September electricity generation: The grid won’t catch the sun

Power generation data for September 2025 paints a familiar picture — one of stagnation and structural transformation colliding in real time.

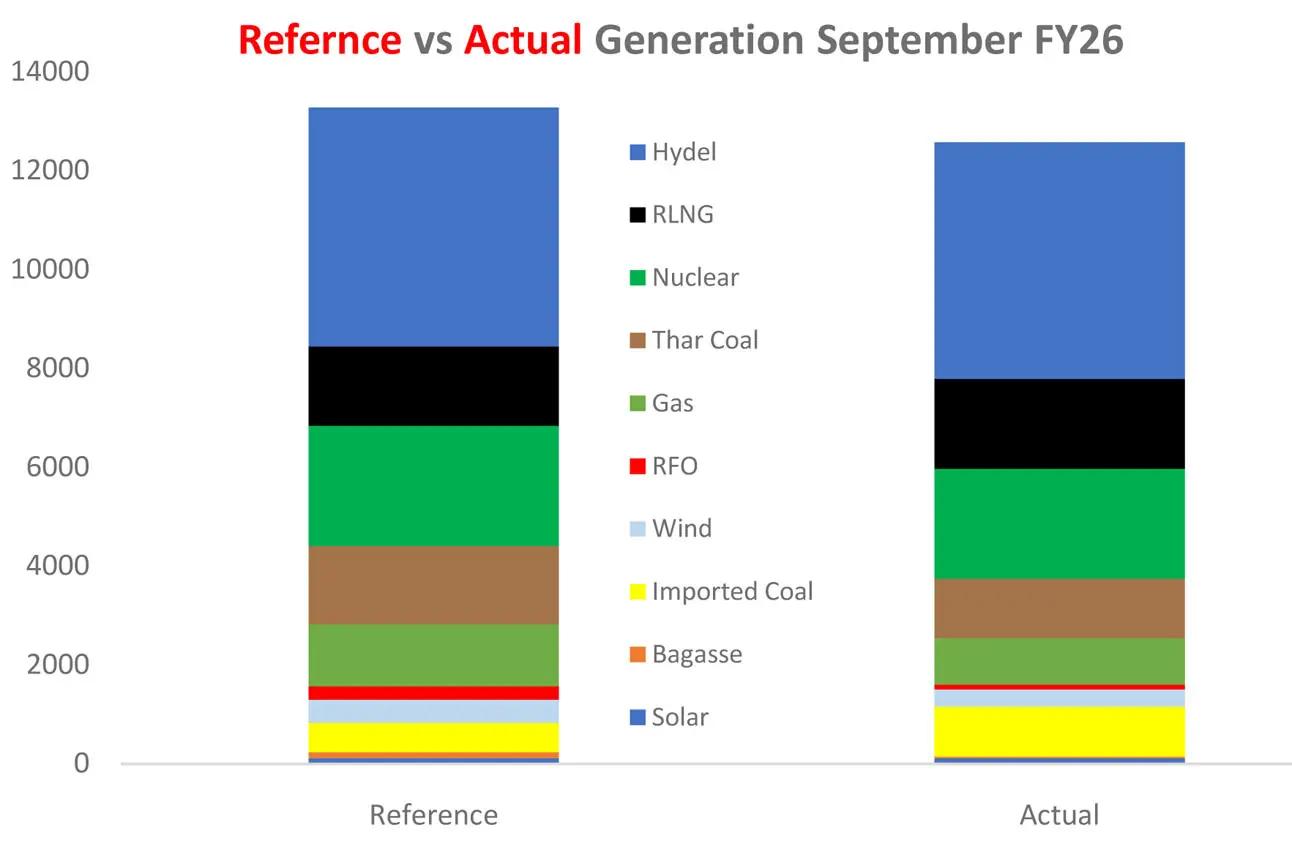

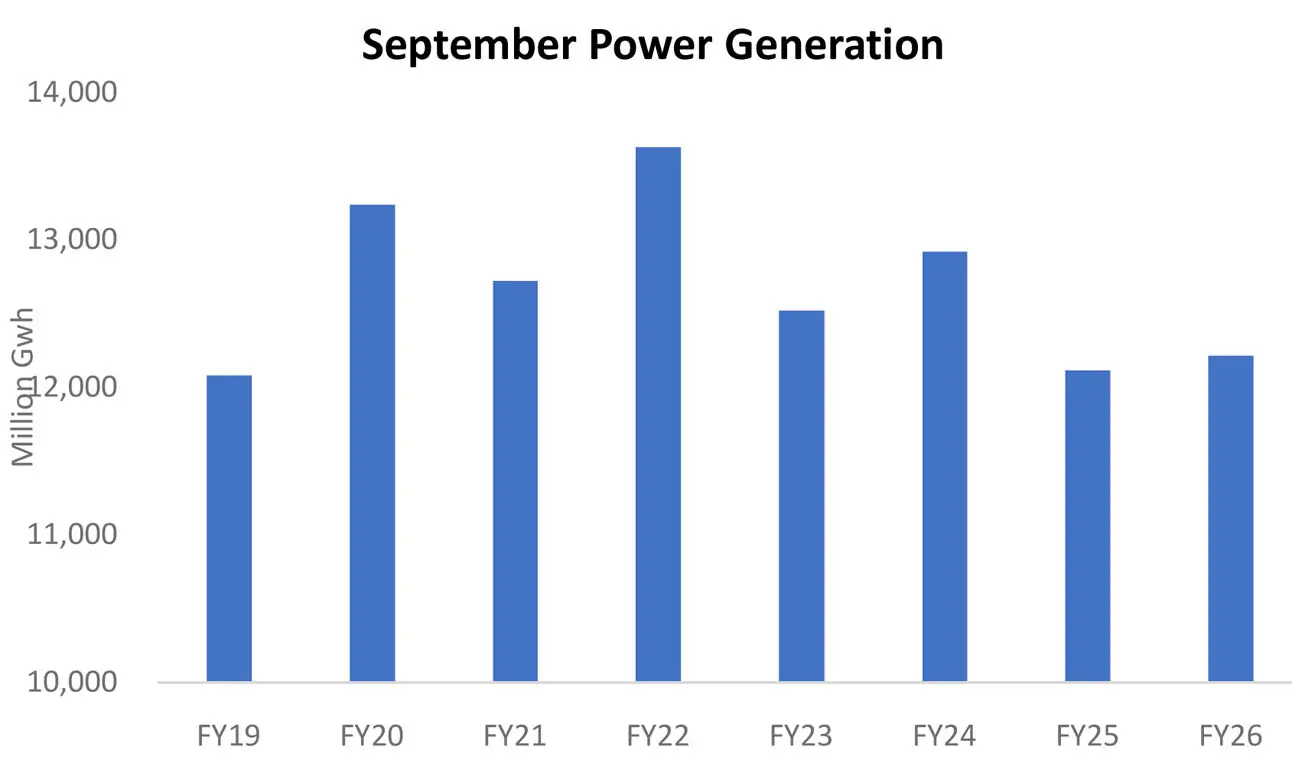

Gross generation clocked in at 12.6 billion units, about 5 percent lower than the reference generation, marking the 12th instance in the last 14 months that actual generation has fallen short of target.

On the surface, generation is up a marginal 1 percent year-on-year, but that rise comes on a low base, as power output had tumbled to multiyear lows last year.

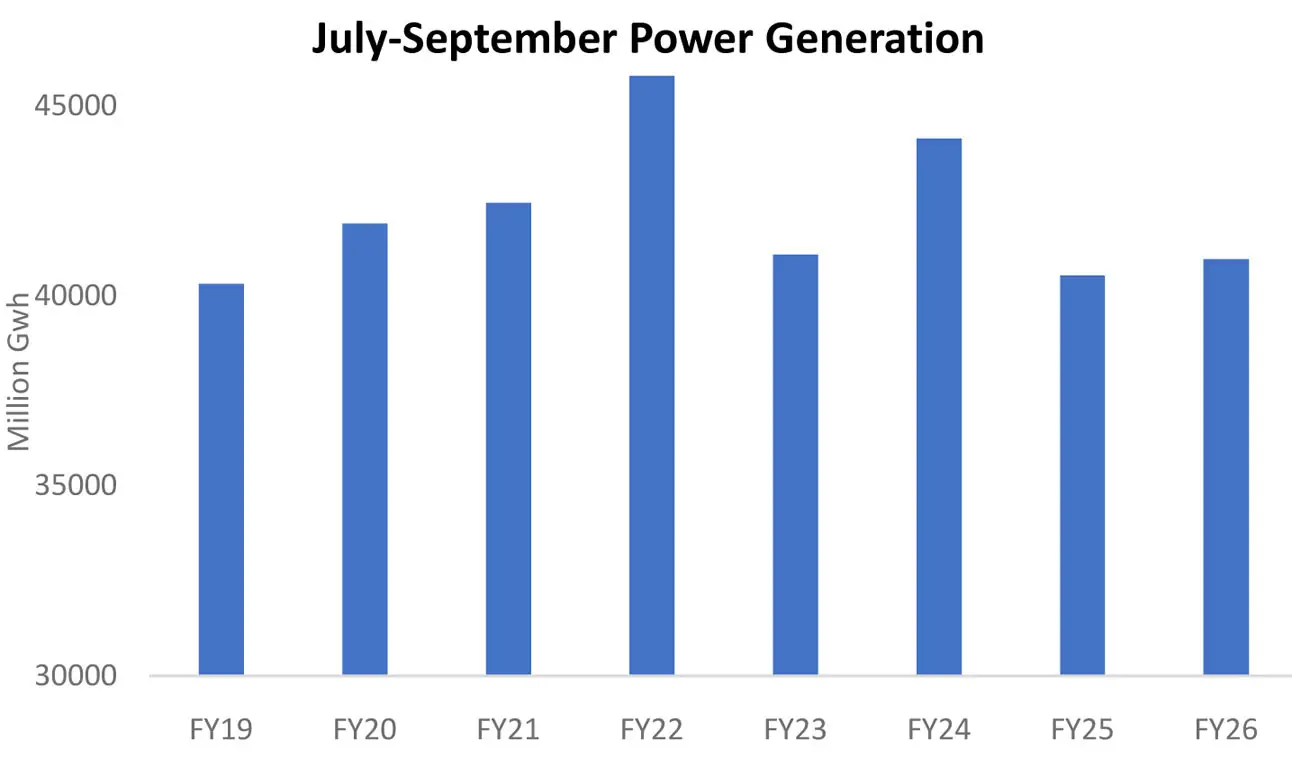

The broader picture offers little comfort: the first quarter of FY26 saw gross generation of 40.9 billion units, still below levels recorded in 1QFY20. That’s half a decade of economic, demographic, and technological change — and yet generation remains stuck in the same zone.

Electricity demand doesn’t typically contract over such a long horizon in any growing economy. Pakistan’s case is no different. There was, of course, a period when organic demand shrank, as the country reeled from a near-default macroeconomic crisis, industrial activity slowed, and power tariffs soared.

But those temporary suppressors have long since eased, and yet grid-based demand has not recovered in the way it once did.

The real story lies elsewhere — in the solar rush that has quietly redrawn the contours of Pakistan’s electricity landscape. And unlike most transitions that begin with policy nudges or utility-scale reforms, this one has been led from the bottom up — by households, farmers, and small businesses rather than by the state.

Pakistan’s solar imports have ballooned over the last three years, with solar panel imports crossing $2 billion in 2024 alone, quadrupling in just three years. Battery imports have followed the same trajectory, with the first half of 2025 already exceeding the entire previous year’s total.

Together, they tell a story of mass adoption — an unplanned but unstoppable migration away from grid dependence during daylight hours.

The impact of this transition is now visible in the data. Electricity hourly generation profiles show a pronounced midday dip in grid demand — the so-called “duck curve” — that looks nothing like the flat consumption pattern of just two or three years ago. Daytime demand, especially in rural and agricultural zones, has collapsed as on-site solar meets irrigation, residential, and commercial needs.

This solar-driven reshaping of demand has come even as captive power generation has been curtailed, and a large segment of industrial users has returned to the grid. In other words, even after factoring in higher grid uptake from industries, total system generation continues to lag — suggesting that the migration of domestic, small commercial, and agricultural users away from the grid is more than offsetting any industrial rebound.

The deviation between actual and reference generation in the two key imported fuel categories — RLNG and imported coal — underscores the new operational challenge. With daytime grid demand dropping sharply, the system must rapidly ramp up generation post-sunset, leading to load-following inefficiencies, higher marginal costs, and greater wear on thermal plants that were not designed for such volatility.

The grid, designed around predictable consumption cycles and centralized dispatch, is now contending with a volatile, two-peak load curve, driven by millions of prosumers whose generation is invisible to the system operator. This structural change is not unique to Pakistan, but the speed and informality of its adoption here — largely without coordinated planning or pricing reform — makes it particularly disruptive.

For policymakers and regulators, this presents a double bind. On one hand, the proliferation of rooftop solar has provided genuine relief to households and small enterprises that have faced punishing electricity tariffs.

On the other hand, it has eroded the demand base needed to sustain the financial viability of the grid, especially given the large, fixed costs embedded in Pakistan’s generation and transmission contracts.

The FCA (Fuel Cost Adjustment) mechanism will once again expose the widening gap between reference and actual generation in the coming months, particularly for imported fuels. But the larger issue goes beyond tariff adjustments — it’s about a system architecture stuck in the past, while the user base has already jumped a decade ahead.

Pakistan’s power planners have long measured progress by megawatts added to the grid. The new reality demands a different metric — one that accounts for distributed generation, storage integration, and flexible dispatch. Without that shift, the system will continue to look increasingly outdated, even as consumers modernize around it.

The real debate Pakistan needs is about who stays on the grid — and for how long. Because the trend lines are already clear: generation may be stuck in the past, but consumption behaviour has decisively moved into the future.

Comments

Comments are closed for this article.