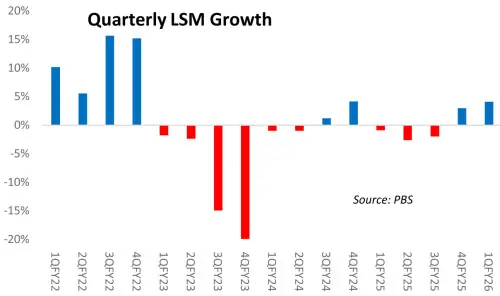

The Large-Scale Manufacturing (LSM) seems to be finally waking up from the slumber. Data for September 2025 shows 1QFY26 LSM up 4 percent year-on-year. This is only the second instance of two consecutive periods of quarterly LSM growth in the last 13. Of course, the base remains in lay, but early signs of resurgence in a select few sectors may have started to emerge.

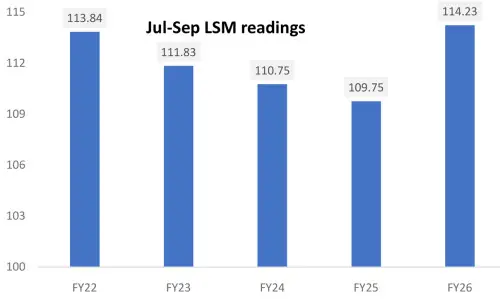

The monthly year-on-year positive readings have now stretched to six straight months – after five straight months of negative growth. The cumulative index reading for 1QFY26 is highest ever – surpassing the FY22 highs, albeit slightly.But it only gets harder from here, as a mere 4 percent year-on-year growth will not keep the cumulative index clear of FY22 highs. It will take an average 13.75 percent year-on-year growth for the next three quarters to just meet FY22 level. It will have to be the longest stretch of LSM growth, and that will takesome doing.

For now, let’s appreciate the recovery, the signs of which were seen in the sentiment surveys leading up to this point – from Purchasing Managers Index to capacity utilization levels. Nearly 45 percent of the cumulative growth is attributed to just one sector – automobiles. Growth has come from virtually all segmentsfrom jeeps and cars to two-wheelers and three-wheelers and from LCVs to trucks and buses. October PAMA numbers show the trend continues – and more of the same is in store for 4MFY26 – where LSM is likely to lead the growth mantle.

Cement remains the other turnaround story. Utilization levels have picked up meaningfully in recent months, and October’s performance is believed to have carried forward the momentum of the first quarter. Food sector growth is led by wheat and rice milling, nearing double-digit growth, hitting a 43-month high. Palm oil production also remains strong as import momentum carries on. All eyes from November onwards will turn to sugar, which has the second highest food basket weight. Early reports suggest a sizeable recovery is in the offing – likely to keep food sector growth in the positive territory for much of FY26.

Having almost single-handedly carried the positive side of LSM for well over a year – wearing apparel has now taken a back seat as readymade garment export quantity growth has muted. With October 2025 exports up 7 percent year-on-year, cumulative impact on 4MFY26 LSM will be higher than 1QFY26.

Meanwhile, the heavyweight textile sectordoesn’t have much going on and remains deep in the red, with its index staying below 100 for a staggering 36 consecutive months. The sector’s output is now lower than what it was a decade ago — a statistic that says more about Pakistan’s industrial erosion than any year-on-year growth percentage can.

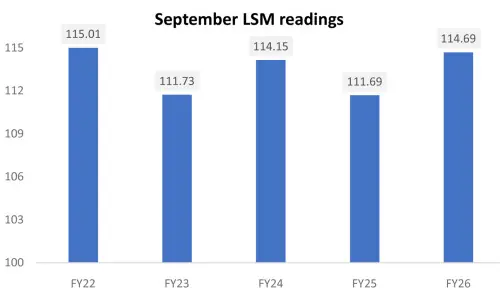

And textile isn’t alone. A staggering 10 of the 22 LSM sectors are operating at output levels lower than those recorded ten years ago.September recovery appears broad-based with 16 of the 22 LSM sub-sectorsposting growth — up from 10 in August.

Pharma sector, worryingly slipped into negative territory, with the lowest every monthly production of injections reported in September 2025. Whether it is a temporary blip or a trend remains to be seen. On the brighter side, of the six sectors still in the red zone, only two, with small weight are in double-digits.

What is clear is the worst is well in the past, and the painfully long slow recovery may finally be starting to show in numbers. That said, it is still a long way to go to erase so much ground lost in the last three years.

Comments

Comments are closed for this article.