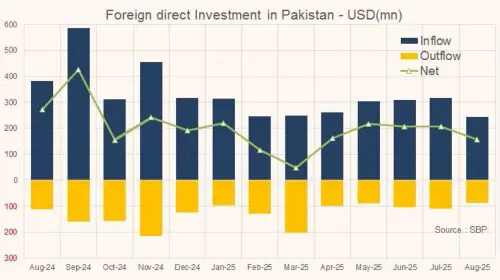

There are promises and claims about investments; however, to date, FDI has almost completely dried out. In FY25, net FDI stood at $2.5 billion, and barring retained earnings, fresh investment was below $500 million.

The first two months of FY26 show no different picture. Net FDI stood at $363 million – down 22 percent year-on-year. The news flow is good. The feel-good factor is here. Markets are bullish. However, the numbers are dried up. Hopefully, some day this euphoria may turn into actual investment.

The numbers so far are concentrated in the power sector – comprising 43 percent of total FDI. The share was similar last year. A comparable chunk of FDI is coming from China. This is the lingering effect of CPEC, where major investments were undertaken in the power sector. Now those companies – mainly IPPs – are earning profits on guaranteed returns, irrespective of how much power is being generated. These profits are being retained here, partly due to delayed payments and limited dividend repatriation.

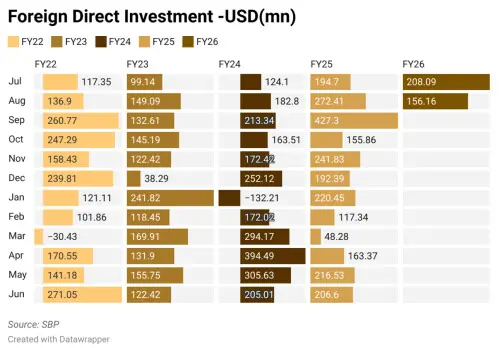

Over the last ten years, FDI has hovered between $2–3 billion annually, with an average of 35 percent in the power sector. FDI from China averaged 36 percent, mostly in energy. The country is stuck in a groove. No meaningful foreign investment has come apart from power projects sponsored by China. It is high time the gears were shifted to attract investment from diversified sources – across both sectors and countries. For now, there is only hope to sell.

There were promises of $75–100 billion from GCC countries, but none has materialized. The recent defence pact with Saudi Arabia is a sign that investment may eventually flow in. The buzz is that other GCC countries may follow, showing inclination towards investment.

These countries may offer concessions and free money. They may provide oil and gas at lower rates. They may add to remittances, as military personnel are posted there and send money back home. However, investment requires bankable projects. It requires economic opportunities. All these demand reforms and deregulation – signs of which are nowhere to be seen.

Another hope lies with the US in the mining sector. Saudi Arabia has pulled out of RekoDiq, where costs are escalating, and third-party investment is needed. American firms are reportedly taking interest. However, mining projects are long-gestation and require time and patience to yield profits. These firms also fear policy inconsistency if the regime changes, which makes them cautious.

In other economic areas, there is slack in many industries, and fresh investment is hard to come by. The stock market has performed superbly, but foreigners are yet to take a bet. They remain net sellers. Some hope Saudi Arabia may buy energy stocks listed on the stock exchange, whose valuations are improving with the possible settlement of circular debt.

There is potential in mining, energy, and other sectors. There are geopolitical rents to extract. The challenge is to convert this potential into actual investment flows – sooner rather than later.

Comments

Comments are closed for this article.