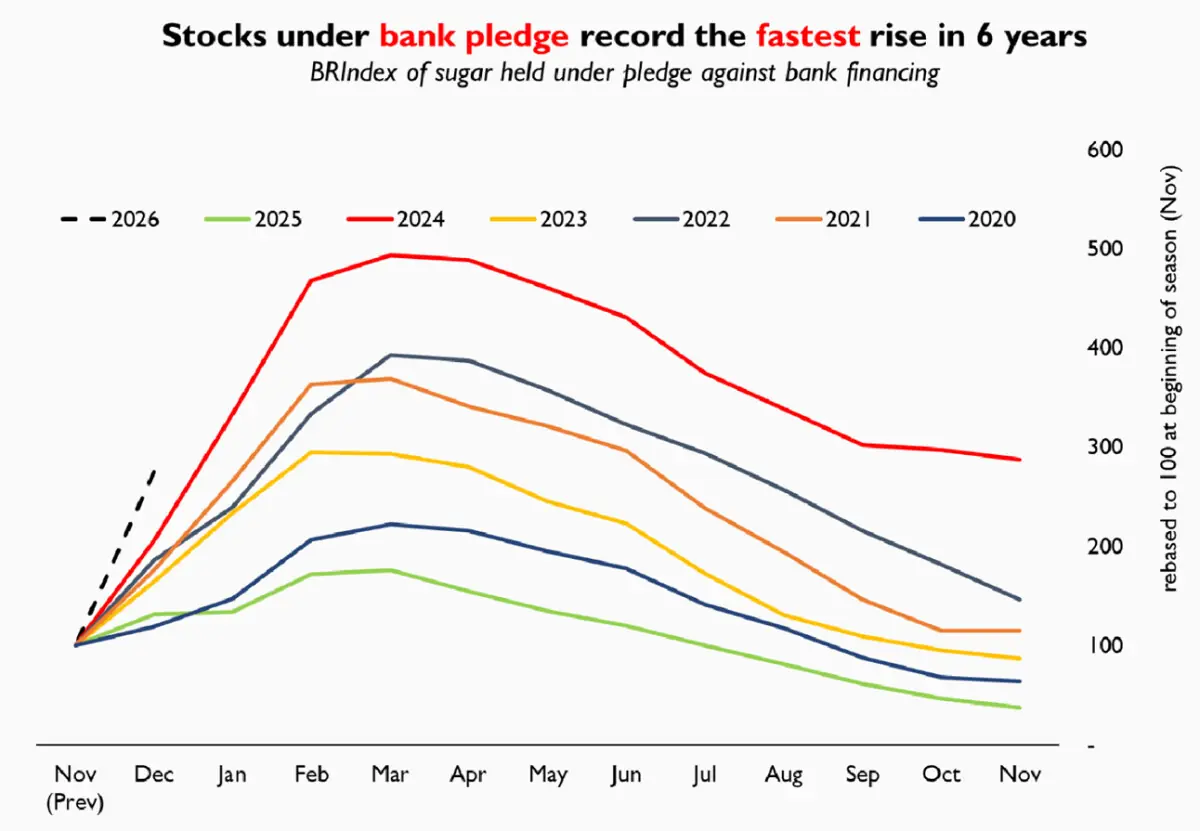

If December 2025 banking advances data is to be believed, Pakistan’s sugar sector may finally be doing what it does best when left alone: produce.

Bank pledge figures show a spectacular rise in December 2025, a clear signal that crushing has picked up pace and sugar production is flowing into inventories.

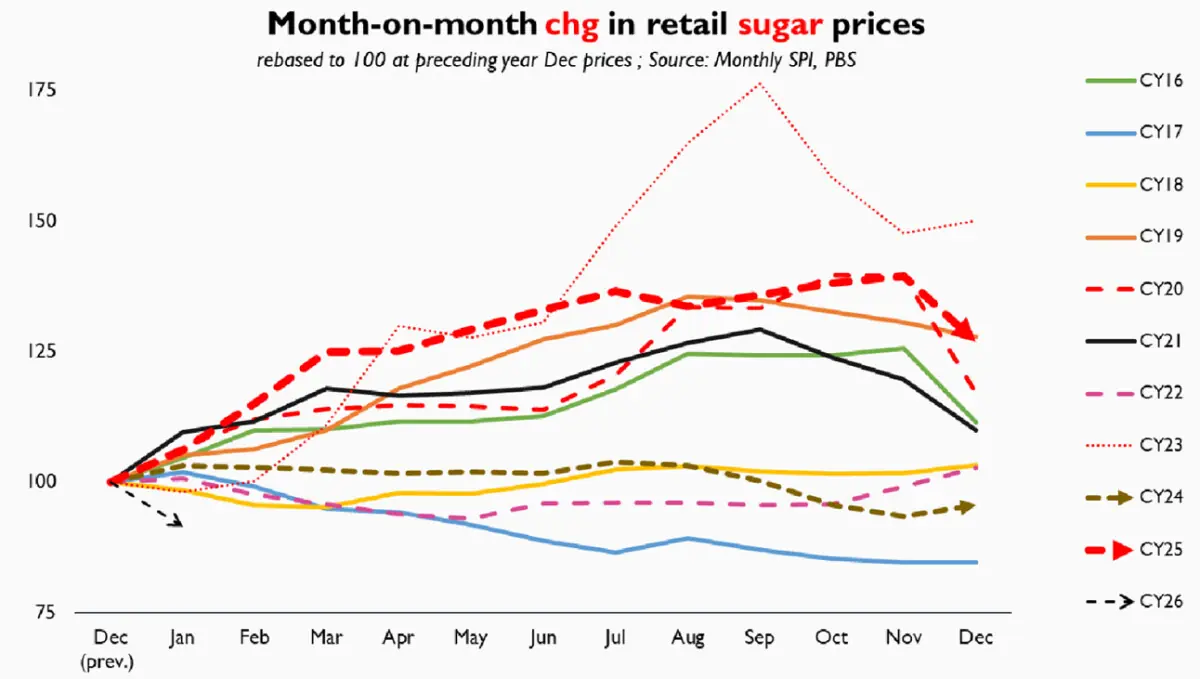

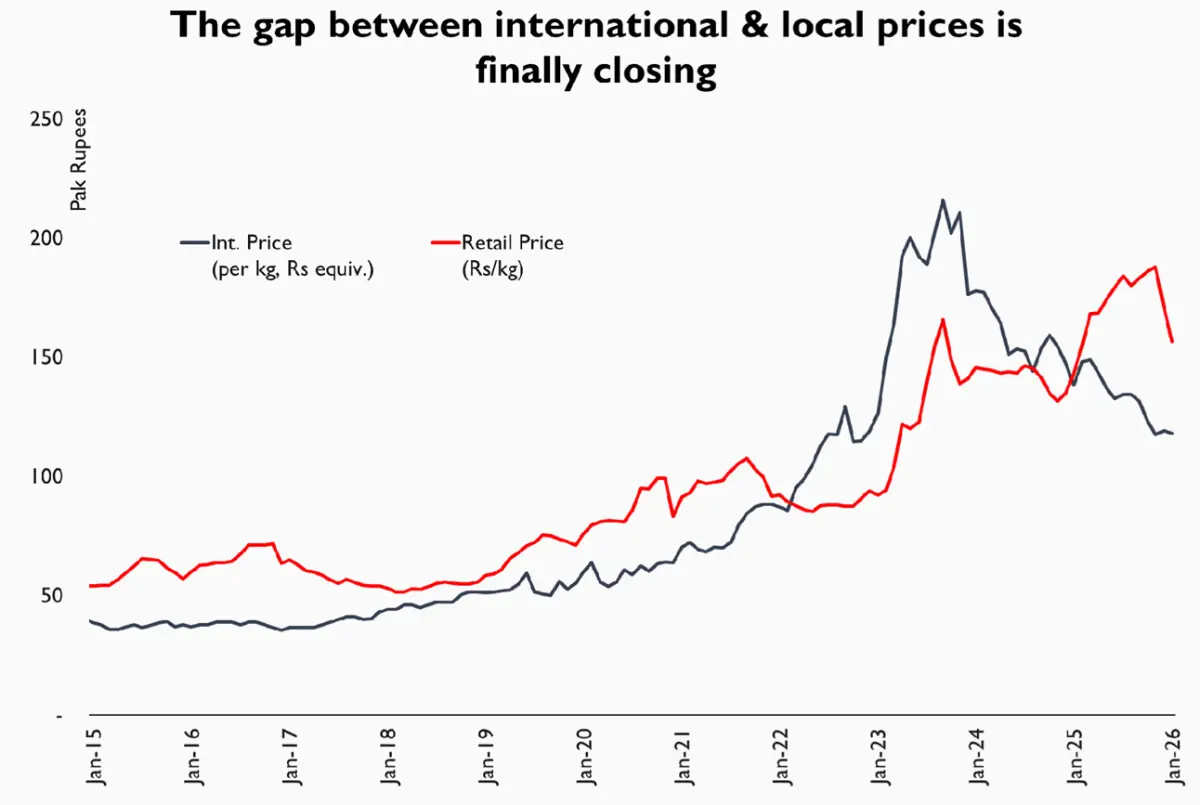

Retail prices, which had remained stubborn through much of 2025, have begun to ease since December and carried that momentum into January 2026. For the first time in months, the market is showing signs of release rather than resistance.

This matters because the floods of monsoon 2025, while disruptive, were never meant to be a verdict. Cane harvesting began early this season in November andshall run through April 2026. The industry is very much in the middle of the season, not at its conclusion.

Early fears of acute shortage could prove to be premature. December’s inventory surge could only be the beginning, and the supply may become more visible and peak consumption season unfolds earlier this year beginning Ramzan all the way to summer.

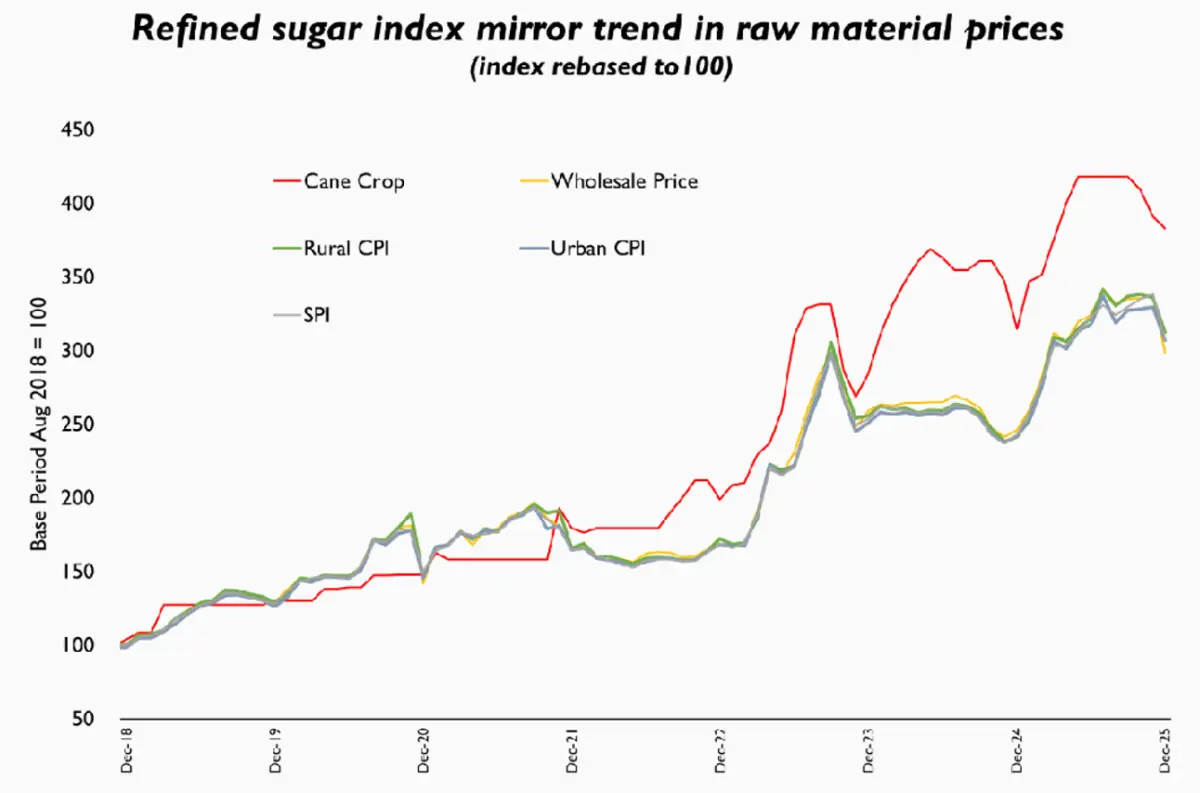

The question, as always, is what happens next.History urges caution. In previous cycles, rising production did not automatically translate into cheaper sugar. Stocks are built, pledged, and held back, allowing prices to stabilize at elevated levels rather than correct meaningfully.

But this season carries a subtle difference. Prices have already started to decline, not merely plateau. That suggests that the current inventory build-up is not yet being used to enforce scarcity. At least for now, supply appears to be making its way through the system.

Still, it is too early to declare a surplus year. A December spike in pledged stocks can mean two very different things. It can signal a genuine production upswing that eventually overwhelms domestic demand, forcing prices lower as the season progresses. Or it can signal front-loaded crushing combined with inventory finance – an increasingly permanent feature of the crushing season - setting the stage for controlled release later in the year.

READ MORE: Pakistan decides to fully deregulate sugar sector

The difference will become clear only by late March, when the bulk of the crop has been processed and the industry’s appetite for holding inventory is tested.

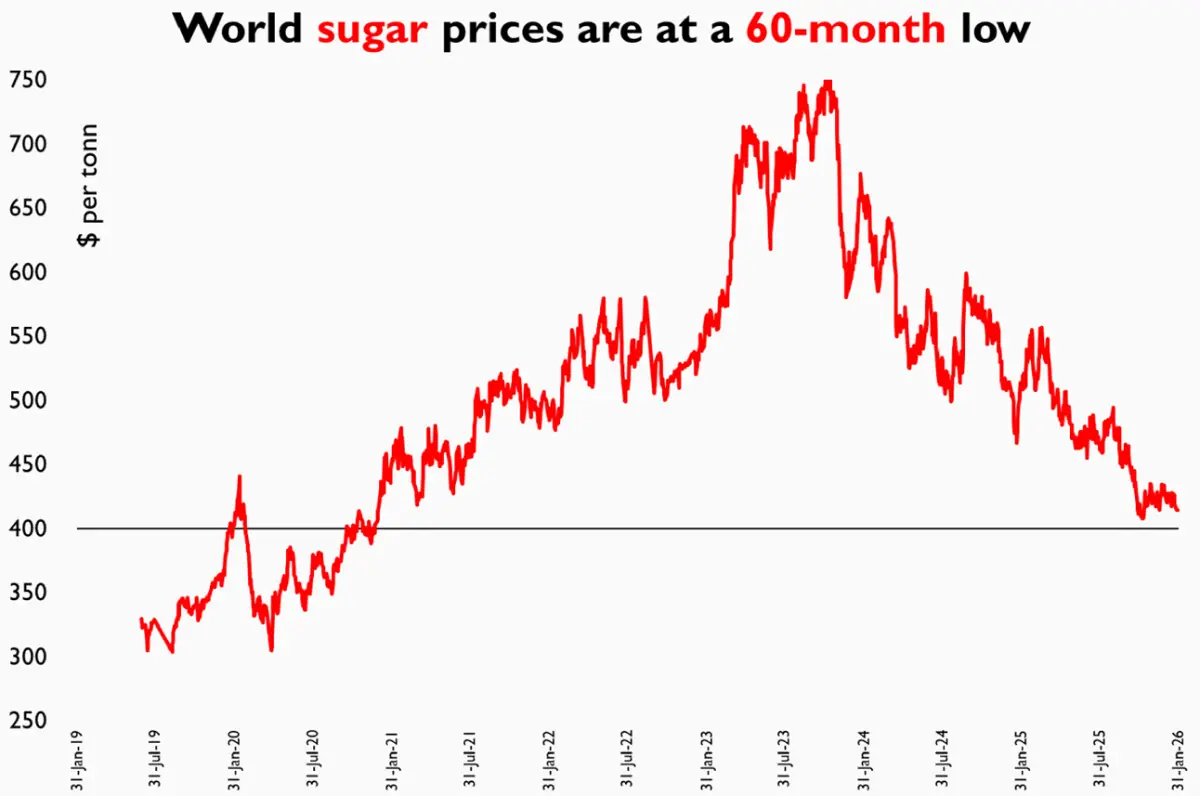

Global conditions are also unusually supportive. International sugar prices remain at multi-year lows, limiting the industry’s ability to argue for export-driven relief or parity-based price defense. Imports remain available as a backstop, even if they are not being actively deployed. In other words, the usual external justifications for domestic tightness are weaker than they have been in years.

That leaves domestic behavior as the swing factor.If production continues at the current pace and inventories keep rising well into April, Pakistan could well end the season with surplus supply.

In that case, price softening would likely continue, testing the industry’s tolerance for margin compression.

Alternatively, if inventory accumulation slows and pledged stocks become a tool for timing release rather than clearing supply, the market could settle into a familiar equilibrium of balance without relief.

For now, the most honest forecast is conditional, as data supports neither crisis nor complacency.

The sugar market is moving, not freezing as prices continue to ease without altogether collapsing. Whether this turns into a surplus year by summer, or merely a year of managed balance, will depend less on weather and more on whether supply is allowed to behave.

Comments