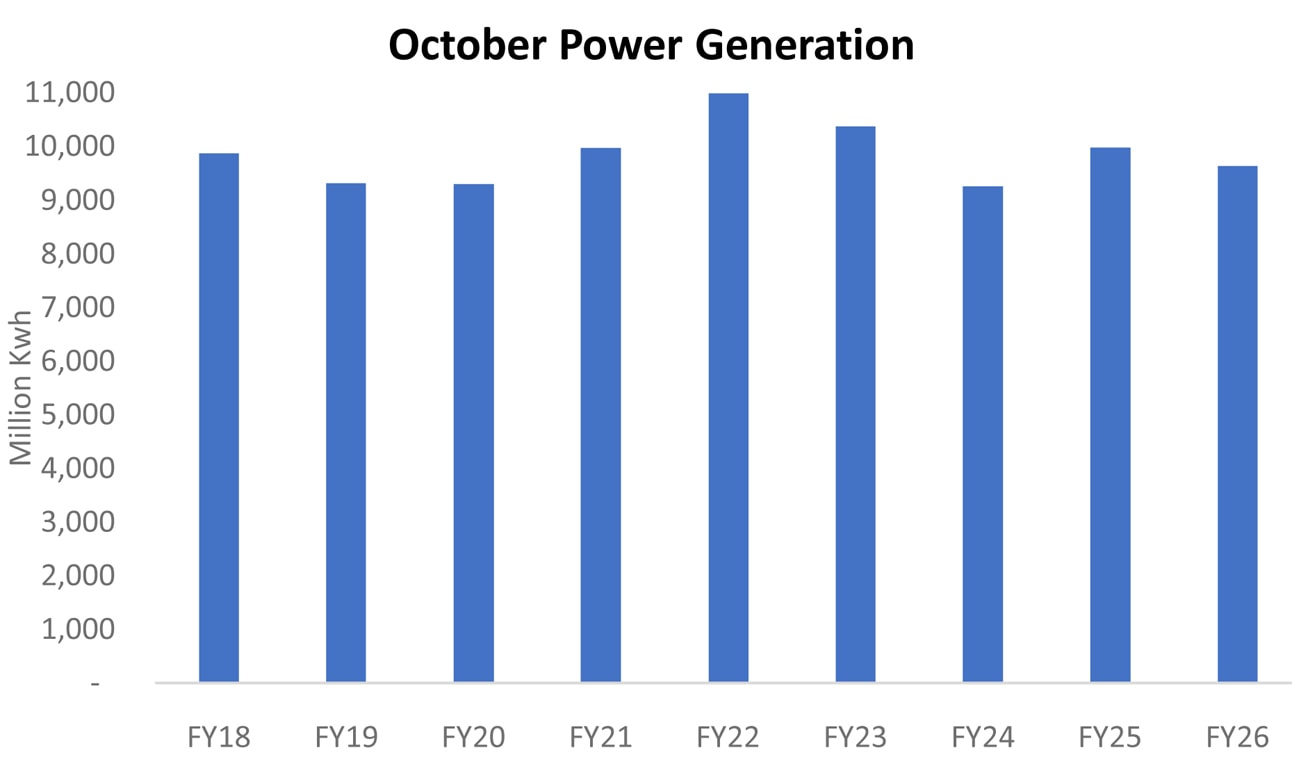

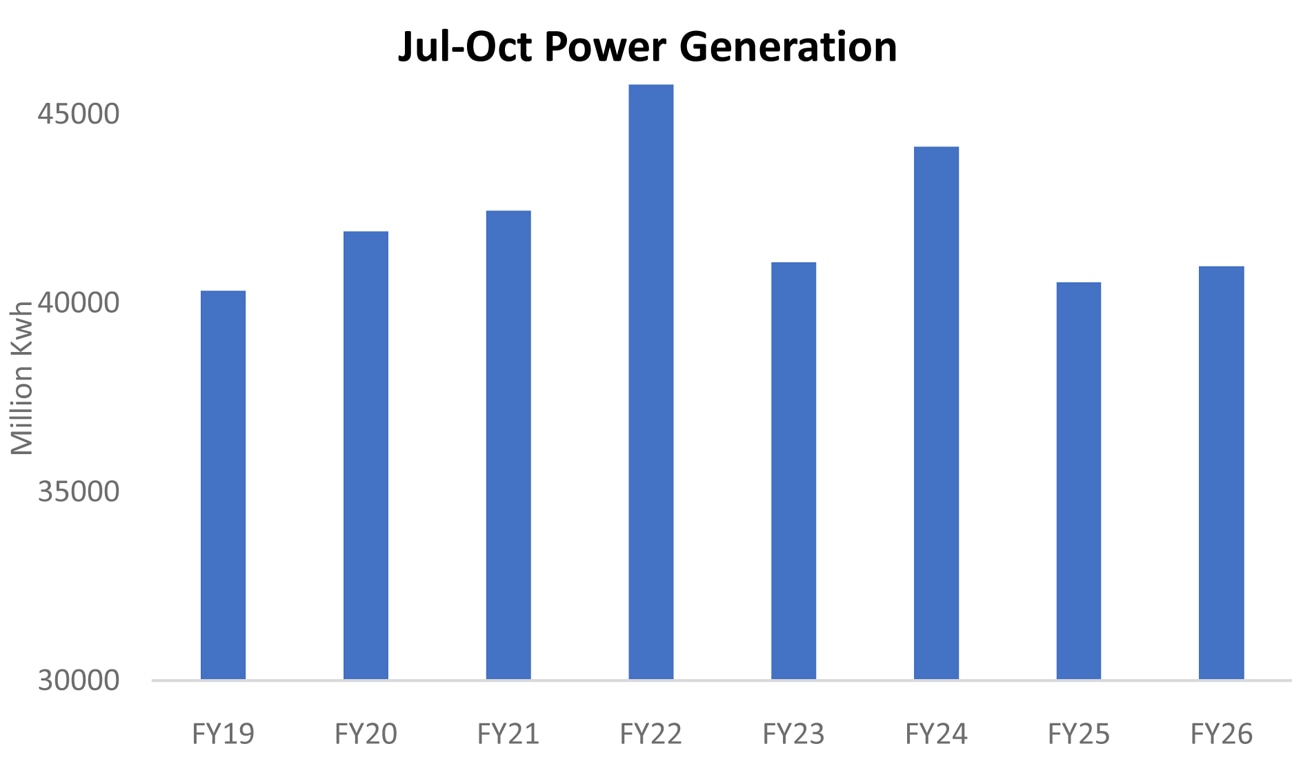

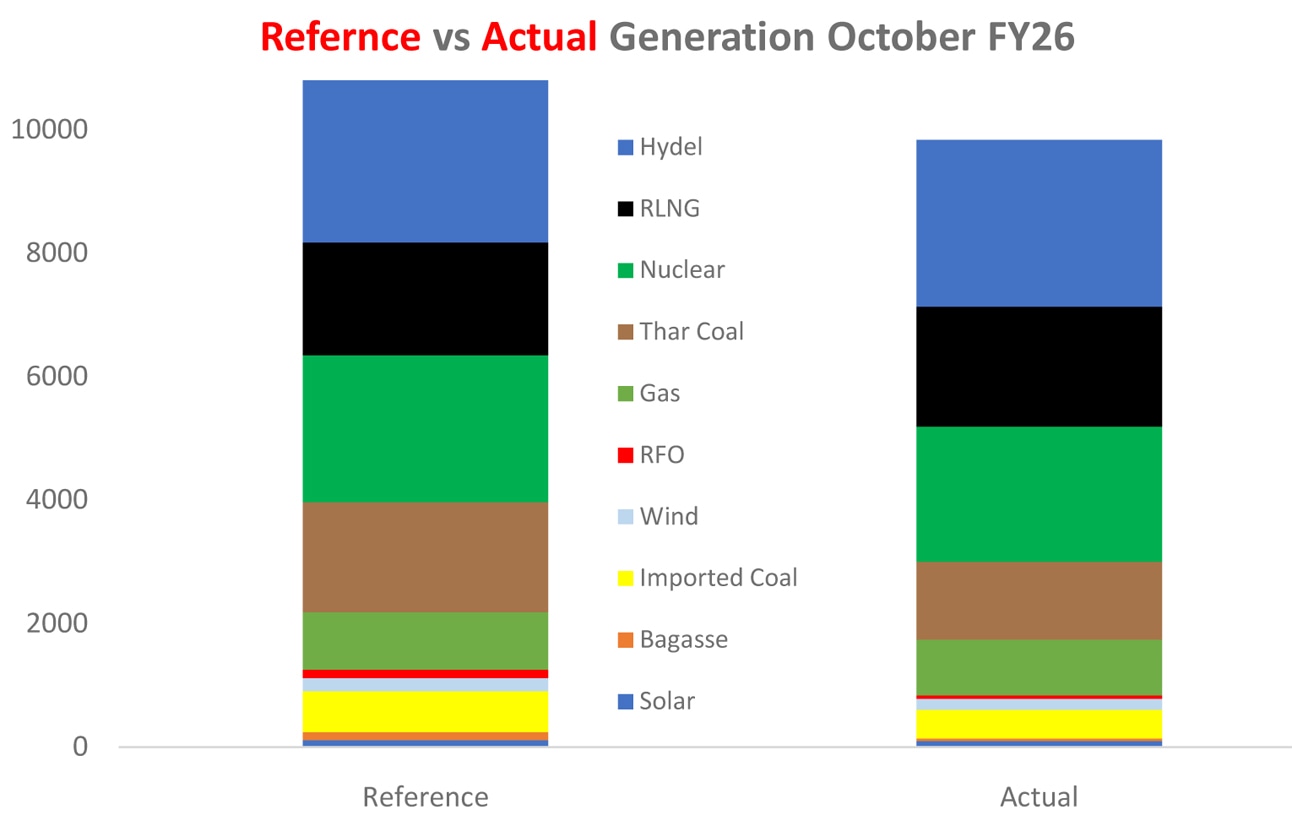

Pakistan’s national grid generated more electricity units in the October of eight years ago than it did in 2025. First four months of FY20 had a higher cumulative generation than 4MFY26 as the cumulative generation in FY26 till date is the lowest since 4MFY20. For the 13th time in 15 months – actual generation is lower than reference.

The 12-month rolling average power generation stood at 10.2 billion units – a level first achieved almost five years ago. The 4MFY26 generation is 11 percent shy of the FY22 peak. The only silver lining is the lower adjustment on account of fuel charges sought for October – continuing with the trend from last year.

Electricity demand rarely contracts for this long in any economy that is even modestly expanding, and Pakistan is no exception. There was a period when usage fell for understandable reasons: the macroeconomic crisis hit incomes, industrial output slumped, and successive tariff hikes eroded affordability. Those factors have since softened, yet grid demand has not climbed back the way planners had expected.

The explanation lies less in macro conditions and more in a structural shift that has unfolded outside the formal planning ecosystem. A rapid, largely self-financed shift toward solar has quietly reconfigured the country’s demand profile. What makes Pakistan unusual is that the momentum has come from households, small enterprises, and farmers - not from policy-led utility-scale additions. It is a bottom-up transformation that has altered consumption patterns far faster than the system operator can track.

This is now clearly reflected in operational data. The hourly load curve shows a deepening midday trough as solar generation at customer premises displaces demand from the grid. The profile bears little resemblance to the flatter daytime pattern of just a few years earlier. In rural and peri-urban regions in particular, irrigation loads and household consumption are increasingly being served by rooftop and small-scale solar during daylight hours.

This shift has taken hold even as many industries have reverted to grid supply and captive generation has declined. The fact that overall system generation still trails past reference levels suggests the pullback from domestic, agricultural, and small commercial consumers is easily overpowering the incremental return of industrial load.

The divergence between reference and actual output in RLNG and imported coal plants highlights the operational strain. With daytime demand suppressed, the system must lift generation sharply after sunset to meet evening peaks. That creates stress on thermal units, which were not designed for rapid ramping, and raises operating costs at the margin.

A grid that was built for stable, centrally dispatched demand is now dealing with a two-hump load curve shaped by millions of prosumers whose generation remains largely unmeasured. Other countries face similar transitions, but Pakistan’s version is unusually swift and informal, proceeding without the supporting reforms - pricing, metering visibility, distributed planning, or storage - that typically accompany such a shift.

For years, sector performance was evaluated through the lens of installed capacity. That metric no longer captures the system’s realities. Planning now requires accounting for distributed generation, flexible resources, and storage options. Without adapting these frameworks, the grid risks becoming progressively less aligned with consumer behavior.

The question ahead is not only about how much power the system can generate, but about the composition of demand that will remain connected to it. The direction of change is clear: grid supply is anchored in an older model, while consumer choices are evolving far more quickly.

Comments

Comments are closed for this article.