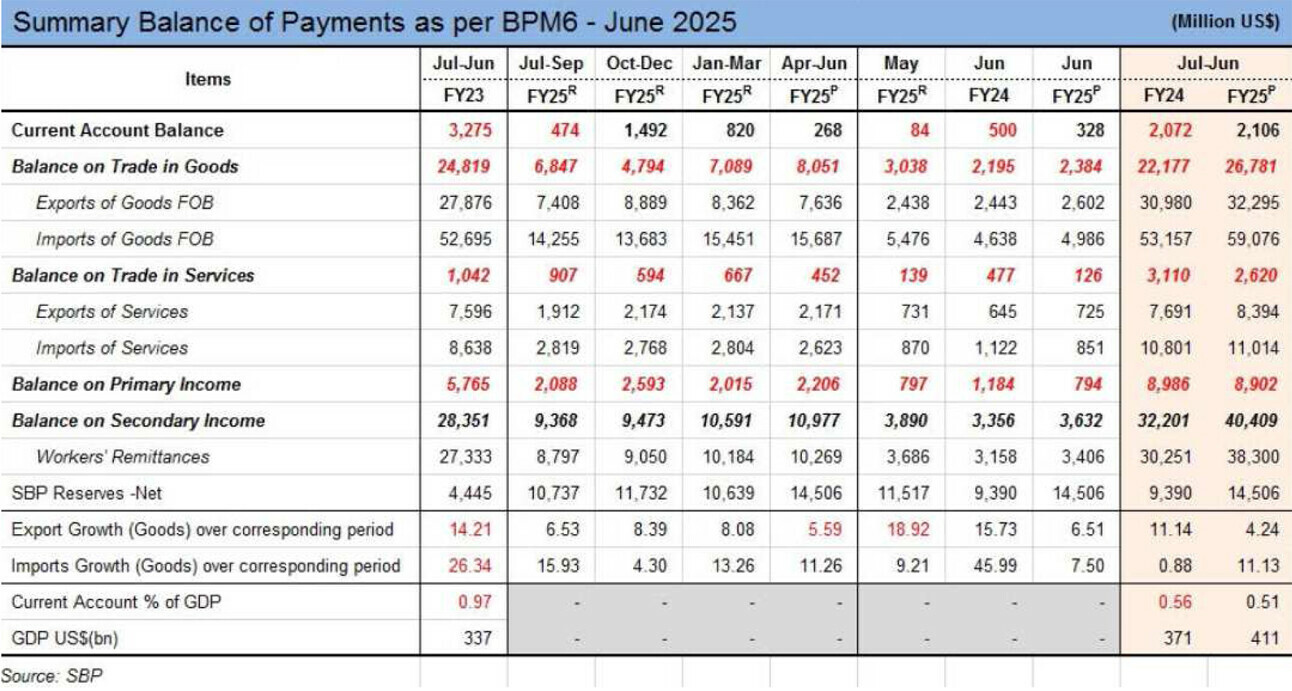

The current account posted a surplus of $2.1 billion (0.5 percent of GDP) in FY25, compared to a deficit of $2.1 billion in the previous year. This is Pakistan’s first current account surplus since FY11. Interestingly, there were four consecutive years of current account surpluses between FY01 and FY04—perhaps linked to the country’s six consecutive years of primary fiscal surpluses during FY99–04.

Now, with two straight years of primary surpluses (FY24–25), the current account has turned positive again in the second year.

In economic theory, deficits in current and fiscal accounts are referred to as twin deficits. At present, we are in a rare phase of twin surpluses. If the government maintains a budgeted primary surplus in FY26, it is likely the current account will remain in surplus as well.

The current account balance improved by $4.2 billion in FY25 compared to the previous year, even though the trade deficit in goods and services worsened by $4.1 billion. The $8.3 billion swing is almost entirely explained by the extraordinary performance of home remittances, which increased by $8.0 billion—or 27 percent—to $38.3 billion in FY25.

However, this momentum in remittances may not continue. The rise was not primarily driven by an increase in the number of workers going abroad. In fact, fewer people emigrated in 2024 compared to FY23. For example, the largest increase in inflows during FY25 came from the UAE—up by 41 percent to $5.5 billion—while the number of workers headed to the UAE fell by 71 percent year-on-year to just 66,000 in 2024.

This suggests there is more to the remittance surge than new labor migration. It is perhaps a form of reverse money laundering. Significant capital flight to the UAE occurred in 2022–23, as indicated by heavy Pakistani investment in Dubai real estate. Additionally, many freelancers and businesses operate partly from the UAE and remit money back to Pakistan through formal banking channels for local expenses. Crackdowns on smuggling may have also redirected informal flows into formal remittance channels.

That said, there is a ceiling to this upside, and it is likely to fade. At best, remittances may grow by 8–10 percent in FY26, leaving limited space for economic expansion without risking a return to current account deficits and pressure on SBP’s foreign exchange reserves.

Imports in FY25 (PBS data) reached $58.4 billion—an increase of 7 percent year-on-year. This is approaching FY18 levels, when GDP growth was close to 6 percent, unlike the current 2.5 percent. Importantly, due to rapid population growth and sticky food prices, the rising share of so-called essential imports is becoming problematic. Food imports in FY25 were 1.3 times higher than in FY18, and 90 percent of the FY22 peak—years when GDP growth exceeded 5 percent.

In contrast, non-essential imports (including transportation equipment, metals, agri-chemicals, etc.) are only two-thirds of their FY22 levels. If economic growth is to be revived, any increase in imports could undermine hard-earned gains. The SBP has purchased $12–14 billion from the interbank market over the past 18 months—funds that helped service external debt, reduce forward liabilities, and rebuild reserves to $14.5 billion.

Yet banks remain reluctant to process import payments and are conservative in opening letters of credit (L/Cs). Given these restrictions, how can the economy grow to meet the government’s 4.2 percent target for FY26 without allowing imports to rise? Thus, the business-as-usual approach continues: SBP will keep policing commercial banks, controlling import flows, and buying dollars from the interbank market to build buffers.

The only viable way to accommodate higher imports is through higher export proceeds. But exports (goods, per PBS data) already hit an all-time high of $32 billion in FY25. Exporters are dissatisfied with the current tax and energy policy environment and are struggling to grow from this base. There is little to no chance of substantial growth in exports in FY26.

ICT exports are the standout performer—up 18 percent to $3.8 billion, with a compound annual growth rate of 17 percent over the past decade. However, the scale remains small. For context, ICT exports barely match Pakistan’s edible oil import bill, which stood at $3.7 billion in FY25. In the larger scheme of things, the contribution is still limited.

To sustain external stability while pursuing growth, Pakistan must attract financial and capital account inflows to fund a manageable current account deficit. However, foreign direct investment (FDI) remained disappointing—at $2.4 billion, up just 13 percent. Counterintuitively, portfolio investment remained negative despite record performance in the stock market. Foreign investors, it seems, are still not convinced.

They need to be—because growth in 2004–07 was not just fueled by prior twin surpluses, but also by robust FDI during the recovery years. Pakistan needs inflows.

To supplement investment, debt-related flows must also rise. After remaining negative for 11MFY25, the financial account turned positive in June with a $2.8 billion inflow. This helped the SBP surpass its reserve target and brought a sigh of relief—but it is not enough to trigger meaningful growth or job creation.

Comments

Comments are closed for this article.