Pakistan State Oil (PSX: PSO) is Pakistan’s largest oil marketing company by market share and operates across the full range of petroleum products, including motor gasoline, high-speed diesel, furnace oil, jet fuel, kerosene, LPG, lubricants, and petrochemicals.

The company runs the country’s largest fuel distribution network and remains a key importer of Mogas, HSD, JP-1, and furnace oil, giving it a significant role in ensuring fuel availability.

As the energy mix evolves, PSO has begun broadening its focus beyond traditional fuels, with investments in infrastructure, selected renewable initiatives, exploration and production, and technology upgrades. These efforts reflect a gradual shift to adapt to structural changes in Pakistan’s energy sector rather than a departure from its core oil marketing business.

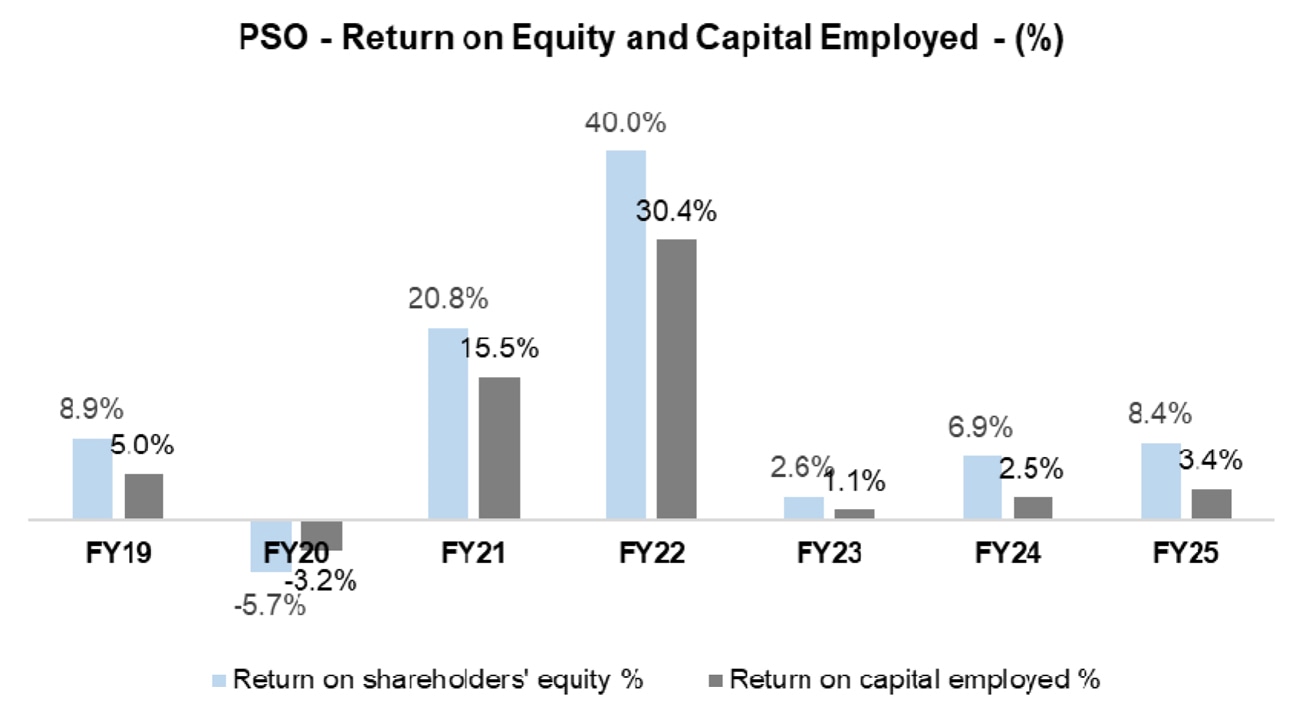

Historical financial performance

The downstream oil and gas sector has experienced significant fluctuations in demand in recent years, driven largely by the impact of COVID-19 and a shift in the energy mix—particularly the transition from furnace oil to coal and RLNG. As the industry leader, Pakistan State Oil (PSO) has consistently been at the forefront of shaping sectoral trends.

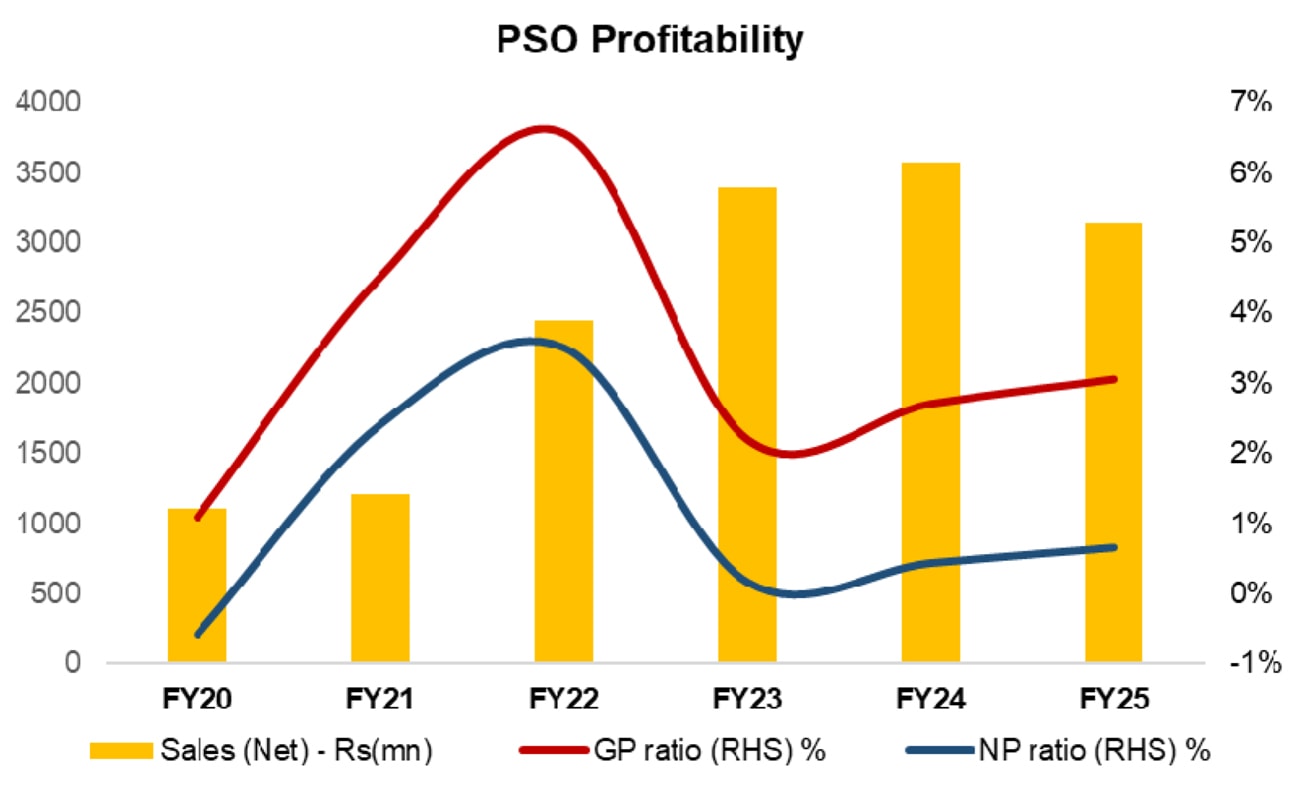

In FY17, PSO posted 8 percent growth compared to a range of -9 to 4 percent over the previous six years. This performance was supported by higher product volumes and prices, as well as its RLNG business, resulting in a 30 percent increase in sales revenue and a 77 percent rise in profits.

Volumetric growth continued in FY18, especially in motor spirit and high-speed diesel (HSD), though furnace oil volumes declined by 29.6 percent due to the energy transition. Despite a 20 percent increase in revenue, net profit fell by 15.2 percent, attributed to a one-time deferred tax reversal, reduced other income, and elevated exchange losses.

FY19 proved challenging for oil marketing companies (OMCs), with an economic slowdown, increased competition, shrinking margins, and declining sector volumes—particularly for furnace oil and diesel. High interest rates, exchange losses, mounting circular debt, and growing receivables further strained the industry.

While PSO’s overall sales volumes fell by 38 percent, revenues rose slightly in the final quarter due to a recovery in volumes. However, profit declined by 32 percent, weighed down by inventory losses, lower volumes, and higher finance costs. A key milestone in FY19 was PSO’s acquisition of a 52.67 percent stake in Pakistan Refinery Limited (PRL), which contributed to consolidated earnings.

In FY20, furnace oil volumes continued to shrink due to RLNG's increasing role in the energy mix. Although industry-wide demand was contracting, PSO managed to grow its petrol volumes. Diesel volumes, however, were hit by reduced industrial and construction activity and limited transportation.

Gross profit declined due to inventory losses stemming from falling international oil prices, while higher finance costs further dented profitability. These losses were partially offset by lower exchange losses and higher interest income from recoveries in the power sector.

FY21 marked a strong turnaround, with PSO posting record earnings. Revenue grew by 9 percent, backed by volumetric growth and improved pricing. Furnace oil re-entered the energy mix, resulting in a 24 percent increase in total volumes.

Motor spirit, HSD, and furnace oil grew by 21 percent, 21 percent, and 37 percent, respectively. The introduction of Euro-5 compliant fuels boosted sales. Additionally, increased other income from late payment surcharges and lower finance costs due to declining interest rates supported profitability.

In FY22, PSO delivered exceptional performance, driven by strong topline growth and significant inventory gains from rising oil prices. Product volumes for motor spirit, HSD, and furnace oil rose by 15 percent, 26 percent, and 62 percent, respectively, helping PSO grow its market share. Gross profit growth was notable, supported by a 32 percent increase in delayed payment interest.

Operating profit surged by 183 percent, and net profit nearly tripled, fuelled by higher volumes, inventory gains, elevated prices, and an expanded retail footprint—solidifying PSO’s market dominance.

In FY23, PSO’s revenue rose by 38 percent year-on-year, but the increase was driven solely by higher petroleum prices. Volumetric sales of key products declined sharply—motor spirit by 17 percent, diesel by 25 percent, and furnace oil by 64 percent. Petroleum product sales, which had been robust in FY22, reached their lowest level in five years due to the economic downturn, political instability, and flash floods.

PSO’s gross profit declined in FY23 due to inventory losses and weaker sales, with gross margins dropping to 2.21 percent—down more than 400 basis points year-on-year. While provisions on financial assets were reversed and other expenses were reduced, weak gross profits led to a fall in operating margins.

Other income dropped by 46 percent, reflecting lower interest on delayed payments. Finance costs surged eightfold, and PSO reported a share of loss from associates—resulting in a 93 percent drop in unconsolidated profit to Rs12 billion, compared to Rs184 billion in FY22.

In FY24, PSO delivered remarkable financial and operational performance in FY24, with earnings surging by 180 percent year-on-year—despite challenges faced in the preceding quarter.Revenue grew by 5 percent year-on-year, reaching Rs3.6 trillion, primarily driven by higher average selling prices of petroleum products, including Motor Spirit (MS) and High-Speed Diesel (HSD) - despite a 9 percent decline in overall sales volumes, with HSD and MS volumes falling by 8 percent and 1 percent, respectively, and furnace oil (FO) sales plummeting by 76 percent year-on-year.

Gross profit increased by 30 percent year-on-year, although gross margins remained modest at 2.72 percent, reflecting the impact of inventory losses due to fuel price volatility. A significant uplift in profitability came from other income, which rose by 74 percent year-on-year—driven largely by interest on delayed payments. Notably, in 4QFY24, other income increased fivefold. However, finance costs also rose by 30 percent year-on-year, owing to higher short-term borrowings.

Financial performance of FY25

PSO closed FY25 with earnings up 32 percent year on year to Rs21 billion, delivering a strong bottom-line recovery despite a 12 percent decline in revenues to Rs3.15 trillion. The topline contraction reflected lower petroleum prices and weaker volumes, with motor spirit down 4 percent, high-speed diesel down 5 percent, and furnace oil plunging 47 percent year on year, partially offset by stability in the RLNG segment where PSO managed over 110 cargoes during the year.

Margin management drove earnings improvement. Gross margins rose to 3.1 percent from 2.7 percent in FY24 due to lower inventory losses. Finance costs declined 36 percent year on year, supported by lower interest rates and reduced borrowings.

Taxation remained a key drag, with an effective tax rate of around 60 percent in FY25 (FY24: 62 percent), keeping net margins thin at 0.7 percent versus 0.4 percent last year. PSO maintained a Rs10 per share dividend, implying a payout ratio of 22 percent, while trade debts improved to Rs437 billion by end-June 2025. Overall, FY25 reflected a recovery in earnings despite subdued operational momentum.

PSO in FY26 and beyond

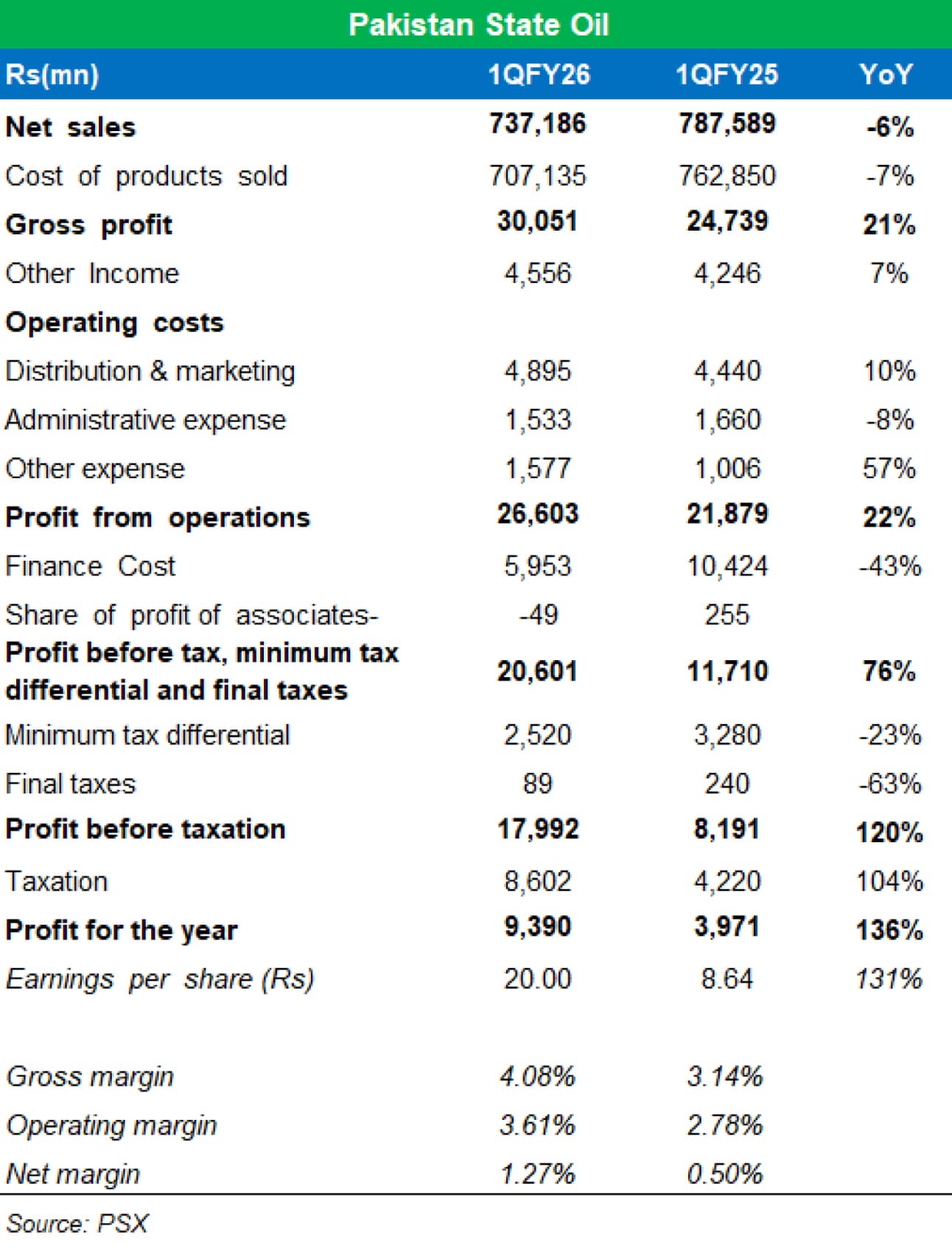

The OMC giant posted a strong start to FY26, with 1QFY26 profits more than doubling year on year, driven by higher inventory gains, sharply lower finance costs, and an improved liquidity position. This performance was achieved despite a 6 percent decline in net revenue, largely reflecting weaker RLNG pricing.

During the quarter, gross margins expanded to 4.1 percent from 3.3 percent in 1QFY25, while finance costs fell 43 percent year on year on the back of lower interest rates and reduced short-term borrowings. Other income rose 40 percent, supported by compensation on line-fill costs and tighter working capital management.

Operationally, core fuel demand remained resilient, with motor spirit volumes up 1 percent and high-speed diesel volumes up 6 percent year on year, although RLNG volumes stayed subdued. Liquidity improved meaningfully as receivables declined following partial clearance of power sector circular debt and timely payments from the gas company, easing working capital pressures and further reducing borrowing needs.

The outlook for the remainder of FY26 remains positive. A proposed OMC margin increase by OGRA, if approved, could provide a material earnings uplift in the second half of the year. With liquidity improving through power and gas sector settlements, gross margins at a two-year high, and finance costs at multi-quarter lows, PSO appears well-positioned for further profitability gains.

Comments

Comments are closed for this article.