In what appears to be a first, the Central Power Purchasing Agency (CPPA) has laid the groundwork for the base tariff adjustment for CY26, submitting its Power Purchase Price (PPP) projections after consultations with multiple stakeholders, including the Power Division.

Historically, tariff rebasing has followed the fiscal year, but there has been a growing push to shift it to the start of the calendar year. The rationale: spreading the impact of any upward revision more evenly, especially since the first quarter coincides with peak electricity consumption.

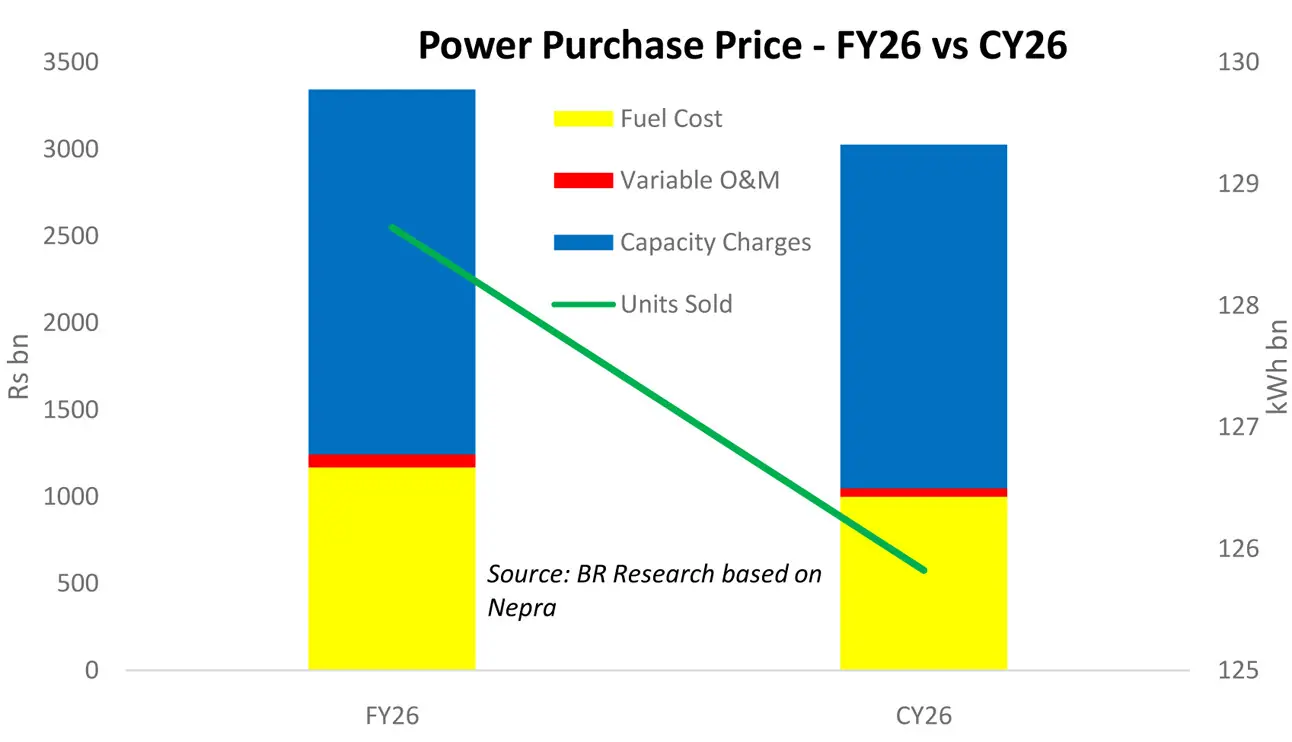

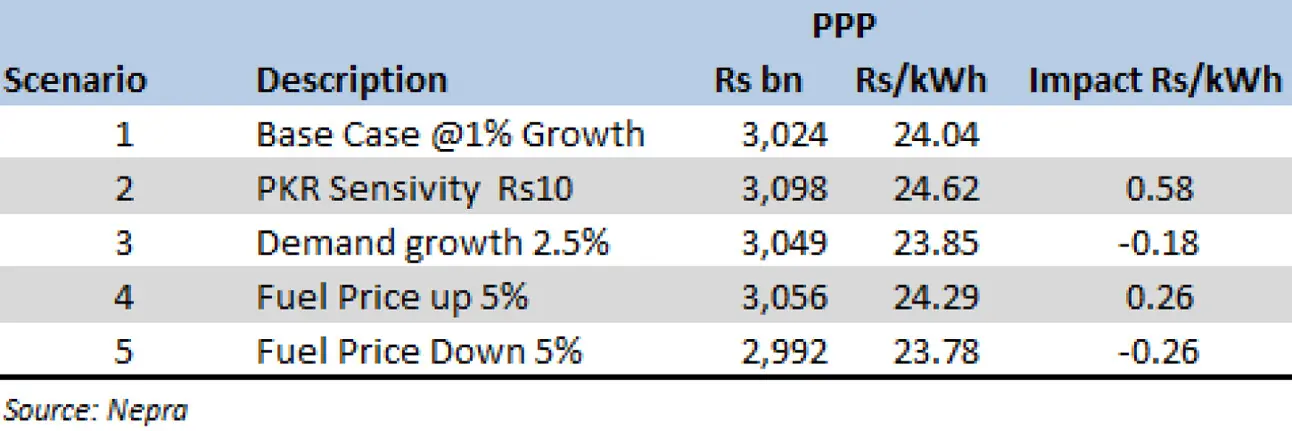

The CPPA’s projections cover five distinct scenarios, each reflecting different assumptions for demand, fuel prices, rupee-dollar parity, and hydrology. The range between the most optimistic and pessimistic PPP outcomes is less than Re1/unit - a sharp narrowing compared with the Rs1.95/unit variance in the previous rebasing exercise.

The lowest projected PPP for CY26 stands at Rs23.78/unit, nearly Rs1 below the minimum figure projected in last year’s FY26 exercise. For context, the PPP for FY25 had been set at Rs27/unit (Rs3.5 trillion in absolute terms), while FY26 was pegged at Rs25.4/unit (Rs3.26 trillion).

Early indications suggest the final CY26 PPP could decline year-on-year, marking the first such contraction in many years. Under the base case scenario, assuming modest demand growth of just 1 percent over actual generation from January–September 2025, the reduction translates into a relief of almost Rs1/unit — modest in absolute terms, but symbolically significant given that Pakistan’s electricity PPP has doubled over the past five years despite improvements in the fuel mix.

A key contributor to the potential easing is the Rs125 billion in projected savings from renegotiated IPP contracts. The demand bar has been set conservatively, reflecting the sluggish recovery over the past two years. Even the “high” demand scenario envisages only a 2.5 percent increase in power sales over January–September 2025, while the “normal” scenario projects growth of around 1 percent, consistent with both domestic and industrial realities amid the ongoing solar expansion.

What remains concerning is the anticipated sharp decline in overall electricity demand, likely to hit a five-year low in CY26. The final tariff determination will be needed to account for subsidies and prior year adjustments, alongside distribution margins. Service charges have been assumed at Rs1.91/unit across all scenarios.

While the exchange rate and international fuel prices have remained relatively stable, hydrology emerges as the key uncertainty. A weaker hydel generation season could push the PPP close to Rs26/unit, potentially offsetting gains from IPP renegotiations. How authorities adjust hydel assumptions, especially in the context of recent geopolitical developments, will be crucial. Even without disruptions to the Indus Water Treaty, experts have flagged low hydrology as a looming risk. In practical terms, this may result in more frequent periodic and monthly adjustments, even if the base tariff itself remains largely unchanged.

Comments

Comments are closed for this article.