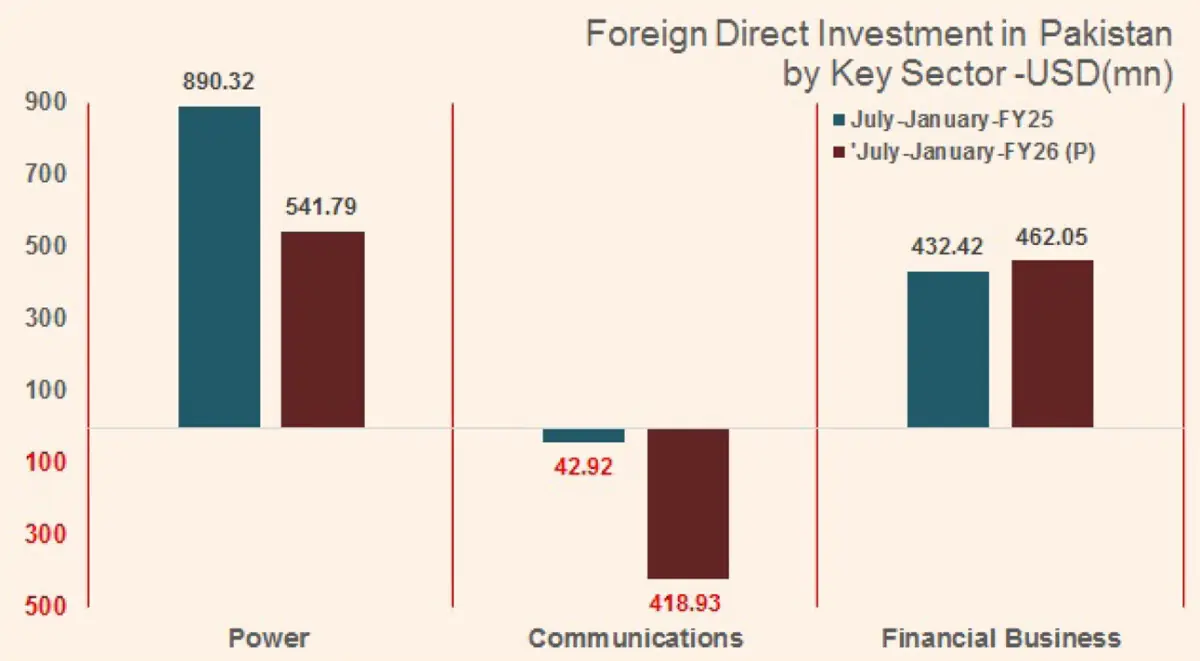

Sectoral data reinforces the mismatch. While automobiles, cement, and petroleum have supported LSM recovery, FDI remains concentrated in non-tradable sectors—mainly Power ($542 million) and Financial Business ($462 million).

Meanwhile, Communica-tions has shifted into net outflow, pointing to restructuring and exits rather than new investment.

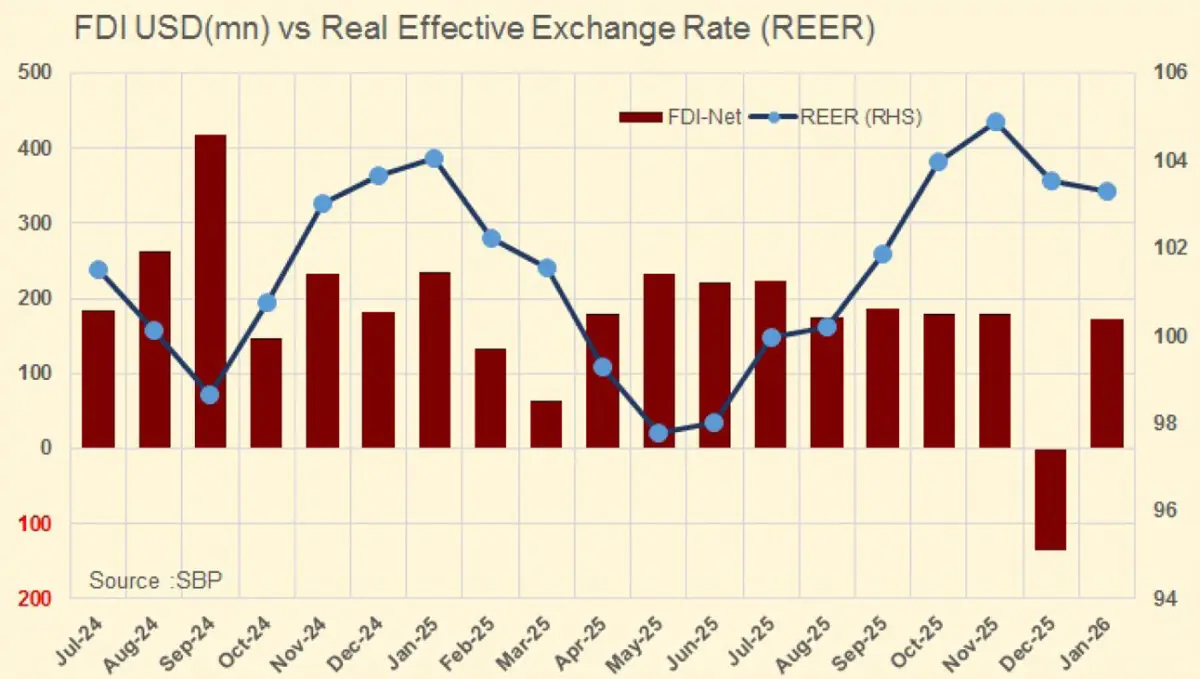

The REER picture adds another layer. As of Jan-26, the REER stood at 103.29 and has remained above 100 for the last six months, signalling a relatively strong rupee in real terms. A REER above 100 typically discourages export-oriented FDI, as it raises production costs in dollar terms for foreign manufacturers.

At the same time, a stronger REER improves repatriation value for existing investors. Profit repatriations hit a record $1.56 billion in 1HFY26. This creates a structural imbalance: the same sectors attracting FDI—Power and Finance—are also among the biggest repatriators.

While repatriation supports confidence by showing investors can take profits out, it also creates a drain on reserves. With FDI declining and outflows rising, Pakistan is increasingly becoming a net exporter of capital, leaving external stability dependent largely on remittances.

Overall, Pakistan’s Jan-26 FDI and 7MFY26 trend confirm a key reality: the economy may be stabilizing and LSM may be recovering, but foreign capital is not buying into the rebound.

Comments