Oil Marketing Company (OMC) sales recorded a pronounced slowdown in Nov-25, with total industry offtake falling 10 percent year-on-year to 1.42 million tons.

The decline was broad-based and driven primarily by high-base effects, border disruptions, and persistent price sensitivity across key fuel categories. Nov-25 was always expected to be a difficult comparison because November 2024 had marked a 25-month peak in OMC volumes, reflecting price stability and strict crackdowns on smuggling at the time.

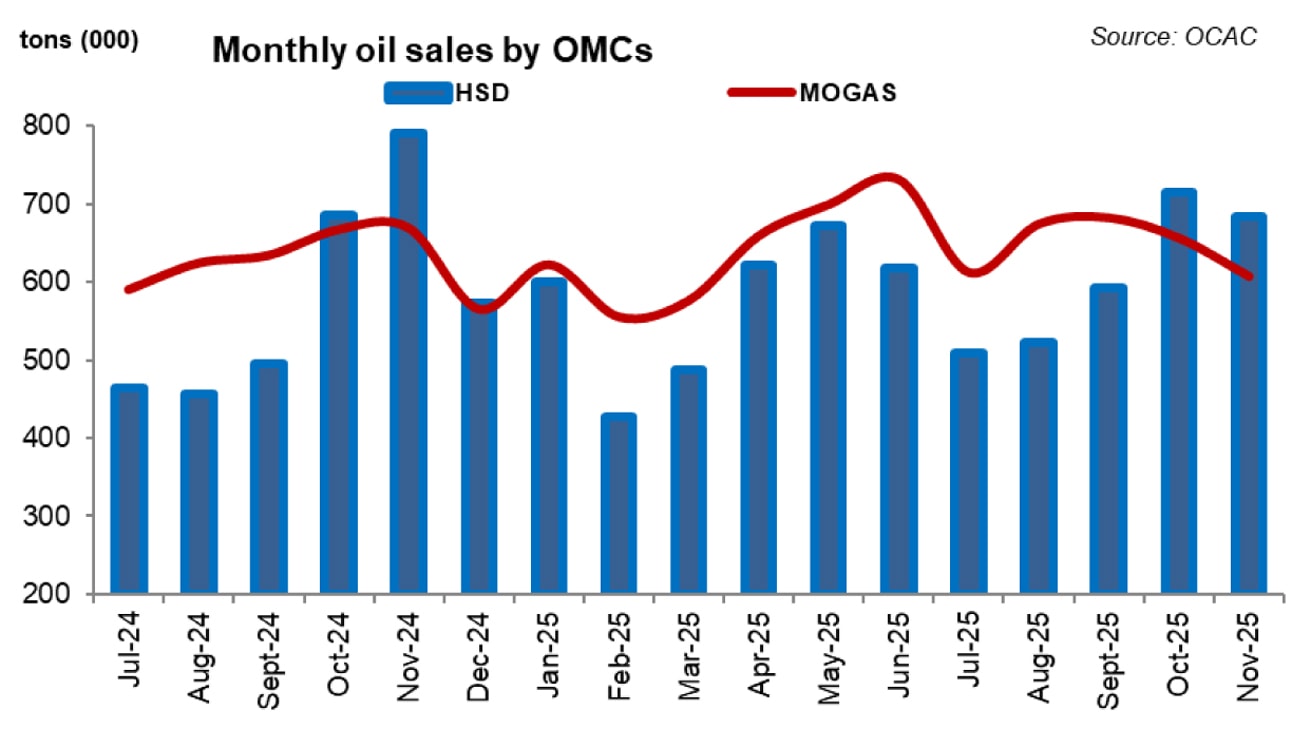

Against that backdrop, demand in Nov-25 appeared weak, with ex-furnace oil (Ex-FO) sales falling 9 percent year-on-year and total sales also slipping 5 percent month-on-month. Within product segments, High Speed Diesel (HSD) volumes declined 13 percent year-on-year as freight movement remained subdued due to western border closures, weaker cross-border trade, and reduced activity of heavy commercial vehicles. Rising diesel prices—now averaging Rs281.44/litre, up from around Rs250/litre in July—further weighed on consumption and contributed to higher smuggling incentives.

Motor Spirit (MS) sales also weakened, falling 9 percent year-on-year (and 7% MoM) as sticky pump prices and seasonal winter demand softness curbed consumption; retail MS prices remained roughly 7 percent higher compared to last year.

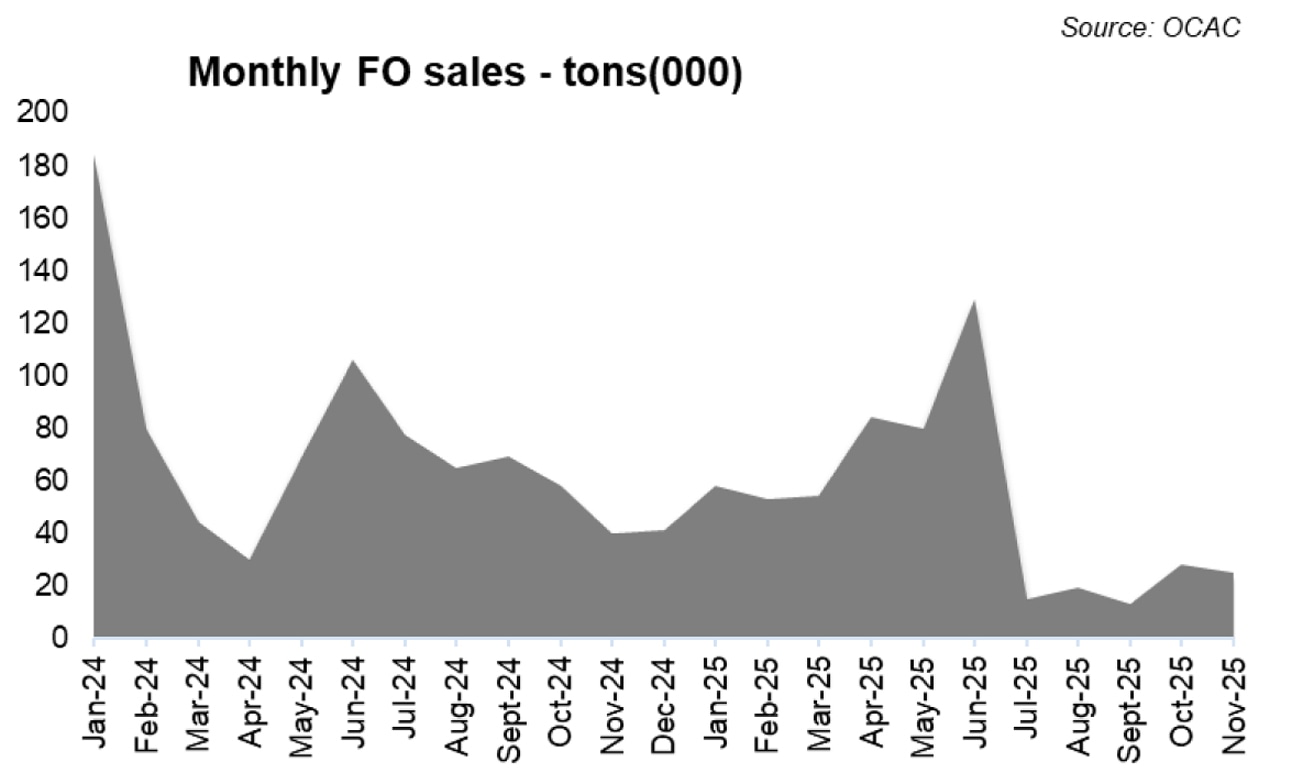

The steepest decline was seen in Furnace Oil (FO), where sales dropped 32 percent year-on-year due to reduced reliance on FO-based power generation, continued crowding out by cheaper alternatives in the merit order, and the imposition of a Rs77/litre Petroleum Development Levy (PDL).

The only bright spot was HOBC, which rose 78 percent year-on-year, reflecting continued SUV penetration, premium fuel demand, and smaller delta with MS.

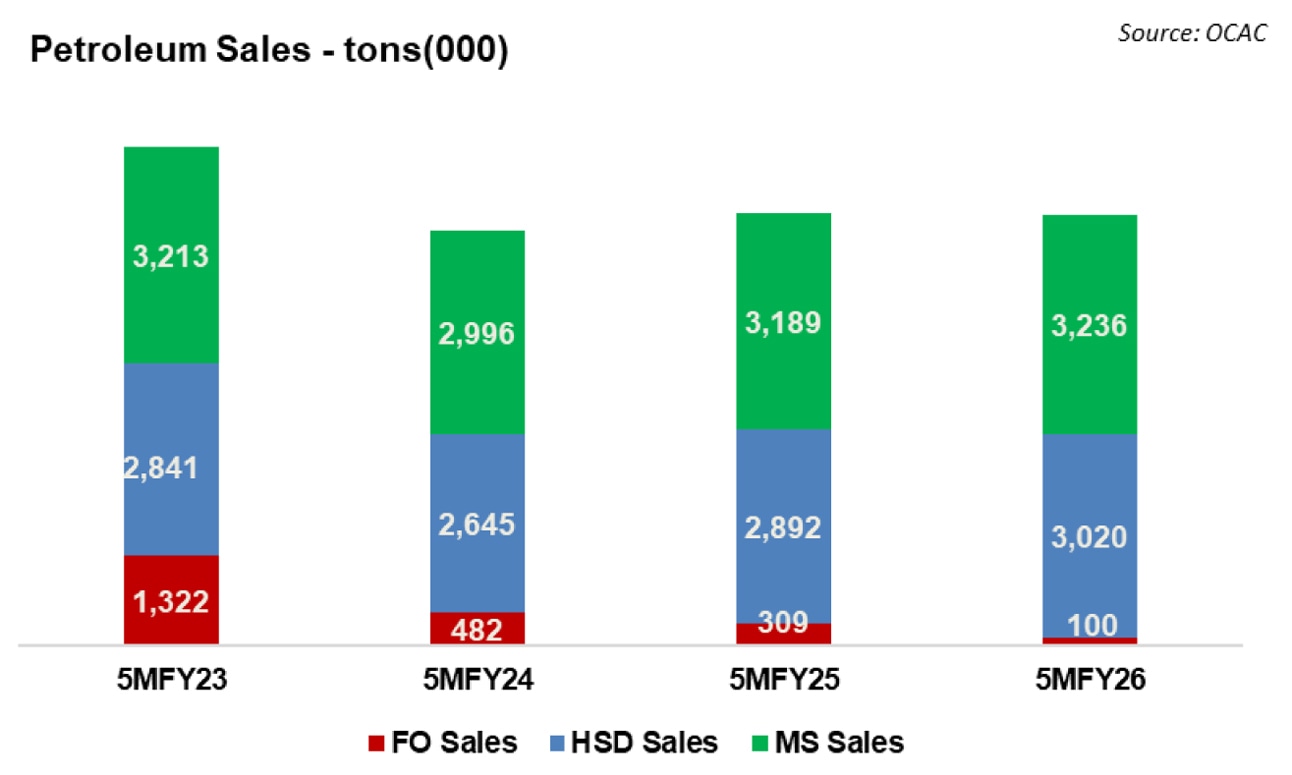

Despite the monthly decline, cumulative OMC sales for the first five months of FY26 (5MFY26) remained marginally positive, rising one percent year-on-year to 6.81 million tons.

Growth was supported by transport fuels: MS sales increased 2 percent year-on--year, while HSD volumes rose 4 percent year-on-year. Ex-FO sales improved 4 percent as well, reflecting the relative stability of retail consumption despite economic strain. FO volumes, however, plummeted 67 percent year-on-year in 5MFY26, driven by the same structural decline in FO-based power generation and the PDL impact.

Taken together, November’s contraction and 5MFY26’s modest growth tells a story of a sector under mixed pressures.

OMC sales are expected to remain weak in the near term, as all reports highlight persistent pressure from high-base effects, price sensitivity, and slowing demand.

Furnace Oil volumes will stay at historic lows; High Speed Diesel demand is likely to remain soft, given ongoing freight disruptions from western border closures, weaker farm economics, and elevated diesel prices; and Motor Spirit will continue to provide the only steady support, with modest growth expected as long as retail prices remain stable.

Comments

Comments are closed for this article.