EDITORIAL: The latest Pakistan Economic Survey 2025-26 presents a disturbing picture of the country’s public health landscape. While the government points to modest improvements in some indicators, a comparison with South Asian averages shows that Pakistan continues to lag behind its regional peers on several critical measures.

More worrying is that these gaps persist despite repeated warnings from health experts and development practitioners about the consequences of chronic under-investment in the health sector.

The survey’s statistics are sobering. Pakistan’s life expectancy at birth stands at 67.8 years, nearly five years below the South Asian average of 72.6 years.

Maternal mortality remains alarmingly high at 155 deaths per 100,000 births, compared to 120 in the region, while the infant mortality rate is more than double the regional average, pointing to serious deficiencies in maternal and child healthcare services.

Equally troubling are the levels of undernutrition and stunting, which continue to affect millions of children and undermine their physical and cognitive development. These challenges are compounded by the country’s comparatively high birth rate.

Rapid population growth places immense pressure on already overstretched health, education and social welfare systems. Without effective family planning services and greater investment in reproductive health, Pakistan risks falling even further behind its neighbours in human development outcomes.

The government’s economic managers frequently cite fiscal constraints to justify limited social-sector spending. Yet the real issue is one of priorities.

Countries that have made significant gains in health outcomes have done so by treating healthcare as an investment rather than expenditure. As a matter of fact, better health produces a more productive workforce, reduces poverty and lowers long-term pressures on public finances.

Pakistan’s health indicators are not merely statistics; they reflect the lived realities of millions of citizens. Unless health — alongside education — is placed at the centre of national development planning and supported by substantially greater public investment, the country will continue to pay a heavy economic and social price for this neglect.

ISLAMABAD: The opposition Pakistan Tehreek-e-Insaf (PTI) on Thursday rejected the government’s recently released Pakistan Economic Survey 2025-26, calling it a politically motivated document that misrepresents the country’s economic situation.

In a statement, PTI spokesman Sheikh Waqas Akram described the survey as “a masterpiece of statistical manipulation” and accused the coalition government of ignoring the economic hardships faced by ordinary Pakistanis.

“This document is not an Economic Survey. It is an anti-poor manifesto wrapped in fancy tables and self-congratulatory claims,” he said.

The survey reports a gross domestic product (GDP) growth of 3.7 percent for the year, a figure Akram said falls short of the 6.5 percent growth achieved during the PTI government under former prime minister Imran Khan.

He also questioned the reported increase in per capita income from USD1,700 to USD1,901, calling the methodology “opaque” and the data “economic gas lighting.”

Akram criticised the government’s agriculture growth figures, which the survey cites at 2.89 percent, arguing that they are heavily dependent on livestock estimates that may be “unverifiable.”

He also dismissed claims of 6.1% growth in large-scale manufacturing, citing factory closures, industrial shutdowns, and a decline in investor confidence.

He also accused the government of taking credit for programs introduced under the PTI, including the Roshan Digital Account and Naya Pakistan Certificates.

Debt management was another point of criticism. Akram highlighted that although the government reports 45 percent of debt as concessional, debt servicing has reached nearly Rs8,000 billion, with projections for the next fiscal year close to Rs7,824 billion. He said much of the borrowing is domestic and burdens ordinary households.

He also disputed the survey’s inflation narrative. While the report states that consumer price index (CPI) inflation remained broadly stable at 6.2-6.7 percent from July to April FY26, he noted that May 2026 saw inflation surge to 11.7 percent year-on-year, the highest since June 2024, largely due to rising food, energy, and transport costs.

“This Economic Survey is a declaration of war on the poor,” he said. “While elites celebrate manipulated Debt-to-GDP ratios and reported growth, ordinary Pakistanis face rising prices, unemployment, and shrinking livelihoods.”

PTI called for transparent and verifiable economic data using consistent baselines, including figures from the PTI era, and rejected the survey as a document designed to mislead both the public and international stakeholders.

ISLAMABAD: Pakistan remained on the frontline of the global climate crisis in FY2026 as the 2025 floods alone caused damages worth Rs 822 billion, claimed more than 1,039 lives and displaced over four million people, according to the Pakistan Economic Survey 2025-26.

The document noted that 2025 ranked as Pakistan’s second warmest year in the past 65 years, with a national mean temperature of 23.9°C and rainfall three percent below average. Progress under the IMF Resilience and Sustainability Facility was highlighted in the survey, including completion of four key reforms: introduction of carbon levy, adaptation of an electric vehicle policy framework, issuance of climate-related financial risk management guidelines, and operationalisation of green taxonomy and ESG disclosure guidelines.

Climate change has moved from a distant threat to a present reality for Pakistan, creating serious risks for the country’s economy, agriculture, infrastructure and population. It noted that despite contributing less than one percent to global emissions and only 0.4 percent of historic emissions, Pakistan continues to face a disproportionately high burden of climate-related disasters.

According to the survey, shifting monsoon dynamics intensified extreme precipitation, while excessive heat and rainfall triggered multiple floods across the country. Pakistan has faced repeated climate shocks in recent years, including the catastrophic 2022 floods and the widespread 2025 floods that hit all four provinces and Azad Jammu and Kashmir.

The climate change is now a major downside risk to Pakistan’s economic growth, as extreme weather events damage crops, homes, roads, public infrastructure, livelihoods and basic services. The agriculture sector, rural communities, flood-prone districts and low-income households remain among the most vulnerable to climate shocks.

Pakistan has launched the Pakistan Climate Prosperity Plan as a flagship investment-led framework to transform climate challenges into opportunities for sustainable economic growth, resilience and prosperity. The plan is aimed at mobilising climate investment and linking adaptation needs with economic development.

The survey said the Pakistan Climate Prosperity Plan also presents a major climate investment requirement, estimating that the country will need around USD 1.6 trillion by 2050, with annual investment needs of about USD 65 billion. It projected climate-related investments of USD 565.7 billion by 2035, covering priority areas such as energy transition, climate-resilient agriculture, green economic zones, infrastructure, transport and natural capital.

The survey highlighted Pakistan Green Taxonomy, which has been issued and is being implemented. Under this framework, voluntary reporting of climate-related risks, opportunities and taxonomy-aligned activity data will continue until June 2029 before a three-phase mandatory rollout. The taxonomy is expected to help identify green investments, improve climate finance flows and support sustainable business activity.

ISLAMABAD: Pakistan’s agriculture sector has missed the growth target of 4.5 percent set for the outgoing financial year and grew by 2.89 percent, according to the Economic Survey 2025-26 released on Thursday.

The Survey noted that the agriculture sector recorded a growth of 2.89 percent, compared to 1.53 percent during the same period last year. Cotton and maize production contracted by 0.5 percent and 2.7 percent, respectively, it said.

It further stated that sugarcane registered growth of 6.2 percent (rising from 84.24 to 89.45 million tons), followed by wheat at 4.3 percent (increasing from 28.40 to 29.61 million tons), and rice at 2.8 percent (up from 9.72 to 9.99 million tons).

During 2025-26 the livestock sub-sector, a major component of agriculture and an important contributor to the overall economy, expanded by 3.75 percent, against 2.95 percent in 2024-25. This performance was supported by a 3.46 percent increase in output, notwithstanding a 4.5 percent decline in green fodder availability.

According to the Economic Survey, during 2025-26, cotton was sown on 2.01 million hectares, a 1.5 percent decline in area compared to 2.04 million hectares last year, the production of cotton declined by 0.5 percent to 7.05 million bales from 7.08 million bales last year.

Decrease in production was mainly associated with a reduction in area sown, as farmers continued to adjust cropping choices in response to relative returns and competing Kharif crop options.

Wheat was cultivated over an area of 9.48 million hectares, compared to 9.07 million hectares last year, reflecting an increase of 4.4 percent, wheat production increased by 4.3 percent to 29.61 million tons, compared with 28.40 million tons last year, supported by an expansion in area sown. The favourable input conditions at the time of sowing provided important support to crop performance.

During 2025-26, despite 3.6 percent decline in area as compared to last year, the production of rice increased by 2.8 percent to 9.99 million tons from 9.72 million tons. The increase was driven by a 6.6 percent improvement in yield, which reached 2,660 kg/hectares.

The Survey noted that the area under sugarcane cultivation expanded by 2.4 percent to 1.22 million hectares during 2025-26 and production increased by 6.2 percent to 89.45 million tons, driven by a 3.7 percent improvement in yield to 73,200 kg/hectares. This was mainly driven by higher expected returns compared to competing crops like cotton and maize, thereby encouraging farmers to expand sugarcane cultivation.

Maize was sown on 1.59 million hectares showing a decrease of 0.1 percent over last year whereas its production declined by 2.7 percent to 8.79 million tons from 9.04 million tons.

During 2025-26, the production of gram, potato, chillies, moong, and bajra increased by 50.4 percent, 27.6 percent, 23.5 percent, 15.2 percent, and 7.2 percent, respectively, mainly due to expansion in the cultivated area. On the other hand, production of onion, mash, masoor, barley, and jawar declined by 2.2 percent, 3.7 percent, 8.0 percent, 6.6 percent, and 12.3 percent, respectively.

Livestock industry has become the primary driver of agricultural growth, accounting for 62.4 percent of agriculture’s value addition and 14.6 percent of GDP in 2025-26. The sector has experienced steady growth, with its gross value addition increasing from Rs6,004 billion in financial year2025 to Rs6,229 billion in financial year 2026, reflecting a growth of 3.75 percent.

ISLAMABAD: A 29.7 percent drop in LNG import volumes has prompted prospective investors to delay decisions on constructing new terminals.

At the same time, a lack of new discoveries has caused domestic natural gas production to fall by 3.7 percent, tightening the country’s overall energy outlook, reveals Pakistan Economic Survey 2025-26.

“Oil and Gas Regulatory Authority (OGRA) has granted construction licenses to two private sector companies i.e. Energas Terminal Private Limited (ETPL) and Tabeer Energy (Private) Limited (TEPL). They have however not taken the final investment decisions (FID) so far”, noted the Economic Survey.

The oil and gas regulator has granted four provisional licenses (out of which only one is valid at the instant) for virtual pipeline projects to facilitate in completing the formalities required for the application of a construction/ installation license.

Moreover, M/s LNG Easy (Private) Limited has been granted a construction license to develop the project; the company has yet to take a Final Investment Decision (FID).

Despite a 29.7 percent reduction in volume, LNG still accounted for 15.2 percent of the country’s total imports during the first nine months of the current fiscal year (July–March). The drop in LNG imports reflects declining demand for gas-based power, a growing contribution from alternative energy sources like solar, and more efficient energy demand management.

Once these terminals are built and are operational, the government is hoping to add approximately 1.52 BCFD of re-gasification capacity, which will help mitigate the natural gas demand supply gap, according to the Survey.

The average natural gas consumption was about 2,929 Million Cubic Feet per day (MMCFD) including 613 MMCFD volume of RLNG during July to March 2026. In same period, the two gas utility companies (SNGPL and SSGCL) have laid 729 Km Mains and 403 Km Services lines and connected 95 villages/towns to the gas network. During this period, 149,908 additional RLNG based gas connections including 148,225 domestic, 1,578 commercial and 105 industrial were provided across the country.

It is expected that gas will be supplied to approximately 708,245 new consumers (during the FY 2027) Gas utility companies have planned to invest Rs 4,491 million on Transmission projects, Rs 87,457 million on Distribution Projects and Rs 10,810 million on other projects bringing the total investment of Rs 102,758 million during the FY 2027.

While, oil production in the country dropped by 0.6 percent, petroleum imports remained the largest component of import bill, accounting for 22.2 percent of total imports during July-March FY 2026. Despite their large share, petroleum imports declined by 5.9 percent to US $ 11.2 billion, helping contain overall import pressures.

During July-March FY 2026, total consumption of petroleum products stood at 13.64 million metric tonnes (MMT), registering a year-on-year increase of 3.5 percent compared to 13.17 MMT during the same period of FY 2025.

The Strait of Hormuz, through which nearly 25-30 percent of global oil trade and around 20 percent of liquefied natural gas (LNG) shipments pass, remains critically important for energy-importing economies in Asia and Europe. And given the critical importance of crude oil and petroleum products for the country, SBP allowed import of Crude Oil/ Petroleum Products on CIF (cost, insurance, freight) basis for a period of sixty (60) days - making procurement easier and avoiding delays in shipment during periods of market uncertainty.

ISLAMABAD: Pakistan’s total public debt amounted to Rs 83,285 billion by the end of March 2026, registering an increase of Rs 2,767 billion (around 3.4 percent) during the first nine months of the current fiscal year, as it was Rs 80,518 billion on June 30, 2025.

This was noted in the Economic Survey 2025-26 released on Thursday. The survey further noted that the outstanding stock of contingent liabilities was Rs 4,322 billion by the end of March 2026 against Rs 3,632 billion in the same period last year, reflecting an increase of 19 percent.

External public debt was recorded at USD 92.2 billion at the end of March 2026, showing an increase of around USD 364 million during the first nine months of the current fiscal year compared to an increase of USD 883 million during the same period of the last fiscal year.

However, it does not contain liabilities of foreign exchange, public sector enterprises (PSEs), banks, and private sector.

According to the State Bank of Pakistan (SBP) data, the country’s external debt and liabilities stood at $137.55 billion by the end of March 2026, which contained government external debt, short-term, from the International Monetary Fund (IMF), as well as liabilities of foreign exchange, public sector enterprises, banks, and the private sector.

Pakistan’s domestic debt stood at Rs 57.566 trillion by the end of March of fiscal year 2026, reflecting an increase of Rs 30.94 trillion during the first nine months of the fiscal year, which amounted to Rs 54.472 trillion by the end of June 2025.

Pakistan’s total external public debt consists of two components: government external debt and debt secured from the IMF. The government external debt accounts for the majority, amounting to USD 82,261 million, while outstanding debt from the IMF stands at USD 9,891 million.

The IMF debt further consists of the federal government debt (USD 3,620 million) and the central bank’s debt (USD 6,271 million).

The central government’s external debt is predominantly long-term in nature, with USD 68,408 million long-term debt (greater than one year) and USD 13,853 million as short-term debt (less than one year). This is in line with the government’s external debt strategy that prioritizes long-term financing, which typically carries lower repayment pressures.

Among external debt sources, multilateral loans form the largest portion, totaling USD 42,483 million, constituting around 46 percent of total external debt. These loans are provided by development partners like the World Bank and Asian Development Bank and are concessional in nature, with lower interest rates and extended repayment periods.

Debt from the IMF amounts to USD 9,891 million, constituting around 11 percent of total external debt. The Paris Club debt amounts to USD 5,497 million, representing approximately 6 percent of Pakistan’s total external public debt. These loans are also concessional, offering longer repayment periods and lower interest rates. Bilateral loans from non-Paris Club countries amount to USD 19,025 million (21 percent of total external debt).

The Government of Pakistan’s international capital markets debt in the form of Eurobonds and international Sukuk amounts to USD 6,300 million, which constitutes approximately 7 percent of total external debt. These debt obligations are long-term in nature with market-based interest rates. vii. Total Outstanding loans from foreign commercial banks amount to USD 6,323 million, constituting around 7 percent of total external debt. These loans are short-to-medium-term (ie, 1-3 years) with market-based interest rates. Other foreign debt in terms of Naya Pakistan Certificates, non-resident investment in government securities, and Pakistan Banao Certificates, etc., constitutes around 1.5 percent. This category falls under the short-to-medium-term nature of debt with a market-based interest rate. ix. Short-term debt, having a tenor of less than 1 year, amounts to USD 13,853 million, which also includes external holdings of short-term local currency securities (T-bills) of USD 323 million.

In the first nine months of the FY 2026, the total inflows from external debt disbursements amounted to USD 6,101 million. Of this, multilateral sources contributed the largest (USD 2,738 million), followed by commercial/other (USD 2,238 million), which also includes NPCs, and bilateral sources (USD 1,125 million). There were no bond issuances during this period.

Repayments totaled USD 6,250 million, with multilateral creditors receiving the largest portion (USD 2,150 million), followed by bilateral creditors (USD 657 million), International Bonds (USD 500 million), and commercial/other sources (USD 2,944 million).

Interest payments amounted to USD 2,582 million, with the bulk of these payments directed towards multilateral creditors (USD 1,201 million).

The interest payments to bilateral creditors (USD 663 million), international bonds (USD 320 million), and commercial/other sources (USD 398 million) were lower in comparison.

Permanent debt, which primarily comprises medium to long-term instruments such as Pakistan Investment Bonds (PIBs), Government Ijara Sukuk (GIS), and Prize Bonds, rose from Rs 41.8 trillion in June 2025 to Rs 43.9 trillion in March 2026, reflecting an increase of Rs 2.1 trillion during the first nine months of FY 2026.

PIBs increased by Rs 0.7 trillion, GIS, including Bai-Muajjal, rose by Rs 1.4 trillion, and Prize Bonds saw a marginal rise of Rs 20 billion. Overall, permanent debt accounted for nearly 77 percent of total domestic debt, indicating more reliance on medium to longer-term borrowing to ensure debt sustainability.

Floating debt stock was recorded at Rs 9.6 trillion by the end of March 2026, compared to Rs 8.8 trillion in June 2025, showing an increase of Rs 0.8 trillion in the first nine months of the ongoing fiscal year.

The share of floating debt out of total domestic debt was 16.6 percent, which is almost constant at the March 2025 level of 16.1 percent. This is in line with the government’s medium-term debt management strategy to keep net issuance of short-term T-Bills around zero, and rely more on the medium to long-term bond issuances.

The ‘Other’ components of domestic debt increased slightly from Rs 905 billion to Rs 910 billion. Naya Pakistan Certificates declined slightly by Rs 2.4 billion to Rs 59.5 billion. SDR on-lent loan from SBP remained stable at Rs 474.9 billion. Foreign currency-denominated domestic debt is recorded at Rs 376 billion.

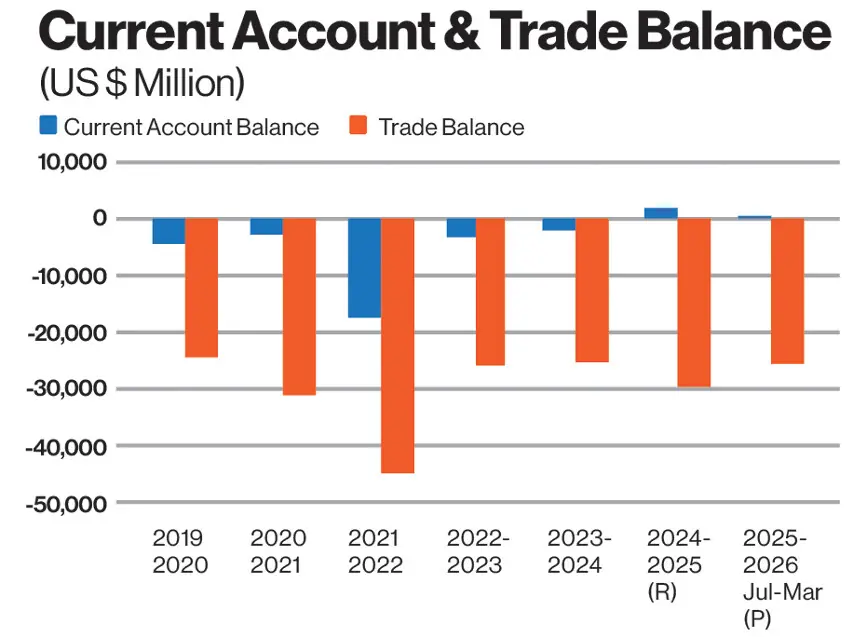

ISLAMABAD: The Economic Survey 2025-26 has revealed that Pakistan’s net exports remained negative, underscoring the persistent need to strengthen export capacity and diversify the country’s export base.

According to the survey, trade openness—measured as the ratio of exports and imports to GDP—stood at around 30 percent, indicating significant potential for deeper integration into global markets.

The exchange rate remained largely stable during the fiscal year, recorded at Rs 280.65 per US dollar compared to Rs 279.35 last year, reflecting a marginal depreciation of just 0.5 percent.

The global trade environment remained challenging in 2025, primarily due to substantial tariff increases by the United States, which heightened trade restrictions and policy uncertainty.

Additional pressures emerged in February 2026 as escalating tensions in the Middle East triggered volatility in energy markets, increased shipping and insurance costs, and disrupted regional supply chains.

Despite these headwinds, Pakistan’s external sector demonstrated resilience. During July–March FY2026, the current account posted a surplus of USD 72 million, supported by strong remittance inflows, reduced primary income outflows, and improved financial account performance.

Workers’ remittances remained a key pillar, rising by 8.2 percent to USD 30.3 billion, largely due to policy and regulatory measures encouraging inflows through formal channels.

However, the merchandise trade deficit widened to USD 27.9 billion from USD 22.7 billion last year, driven by a 6.9 percent increase in imports amid recovering domestic economic activity. Export performance remained subdued, declining by 8 percent due to weak external demand and geopolitical disruptions affecting trade routes.

The services sector provided some relief, with the deficit narrowing to USD 2.1 billion from USD 2.3 billion, supported by robust growth in IT exports, which surged by 19.8 percent.

The primary income deficit also improved, declining by USD 364 million to USD 6.4 billion, mainly due to lower interest payments.

On the financing side, the financial account recorded a net inflow of USD 194 million, compared to a net outflow of USD 1.0 billion last year, primarily due to higher official disbursements.

Foreign exchange reserves increased to USD 21.8 billion by end-March 2026—comprising USD 16.4 billion held by the State Bank of Pakistan and USD 5.4 billion by commercial banks—helping maintain exchange rate stability at around Rs 281 per US dollar during the period.

Exports remained stagnant at approximately 9 percent of GDP, while imports stayed elevated at around 16 percent, largely driven by essential and energy-related purchases. The trade deficit widened further in the third quarter due to the Middle East crisis and rising oil import costs.

To address these imbalances, the government is pursuing structural reforms aimed at enhancing export competitiveness, diversifying export products, and rationalizing tariffs to curb imports.

The Survey noted that wholesale and retail trade grew by 3.71 percent, supported by improved output in agriculture and manufacturing, along with higher import volumes. The services sector maintained steady momentum, with growth reaching 4.18 percent in the third quarter, while wholesale and retail trade expanded by 4.13 percent during the same period.

Looking ahead, the outlook for global trade in 2026 remains uncertain due to ongoing tariff tensions and geopolitical risks, which are expected to slow goods trade. However, services trade is projected to remain relatively resilient, driven by digitalization and rising demand for technology-based services.

Growth in Pakistan’s major trading partners—including China, the United States, the United Kingdom, and the European Union—is expected to remain moderate, potentially weighing on demand for Pakistan’s exports. Nonetheless, continued expansion in IT and digitally delivered services presents an opportunity to offset pressures in the goods sector.

The widening trade deficit was largely attributed to a 7.8 percent increase in import payments during July–March FY2026, reflecting stronger demand for industrial inputs as economic activity picked up. Rising global oil prices further exacerbated the import bill, with Brent crude increasing from USD 62.7 per barrel in December 2025 to USD 103.7 in March 2026.

Meanwhile, goods exports declined by 5.8 percent, mainly due to reduced food exports—particularly rice—amid weak global demand, flood-related losses, and disruptions in Pak-Afghan trade following border tensions since October 2025.

Pakistan’s export of fish and fisheries products has seen consistent growth, reflecting rising global demand for seafood. Pakistan’s top buyers included China, Thailand, United Arab Emirates (UAE), Malaysia and Japan.

In July-March FY 2026, Pakistan exported a total of 200 thousand MT of fish and fisheries products earning approximately US USD 405.1 million in export revenue.

Encouragingly, the services account continued to provide a buffer, with exports growing by 17.2 percent, outpacing import growth of 10.7 percent. This improvement reflects the increasing role of IT and digitally enabled services in strengthening Pakistan’s external account.

KARACHI: The banking sector of Pakistan has demonstrated steady performance with key financial soundness indicators pointing to stability in capital adequacy, earnings, and asset quality.

Economic Survey of Pakistan for the year 2025-26 also highlighted that the financial sector has maintained resilience amid broader economic pressures, underscoring gradual improvements in overall banking sector fundamentals.

According to survey, the banking sector’s asset base grew by 17.8 percent YoY during CY2025, reaching Rs 63.2 trillion by the end of December 2025, mainly driven by investments.

On the funding side, deposit growth accelerated to 24.7 percent to Rs 37.659 trillion by end of December 2025. Deposits remained the mainstay of funding, financing 62.7 percent of the asset base, while borrowings financed 25.1 percent.

The Capital Adequacy Ratio (CAR) improved to 20.8 percent by the end of December 2025 from 20.6 percent a year earlier. The prevailing CAR is well above the domestic and international minimum benchmarks of 11.5 percent and 10.5 percent, respectively.

Earnings also remained steady, with after-tax profit of the banking sector rising to Rs 716 billion in CY25, up from Rs 644 billion in CY24.

Asset quality profile remained broadly stable and the non-performing loan (NPL) to gross loan ratio fell to 6.1 percent in December 2025 from 6.3 percent in December 2024. The net NPLs-to net loans ratio further improved to negative 0.5 percent in December 2025 from negative 0.3 percent in December 2024, indicating muted credit risk in the delinquent portfolio on a net basis.

Since its inception, Islamic banking in Pakistan has also demonstrated substantial growth. Total assets of Islamic Banking Institutions (IBIs) increased by Rs 3,397 billion by the end of December 2025, representing a YoY growth of 30.7 percent to reach Rs 14,467 billion.

Similarly, deposits rose by Rs 3,132 billion or 39.6 percent to Rs 11.037 trillion by the end of December 2025. Consequently, Islamic banking accounted for 22.9 percent of the overall banking industry’s assets and 27.8 percent of its deposits.

Financial Sector Reforms during July-March FY 2026 is also encouraging. In line with the SBP strategic Plan 2023-28 and Vision 2028, the SBP continued to undertake reforms to maintain price and financial stability, promote financial inclusion, strengthen resilience, and support a technologically advanced financial system.

The SBP has developed a comprehensive Cyber Resilience Strategy, namely Cyber Shield 2025-30, for the SBP regulated entities.

As the banking ecosystem faces an increasingly sophisticated cyber threat landscape, the strategy aims to enhance cyber defenses of the SBP regulated entities through a holistic, adaptive and collaborative approach built upon five foundational pillars, namely strengthening cyber resilience, maturing cyber security governance, enhancing collaborations and partnerships, developing cyber workforce and continuously evolving the cyber security programs.

ISLAMABAD: The manufacturing sector registered a strong recovery during 2025-26, as the Large Scale Manufacturing (LSM) sector witnessed a growth of 6.5 percent, a sharp turnaround from the –0.69 percent contraction last year, revealed the Economic Survey 2025-26 released here on Thursday.

According to the Economic Survey, notable growth was observed in food (9.77 percent), tobacco (11.70 percent), petroleum products (10.92 percent), rubber products (14.26 percent), electrical equipment (11.87 percent), automobiles (61.66 percent), transport equipment (39.93 percent), furniture (20.45 percent), and other manufacturing (football, 23.06 percent).

However, pharmaceuticals (–5.14 percent) and machinery & equipment (–8.72 percent) recorded negative growth.

Electricity, gas and water supply contracted by 10.63 percent, reflecting a 24.9 percent decline in subsidies (from Rs 1,190 billion to Rs 893billion), slower output from distribution companies, and a 2.7 percent rise in the electricity deflator.

The construction sector grew by 5.73 percent, down from 8.77 percent last year, supported by higher construction-related expenditure across private, public, and general government sectors.

The rebound in LSM was primarily supported by relative monetary easing, as the policy rate declined substantially to 10.5 percent by December 2025, from its peak of 22 percent in FY 2024, reducing borrowing costs and improving liquidity conditions for businesses.

Although the policy rate was subsequently raised to 11.5 percent at the end of April 2026 in response to emerging geopolitical risks, liquidity conditions during most of FY 2026 remained comparatively supportive.

The earlier monetary easing is expected to continue supporting industrial activity in the coming months. This improvement in financial conditions was also reflected in credit flows to industry, where lending to high-weighted manufacturing sectors expanded during July-March FY 2026, with either working capital or fixed investment financing showing an upward trend.

The increase in working capital financing supported short-term production needs amid improving liquidity, while the rise in fixed investment lending indicates a gradual revival in capacity expansion.

Within manufacturing, credit growth was broad-based, with notable contributions from food products, textiles, wearing apparel, non-metallic mineral products, and motor vehicles.

In addition, tariff rationalization measures introduced under the National Tariff Policy supported industrial activity by facilitating easier access to imported raw materials, intermediate goods, and industrial machinery at relatively lower costs, thereby improving competitiveness and production efficiency.

The improved performance also reflects easing inflationary pressures, a stable exchange rate, better foreign exchange availability, and a gradual recovery in domestic demand.

Improved availability of imported inputs and reduced supply-side disruptions enabled industries to operate at relatively higher capacity utilization levels compared to previous years.

On a year-on-year (YoY) basis, LSM grew by11.1 percent in March 2026, compared to a contraction of 2.4 percent in the same month last year.

Meanwhile, on a month-on-month (MoM) basis, LSM declined by 5.2 percent in March 2026, compared to an 8.8 percent decline in February 2026.

Out of 22 industrial groups, 16 recorded positive growth during July-March FY 2026, with the main contribution from Food, Wearing Apparel, Automobile, and Coke & Petroleum products.

The food group recorded a strong growth of 9.8 percent during July-March FY 2026 against the contraction of 3.2 percent last year. Notable growth of 31.0 percent was observed in the production of sugar, bakery products, and chocolate and sugar confectionery, supported by better crop harvests, thus contributing to the overall growth of the food group.

Wheat and rice milling and cooking oil also remained positive with 1.4 percent and 1.2 percent growth in production during the reviewed period. In contrast, tea blended, vegetable ghee, and starch & its products observed contraction of 10.0percent, 3.0 percent, and 0.02 percent, respectively.

Meanwhile, the beverages sector posted a growth of 7.7 percent, driven by strong performance in juices, syrups & squashes.

The textile sector growth remained moderate at0.7 percent during July-March FY 2026, compared to a growth of 2.5 percent in the same period last year.

Growth in yarn (1.8 percent), cloth (0.2 percent), woolen & worsted cloth(32.4 percent), and woolen blankets (7.8 percent)were the key contributors to the sector’s performance.

Moreover, the increasing demand for fixed investment borrowing, along with an increase in textile machinery imports (20.9 percent), signals the industry’s intent to expand and modernize operations, reinforcing positive growth prospects in the coming months.

However, challenges persist in the jute segment, where output of jute goods declined sharply by 35.3 percent due to continued operational inefficiencies. The wearing apparel sector sustained its growth momentum with 6.6 percent growth during July-March FY 2026, against 7.6 percent in the same period last year.

The continued expansion reflects the strengthening position of the ready made garment industry, driven by improved competitiveness and rising demand in both domestic and international markets. This is further evidenced by a 5.9 percent increase in export quantity and a 3.8 percent rise in export values during July-March FY 2026. Coke and Petroleum products posted a strong growth of 10.9 percent in July-March FY 2026, against 4.9 percent last year.

The main contributors to this performance were high-weighted products such as high-speed diesel (18.1 percent), motor spirit (14.5 percent), diesel oil (309.6 percent), jet fuel oil (7.5 percent), and petroleum products n.o.s. (53.1 percent), reflecting increased demand from the transport, industrial, and power generation sectors.

The automobile sector maintained its growth momentum, recording a growth of 61.7 percent during July-March FY 2026, against the growth of 40.0 percent in the same period last year. This robust performance reflects improved macroeconomic fundamentals, including declining inflation, exchange rate stability, and alower policy rate, which collectively reduced borrowing costs and restored consumer andinvestor confidence.

Other transport equipment also performed well with 39.9 percent growth during the period under review.

Tobacco, paper & board, and computer, electronics & optical products remained positivewith 11.7 percent, 0.1 percent, and 1.2 percent,respectively. Although their weights in the manufacturing index are relatively small, their positive contributions reflect improving industrial activity in these segments.

The pharmaceuticals sector contracted by 5.1 percent during July-March FY 2026, comparedto a 2.3 percent increase in the same period lastyear. This deceleration reflects a more subduedperformance in liquids/syrups, injections, andcapsules, while galenical, ointments, and tablets witnessed the growth of 100 percent, 6.5 percent,and 0.9 percent, respectively.

The sectorcollectively contributed a negative 0.31 percentage points to cumulative LSM growth.

The chemicals sector contracted by 1.4 percent during July-March FY 2026, against thecontraction of 5.5 percent last year. Within this group, chemical products declined by 2.2 percent, driven by reduced output in industrial chemicals and basic materials, while fertilizer production declined marginally by 1.0 percent.

The non-metallic mineral products grew by 8.2percent during July-March FY 2026, against a 10.5 percent contraction in the same period lastyear.

The expansion was largely driven by risingdemand from construction-related activities, reflected in a 9.1 percent increase in cement production. Growth in electrical equipment by 11.9 percent further reinforced the improving momentum in construction and allied industrial activities.

The iron and steel sector continued to underperform, recording a contraction of 6.3percent during the period under review. However, imports of iron and steel increased by 5.5 percent in value terms and 10.5 percent in quantity terms during the period under review,indicating a shift toward imported products tomeet domestic demand.

Other manufacturing (football) recorded substantial growth of 23.1 percent during July March FY 2026, supported by strong external demand for footballs ahead of the FIFA World Cup 2026, reinforcing Pakistan’s strong position in the international sports goods market. Furniture production also turned positive with 20.5 percent growth after a sharp contraction of 61.1 percent last year.

ISLAMABAD: The ongoing global situation and volatility in oil prices are likely to influence inflation in Pakistan, according to the 2025–26 Economic Survey released on Thursday.

The Economic Survey said that the global uncertainties, particularly ongoing conflicts and oil price volatility, may influence inflation and macroeconomic conditions in the near term, requiring continued policy vigilance.

The inflation remained contained for most of FY2026, but escalating global energy prices linked to the Middle East conflict pushed headline inflation to 7.3 percent in March 2026.

In response, the State Bank of Pakistan (SBP) raised its policy rate by 100basis points to 11.5 percent in April 2026.

Despite these challenges, continued policy discipline and structural reforms are expected to strengthen resilience and competitiveness, supporting sustainable and inclusive economic growth over the medium term.

ISLAMABAD: Total tax exemptions, concessions/reduced rates, zero-rating and special tax treatments to various businesses, sectors/industries, lobbies/groups and investors have cost the government Rs 2,352.81 billion in 2025-26 against the downward revised figure of Rs 2,434.73 billion in 2024-25, reflecting a decrease of Rs 81.92 billion.

The Economic Survey (2025-26) released on Thursday, revealed that the cost of tax exemptions showed a decrease of 3.36 per cent during 2025-26 as compared to tax exemptions in 2024-25.

However, tax expenditure (cost of exemptions) totaled at Rs 2,352.81 billion during 2025-26 as compared to the original figure of Rs 5,840.2 billion in 2024-25, reflecting a massive decrease of Rs 3,487.39 billion. The figure of Rs 5,840.2 billion for the cost of tax exemptions was given in the Economic Survey (2024-25) issued last year.

In this case, the cost of tax exemptions witnessed a decrease of 59.71 per cent during 2025-26 as compared to tax expenditure in 2024-25.

The tax expenditure figure of Rs 2,352.81 billion for 2025-26 has been mentioned in the Economic Survey (2025-26) launched here on Thursday.

It is important to mention that the Ministry of Finance had issued a figure of Rs 5,840.2 billion of tax expenditure for 2024-25 last year.

Later, the Ministry of Finance has downward revised the tax expenditure figure for 2024-25 from Rs 5,840.2 billion to Rs 2,434.73 billion, reflecting a decrease of Rs1,850.5 billion. The Ministry of Finance has issued “Errata” of the tax expenditure figure for 2024-25 in last year’s Economic Survey (2025).

If the total cost of exemptions (Rs 2,352.81 billion) during 2025-26 has been compared with the downward revised figure of 2024-25, i.e.,Rs 2,434.73 billion, the total cost of tax exemptions now stands at Rs 81.92 billion for 2025-26.

Breakup of downward revised tax expenditure figures or corrected figures for 2024-25 revealed that the cost of income tax exemption was Rs 545.23 billion; sales tax Rs 1,237.11 billion and customs duty Rs 652.39 billion, taking total to revised figure of Rs 2,434.73 billion, as per corrected summary of tax expenditure (Errata) for 2024-25.

The tax-expenditure report-2026 pinpointed that sales tax exemption to petroleum products, duty concessions on imports, reduced rates of sales tax, and overall sales tax exemptions on imports and local supplies were major contributors to the increased revenue loss during 2025-26.

The latest survey has not mentioned revenue loss on account of tax exemptions available to industrial units located in erstwhile tribal areas during 2025-26.

The revenue loss due to sales tax exemption from imports and local supplies stood at Rs 566,949 billion in 2025-26.

The Economic Survey (2025-26) disclosed that the sales tax expenditure remained the highest during 2025-26 as compared to revenue loss on account of income tax and customs duty. All kinds of sales tax exemptions/concessions caused revenue loss of Rs 1,273,977 million; followed by income tax loss of Rs 579,698 million and customs duty revenue loss of Rs 499,136 million during 2025-26.

The survey disclosed that the fixed sales tax regime on cellular mobile phones caused a revenue loss of zero rupees in 2025-26 as compared to Rs 87,950 million in 2024-25. The Federal Board of Revenue (FBR) has suffered a revenue loss of Rs261 billion on account of sales tax exemption on imports during 2025-26 as compared to Rs372 billion during 2024-25, reflecting a decrease of Rs111 billion.

Sales tax exemption on local supplies caused a revenue loss of Rs305 billion in 2025-26 as compared to Rs613 billion in 2024-25, reflecting a decrease of Rs308 billion.

The cost of income tax exemptions amounted to Rs579.7 billion against Rs800.8 billion, showing a decrease of Rs221.1 billion and the cost of customs duty exemptions was Rs499.14 billion in 2025-26 against Rs785.8 billion in 2024-25, reflecting a decrease of Rs286 billion.

The Economic Survey has not mentioned revenue loss on account of the exempt business income granted to independent power producers (IPPs).

Similarly, the survey has not mentioned any revenue loss from capital gains. The accumulative revenue loss on account of tax credits amounted to Rs75,940 billion in 2025-26 against Rs101 billion in 2024-25, showing a decrease of Rs26 billion.

The income tax exemption from special provisions of the Income Tax Ordinance has caused revenue loss of Rs10.9 billion during 2025-26 as compared to Rs41.1 billion in 2024-25.

The income tax exemption from total income has revenue impact of Rs 437,996 billion during the period under review.

The income tax exemption available to the deductible allowances caused revenue loss of Rs 4.01 billion in 2025-26 against Rs 16.4 billion in 2024-25, showing a decrease of Rs 12.4 billion.

The reduction in income tax rates has revenue implications of Rs50.71 billion during 2025-26 as compared to Rs 45 billion in 2024-25, showing an increase of around Rs 5 billion.

The FBR has suffered a massive revenue loss of Rs566.95 billion in 2025-26 as compared to Rs985.594 billion in 2024-25 due to sales tax exemptions available under the Sixth Schedule (Exemption Schedule) of the Sales Tax Act. The loss on account of sales tax exemption (import and domestic stage) has been decreased by nearly Rs565 billion.

The FBR has suffered a loss of Rs635.841 billion due to sales tax exemptions available under the Eight Schedule (Conditional Exemption/reduced rates) of the Sales Tax Act, 1990, during the period of 2025-26 against Rs617.347 billion in 2024-25. The revenue loss from conditional exemptions has been decreased by Rs635.22 billion. The total revenue loss from the zero-rating facility granted to various sectors under the Fifth Schedule of the Sales Tax Act, 1990, amounted to Rs8.774 billion during the period under review against Rs 6.83.429 billion in 2024-25. The FBR has not specified any revenue loss to the exemptions within the federal excise regime, reflecting no loss occurred on this account. The cost of income tax exemptions was Rs579.7 billion in 2025-26 against Rs800.8 billion in 2024-25.

The cost of exemptions in respect of customs duty has been calculated at Rs499.14 billion in 2025-26 as compared to Rs785.9 billion in 2024-25, reflecting a decrease of Rs286.76 billion.

The exemption of customs duty available under Chapter-99 (special classification provisions) of the Customs Act has caused a revenue loss of Rs 17 billion in 2025-26 against Rs 33.481 billion in 2024-25, reflecting a decrease of Rs 1.383 billion.

The concessions under the Fifth Schedule of the Customs Act, 1969 caused a revenue loss of Rs 205.655 billion in 2025-26 against Rs 379.746 billion in 2024-25, reflecting a decrease of Rs174.091billion.

The FBR has suffered revenue loss of zero rupees in 2025-26 against Rs 61 billion in 2024-25 on account of tariff concessions and exemptions available under Free Trade Agreements (FTAs) and the Preferential Trade Agreements (PTAs).

Similarly, exemption of customs duty on the items by the automobile sector, exploration and production (E&P) companies, general concessions and the CPEC caused a loss of Rs 275.772 billion in 2025-26 against Rs 133.236 billion in 2024-25, showing an increase of Rs142.48 billion.

The export-related exemptions cost revenue loss of zero rupees during 2025-26 against Rs178.435 billion during 2024-25.

ISLAMABAD: The country’s overall electricity consumption has posted a growth of 3.8 per cent during the first nine months (July-March) of 2025-26 whereas domestic and agriculture consumption showed a declining trend due to relative structural shift to alternative energy sources due to tariff hikes, which have reduced affordability and incentivized conservation.

According to Economic Survey 2025-26, as of July-March FY 2026, Pakistan’s total installed electricity generation capacity stood at 49,651 MW, reflecting an 8.5 percent increase compared to 45,782 MW recorded in the corresponding period of FY 2025.

The increase can be attributed to the installed capacity of 7,319 MW from net metering. However, out of 102 commissioned IPPs, 13 IPPs of 5,105 MW combined capacity have been closed for various reasons. These include 9 RFO based IPPs of 2,877 MW), 3 gas/RLNG-based IPPs of 601 MW, and 1 multi-fuel-based IPP of 1,638 MW.

The percentage shares of hydel, nuclear, renewable, and thermal are 23.4 percent, 7.1 percent, 20.3 percent, and 49.2 percent, respectively. The share of thermal power as the dominant source of electricity supply has declined over the past few years, highlighting an increased reliance on indigenous sources.

Out of the total electricity generation of 92,835 GWh, the share of hydel, nuclear, and renewable stands at 53.1 percent. This shift marks a positive development of the economy, as the energy mix transitions away from thermal generation towards more sustainable and environmentally friendly alternatives. During July-March FY 2026, total electricity consumption in Pakistan stood at 83,143 GWh, compared to 80,811 GWh in the corresponding period of FY 2025, reflecting a 3.8 percent increase in electricity usage.

The household sector continued to dominate electricity consumption, with its share declining to 47.5 percent (39,472 GWh) during July-March FY 2026, down from 49.6 percent (39,730 GWh) in the same period of FY 2025. This decrease indicates a relative structural shift to alternative energy sources due to tariff hikes, which have reduced affordability and incentivized conservation.

In contrast, industrial consumption increased to 26,205 GWh, up from 21,083 GWh, increasing its share from 26.3 percent to 31.5 percent.

Electricity usage in the agriculture sector dropped significantly by 42.3 percent, falling from 4,566 GWh to 2,636 GWh, which reduced its share from 5.7 percent to 3.2 percent. This sharp decline is likely due to changes in irrigation practices, rainfall patterns, and possibly a switch to diesel-powered or solar alternatives in response to rising electricity costs.

The commercial sector recorded a modest increase in consumption, from 6,898 GWh to 7,044 GWh. This rise indicates a marginal pickup in business and retail activity, particularly in urban centers. The “others” category, comprising public lighting, bulk supply, and government buildings, consumed 7,785 GWh, slightly decreasing its share from 9.8 percent to 9.4 percent.

During the review period, key milestones were achieved, as 32 MW bagasse-based Shahtaj Sugar Mills power plant achieved Commercial Operations Date (COD) on 10 October 2025 and started supplying the national grid 126 million units of clean energy annually over its 30-year lifespan.

The Prime Minister of Pakistan has granted in-principle approval for processing of a 40 MW power project in the Gwadar region.

To establish a more balanced, transparent, and sustainable framework for Distributed Energy Resources (DERs), the government is considering a transition from net-metering to net-billing. Thar coal supply commenced in September 2025 and is being gradually ramped up, with full-scale supply planned by March 2026.

The commercial operation date (COD) for Phase-3, along with full lignite coal utilization, is expected by the third quarter of 2026, ensuring the plant operates entirely on local coal.

During the period from 1 July 2025 to 31 December 2025, significant progress was made on the conversion of the 660 MW Jamshoro Power Project to Thar coal. Pakistan has 175 billion-ton Thar Coal Reserve, which is sufficient to provide a cost-effective and indigenous fuel option for base load power generation for decades to come. So far, five Thar Coal-based IPPs of 3,300 MW have been commissioned through PPIB, which provide inexpensive electricity to the national grid. These projects include: (i) 1320 MW Thar Coal Block-1 Company (Shanghai) at Thar Block-1 ;(ii) 660 MW Engro Power Project at Thar Block-II; (iii) 660 MW Lucky Electric Project at Port Qasim; (iv) 330 MW Thar Energy Limited Project at Thar Block-II; (v) 30 MW Thal Nova Project at Thar Block-II.

Nevertheless, there is still a need to harness Thar’s coal potential as much as possible for meeting the country’s electricity and energy needs.

In this regard, GoP has already imposed a moratorium on the processing of new imported fuel-based power projects since 2016. Due to the increased prices of imported coal in the international market, the GoP took the initiative to substitute imported coal-based IPPs with Thar coal. Subsequently, efforts are under way to start blending Thar coal by three imported coal-based IPPs with a cumulative capacity of 3,960 MW which were implemented under the CPEC regime.

Six nuclear power plants (NPPs) are operating at two different sites with a total installed capacity of 3,530 MW. Chashma Nuclear Power Generating Station (CNPGS) near Mianwali comprises four units (C-l, C-2. C-3 & C-4) with a total capacity of 1330 MW.

Karachi Nuclear Power Station (KNPGS) has a total capacity of 2,200 MW and is located on Karachi coast.

The performance of Pakistan’s Nuclear Power Plants is up to the mark compared to international standards. These NPPs are placed at the top notch among thermal power generation options in the national merit order.

Over the past six months of the current fiscal year, the overall capacity factor of nuclear capacity is about 80 percent despite the challenges of low demand in the country.

The electricity, gas, and water supply industry contracted due to a decline in subsidies, slow growth in the output of WAPDA and companies, and an increase in the deflator.

KARACHI: The benchmark KSE-100 index of Pakistan Stock Exchange (PSX) outperformed the major world stock market indices, with its market capitalisation reaching USD 59.23 billion as of March 31, 2026, according to Economic Survey of Pakistan released on Thursday.

This performance is supported by an improving macroeconomic environment, successful reviews under the IMF’s Extended Fund Facility (EFF) programme, strengthening investor confidence, and continued financial inflows from bilateral and multilateral partners.

According to Pakistan Economic Survey 2025-26, the performance of Pakistan’s capital markets, especially stock market remained encouraging during the first nine months of FY 2026. During July-March FY26, the KSE-100 index continued to strengthen supported by encouraging macroeconomic indicators, a favorable external account, lower inflation, and a fresh wave of investor confidence in the government’s reform agenda.

During the period, the PSX’s benchmark KSE-100 index registered a significant growth of 18.4 percent from 125,627 to 148,743 points. During the period under review, the index closed at its highest level of 189,167 points on January 23, 2026, while the lowest level was observed at 128,199 points on July 01, 2025.

However, the momentum faded towards the beginning of the February 2026 as uncertainty emerged in the wake of tension with Afghanistan as well as escalating geopolitical tensions in the region, higher global oil prices, foreign selling, domestic profit-taking, and the seasonal slowdown during Ramadan.

PSX’s market capitalisation increased to 8.5 percent to reach Rs 16,534 billion (USD 59.23 billion) on March 31, 2026 compared to Rs15,237 billion (USD 53.00 billion) on June 30, 2025.

The average daily volume surged to 1206 million shares during July-March FY 2026, compared to 834 million shares in FY 2025. As of March 31, 2026, the number of listed companies stood at 536, with total listed capital of Rs 1,626 billion and market capitalisation of Rs 16,534 billion.

On the other hand, the major Asian markets’ performance remained mixed from end-June 2025 to end-March 2026. Korean Composite Stock Price Index-KOSPI remained the most attractive market for investors with an unprecedented increase of 64.5 percent followed by Set Index of Thailand (32.9 percent), VN30 Index of Vietnam (23.8 percent), FTSE Straits Times of Singapore (23.2 percent), KSE-100 (18.4 percent), and MSCI Emerging Market Index (13.8 percent). However, decline has been observed in the BSE Sensex 30 of India and the PSEi Composite of the Philippines.

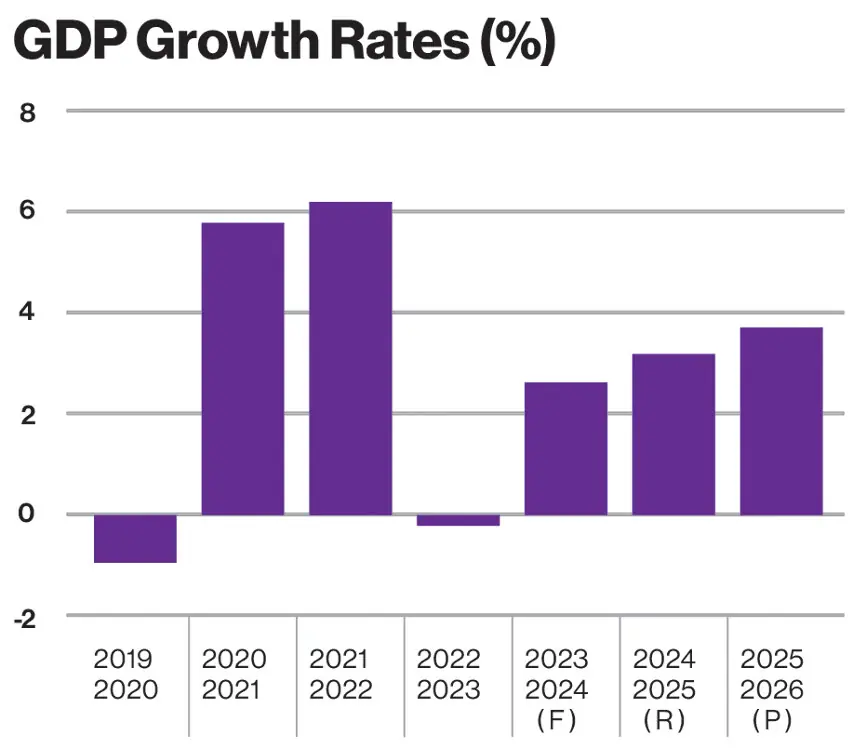

ISLAMABAD: Growth target of 4.2 percent set for the outgoing fiscal year 2025-26 has been missed by 0.5 percent and estimated at 3.7 percent due to three exogenous factors, notably the Middle East conflict, the floods in September, and the Trump tariffs.

This was stated by Finance Minister Muhammad Aurangzeb while unveiling the Economic Survey 2025-26 presented traditionally a day prior to the presentation of the budget for the next fiscal year.

He was flanked by the Planning Minister Ahsan Iqbal, Chairman Federal Board of Revenue Rashid Langrial and the head of the department that authored the Survey, Dr. Raja Hasan M. Mohsin, the Economic Advisor.

The growth rate is higher than last year’s growth of 3.18 percent but falls short of its target of 4.2 percent, said Aurangzeb, adding that it is a story of resilience and discipline shown during the outgoing fiscal year.

The finance minister said that GDP growth in fiscal year 2023 was -0.2 percent, 2.6 percent in fiscal year 2024, and 3.2 percent in fiscal year 2025.

Earlier, GDP growth was estimated to exceed 4 percent, but it did not happen due to the ongoing conflict in the Middle East. “But having said that, we have still reached a historically high size of the economy at Rs126.9 trillion,” he said.

The country’s economy had risen above USD452 billion, with per capita income increasing 9 percent to USD1,901, which was USD1,751.

He said the country began the outgoing fiscal year with uncertainty due to tariffs. “Then, by the end of July, we reached a point where we could be in a competitive position with respect to our exports, especially to the US,” he added. Then there were floods in August and September 2025, followed by a regional conflict in March this year.

“These challenges tested Pakistan’s resilience,” he said, adding that the government was able to deal with them and remained on the path of moving from stabilization to growth. Pakistan faced three major challenges and addressed them effectively. “These factors affected not only Pakistan and the region but the entire world,” he said, noting that global growth had also slowed.

The finance minister said that the government has successfully negotiated the first-order impact of the conflict, but its impact would be felt in the coming months.“Our oil imports, which shot up above USD1 billion in April, were lowered to half a billion dollars in May, because we are now trying to manage the inflows,” he said.

“Whereas, the second-order impact of this conflict is being observed in the rising inflation rate, which has led to an increase in the policy rate,” he said.

Aurangzeb added that he remains optimistic that the country’s leadership mediating efforts would be successful. “But the reality is that the energy infrastructure has been hit and continues to be hit. We are taking that into vis-à-vis our contingency,” he added.

“We have not only increased the size of the economy but also achieved broad-based recovery,” he said, adding that the country had reached the largest economic size in its history. The agriculture sector recorded growth of 2.9 percent, with good growth seen in the crops sector.

“The improvement owes to effective macroeconomic management, better fiscal account, growth in the LSM sector, resilience of the agriculture sector to floods of 2025, exchange rate stability, and reforms under the IMF Extended Fund Facility (EFF) Programme,” it stated. Aurangzeb also pointed out that global growth had reduced to 3.1 percent from 3.7 percent due to the factors he elaborated on earlier in the press conference.

Giving a sector-wise breakdown, he said growth in agriculture was recorded at 2.89 percent, compared to 1.53 percent in the last fiscal year. “This was despite floods,” he said, adding that the crop sub-sector showed positive growth. It was recorded at 1.44 percent, the finance minister said. He added the livestock sector also “continues to go from strength to strength”.

Aurangzeb said 6.1 percent growth was recorded in large-scale manufacturing (LSM) in fiscal year 2026, which was the highest in the last four years. He elaborated that positive growth was seen in 16 of LSM’s 22 sub-sectors. “So it’s not one single sector that is leading or contributing to this 6.1 percent turnaround in LSM. It is broad-based growth,” he said.

“To give you some examples, there was a 10 percent increase in the demand for cement, 17 percent for fertiliser, 5 percent for petroleum, 31 percent for automobiles, and 9 percent for mobile phones.”

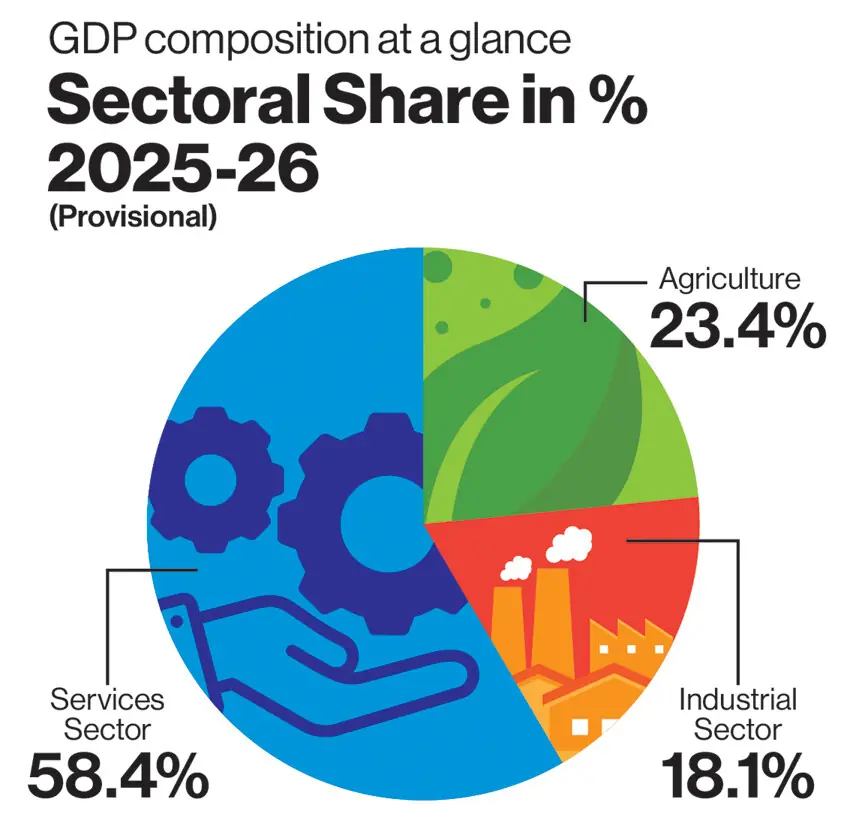

Noting that the services sector made up close to 58 percent of GDP, he said 4.09 percent growth was recorded in this sector in the outgoing fiscal year. “This, too, is the highest in the last four years,” he said.

Aurangzeb particularly mentioned communication and information services, which he said recorded a growth of 7.52 percent. The growth in this sub-sector in fiscal year 2026 was also the highest over the past four years.

He said 175,000 new investors have entered the equity sector, and for the first time in 20 years, 11 initial public offerings (IPOs) have been completed this year. It is often mentioned that some companies have left the country, but at the same time, many global firms, including Aramco, Alibaba, Turkish Petroleum, Veon, and Google, have also increased their investments, he said. “We remain in contact with all friendly countries, including Saudi Arabia and China,” he added. The government admitted low investment savings and regulatory burden, while saying that has to move in right direction and at great speed.

He said 40 to 45 percent of the debt is concessional, long-term, and bilateral, and the debt-to-GDP ratio is continuously declining.

Remittances are expected to cross USD41 billion this year, with the UAE contributing over USD1 billion out of total inflows of USD4.2 billion in May alone. “The UAE has supported us for the longest time, and we are thankful to them. The only responsibility of a borrower is when someone asks them to pay back, you pay back,” Aurangzeb said.

Foreign exchange reserves stand above USD17 billion, and by the end of June, the State Bank expects them to exceed USD18 billion. Overall, foreign exchange reserves reached USD22.6 billion.

The survey document stated that the fiscal deficit “narrowed significantly” to 0.7 percent of GDP (Rs 856.4 billion) from 2.6 percent of GDP (Rs 2,970 billion) in the corresponding period last year. Further primary surplus also improved to 3.2 percent from 3 percent, the survey document said.

Aurangzeb said that tax revenues had increased by 10.1 percent, and markup payments saw a decrease of 23 percent, which he said increased fiscal space.

“The increase in tax revenues was contributed to by growth in both federal and provincial tax collections. FBR tax collection increased by 10.1 percent to Rs9,305.9 billion, while provincial tax revenues increased by 25.8 percent to Rs860.7 billion,” the survey document stated.

On this, Aurangzeb said digital production monitoring had been introduced in various sectors, and he particularly mentioned the cement and sugar sectors. “In these sectors, we have received Rs60 billion additional revenue because of digital production monitoring,” he said, adding that this mechanism was also being introduced in other sectors. Moreover, he said AI-based audit selection had yielded an additional Rs34 billion in revenue.

He also said that the government intended to increase the number of merchants using digital payments to two million by June 2026, and “we are close to about 1.7 million. So, we are getting there”.

He said the government planned to increase the number of digital banking users to 120 million by June 2026 and had exceeded that target, as the number had reached 133 million. “First, we get demand for broadening the tax net, but when we start enlarging the tax base, we get criticism,” the finance minister said. The government has identified 3.5 to 4 million small shopkeepers for tax net expansion.“Any organizational culture, such as nepotism, does not change in a couple of years,” he added.

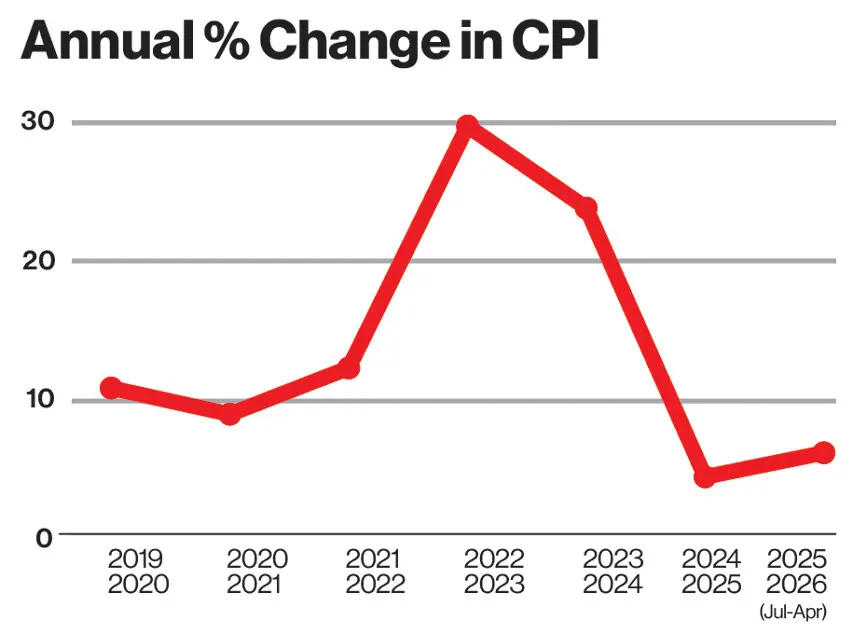

According to the economic survey, CPI inflation for the period between July-April 2025-26 was recorded at 6.2 percent, against 4.7 percent during the same period last year.

“Inflation measured by the sensitive price indicator (SPI) stood at 4.1 percent as against 4.8 percent during the same period last year. The inflation remained broadly stable during the first three quarters of fiscal year 2026.

However, the emergence of an external shock amid geopolitical tensions at the end of the third quarter has increased its vulnerability to renewed price pressures, warranting continued vigilance and timely policy response to preserve macroeconomic stability,” the survey document said. Aurangzeb argued that inflation had been decreasing over the years.

The survey document stated that on the external front, the current account recorded a marginal surplus of USD72 million during July-March 2025-26 compared to a surplus of USD1.7 billion in the same period last year.

“Workers’ remittances remained a key source of external sector support, rising by 8.2 percent to 30.3 billion,” it said. In this regard, Aurangzeb said a debate had been ongoing regarding exports and remittances. But it was not an “and/or discussion. This is an and /and discussion”, he said.

Acknowledging that there was a need to increase exports, he argued that remittances were also an important structural component of economies that were compared to Pakistan in this regard.

“We can debate how much remittances should be contributing to the GDP and to what extent we should rely on them, but remittances are and would remain a very important component of our external balancing position as we move forward,” he said.

The finance minister said the decline in the country’s exports was led by the food sector. “In the food sector, our rice exports have declined by USD1.1 billion,” he said, adding that a decline of USD403 million was recorded in sugar exports. Overall, a decline of around USD1.5 billion was recorded in food exports, he said.

On the other hand, he said, textile exports had increased. He also highlighted the increase in the export of sports goods, mentioning that the football that was to be used during the upcoming FIFA World Cup was manufactured in Pakistan.

He said that from July-May 2025-26, 18 percent growth was recorded in the export of sports goods. The minister said the country’s IT exports had crossed USD3.8 billion, expressing hope that they would reach USD4.5 billion. In this connection, he said the freelancer export was now touching USD900 billion.

He said the country’s foreign exchange reserves currently stood at USD17 billion, hoping that they would reach USD18 billion by the end of June. “This will give us three months of export cover, which is an internationally recognized standard, and this should allow us to further upgrade over the course for the next year,” he said.

According to the economic survey, foreign exchange reserves stood at USD20.6 billion as of April 17, including USD 15.1 billion held by the State Bank of Pakistan, “reflecting strengthened external buffers”.

Replying to a question regarding negotiations with the IMF on budget, he said that negotiations are positive. Regarding another question on retaining provincial’s share, the minister said that it would be for more than year for strategic purposes. He also said that a new tax operating model would be announced in the budget on Friday (today).

The finance minister said if local industrialists invest, foreign investors will also come. He said USD600 million was invested in the privatization of PIA.

Companies from the telecom and energy sectors both entered and exited the market, while foreign companies also participated in the 5G spectrum auction.

The finance minister said the country’s debt currently stands at 68% of GDP.

Agricultural loans increased by 22%, while another figure showed a 15% rise in agricultural lending. He said the government is bringing austerity measures for small farmers. A total of Rs90 billion has been approved for low-income housing. Aurangzeb said the end rate in the housing sector will be fixed for 10 years.

The finance minister said efforts are underway to reduce energy costs. He said cross-subsidies for industries have been abolished to reduce financing costs for the industrial sector. Three power distribution companies will be privatized this year. The policy rate increased due to regional conflict, he added.

The literacy rate in the country has reached 63%. The finance minister said positive results of difficult economic reforms have started to emerge. He added that the textile sector remains central to exports, while the petroleum sector grew by 5%. Panda Bonds were also successfully launched during the year.

Aurangzeb further said the Pakistan Stock Exchange investor base had exceeded 563,000, with a record 11 new companies listed this year. He noted that over 39,000 companies had been registered, bringing the total to more than 297,000.

According to him, private sector credit increased by Rs 934 billion during July–March, while agricultural financing reached Rs 2.162 trillion.

The Planning Minister said Pakistan has failed to build an export-led economy. “Nine million overseas Pakistanis send USD40 billion annually while 250 resident Pakistanis make only around USD40 billion in exports,” he said. “Exports must meet our external sector requirement, which is a structural flaw as the country couldn’t achieve that.”

He stressed that political consistency is essential for growth, evident in all neighbouring countries. “Either we will crawl or leapfrog – we cannot afford to crawl now,” Iqbal said, adding that Pakistan receives only USD1.5 billion to USD2 billion in foreign direct investment due to a lack of policy continuity.

The minister noted that the country had suffered due to a lack of continuity in economic policies, emphasizing the need for consistency and a forward-looking approach to national development. “We must move forward with a positive mindset and ensure policy continuity to maintain economic progress,” he said.

Speaking on the occasion, FBR Chairman said the tax authority had eliminated the culture of favoritism within the institution and was working to improve governance and efficiency.

He explained that changes in the dollar exchange rate can affect sales tax collection levels, adding that a stronger exchange rate may result in lower sales tax receipts in certain sectors.

The FBR chairman stated that revenue collection stood at USD32.6 billion in June 2024 and increased to USD41.9 billion in June 2025. He added that revenue is expected to exceed USD46.4 billion by June 2026, indicating continued growth in tax receipts.

Langrial also praised Prime Minister Shehbaz Sharif and the government leadership for supporting reforms aimed at eliminating the culture of recommendations and undue influence within the FBR.

He said institutional reforms and improved governance measures have contributed to greater transparency and efficiency in the country’s tax administration system.

Retuers adds:Pakistan’s annual economic survey projected real GDP growth at 3.7% for the fiscal year ending June 2026, according to the report released on Thursday.

Here are some details from the report:

Average CPI inflation was seen at 6.7% in the July-May period, the survey said, adding that price stability was broadly preserved despite the Gulf conflict and its impact on energy prices.

The South Asian nation’s current account deficit was at $252 million in the July-April period.

Pakistan’s trade deficit from July to March stood at $23.53 billion, the document showed.

Fiscal deficit was at 0.7% of GDP in the July-March period, which the survey said was the strongest fiscal performance in decades.

The primary surplus was seen at 3.2% of GDP and public debt by the end of March was 83,285 billion rupees, the document showed.

Overall, fiscal performance remains encouraging, the survey said, supported by expenditure control, revenue mobilisation, provincial surpluses, and ongoing fiscal reforms.

KARACHI: The business community has termed the statistics of the Economic Survey 2025-26 as broadly encouraging, noting that the economy is on the right track. However, it stressed the need for deeper structural reforms and targeted policy measures to accelerate sustainable economic growth.

Commenting on the Economic Survey, Senior Vice President of the Federation of Pakistan Chambers of Commerce and Industry (FPCCI), Saquib Fayyaz Magoon, noted that Pakistan’s economy achieved a growth rate of 3.7 percent during this fiscal year compared to 2.8 percent in the previous year.

“This is a positive development, along with an increase in per capita income. However, it noted that the benefits of this growth and development have not yet been transferred to the masses.” He urged the formulation of policies that ensure the wider public becomes a direct beneficiary of economic growth.

He expressed optimism that Pakistan could achieve a GDP growth rate of 5 percent if the government continues to provide strong support to the industrial and export sectors. Magoon, who is also Chairman Businessman Panel Progressive (BMPP), said that the overall size of Pakistan’s economy has also reached historical level of USD 452 billion, which is a positive sign. However, despite being an agricultural country, the performance of the agriculture sector has remained not only below expectations, but alarming.

He stressed that the government needs to pay greater attention to the agriculture sector to unlock its full potential. Agricultural sector exports and value addition can help to reduce the trade deficit.

Khurram Ijaz Secretary General BMPP said that the economic indicators are encouraging. He described the increase in foreign exchange reserves to USD 18 billion as a positive development that would strengthen the country’s external sector and improve economic stability.

He said that Pakistan’s business community stands firmly with the government and supports its efforts toward economic stabilisation. However, he urged policymakers to seriously consider the practical proposals put forward by traders and industrialists during the budget-making process and present a budget that promotes investment, industrial growth, export expansion, and overall economic development.

Ijaz said that government should place special focus on the export sector and introduce policies that can significantly enhance exports. To effectively address such challenges of industrial growth, he said, the government must adopt a comprehensive and long-term economic strategy.

Shabbir Hassan Mansha Churra former vice president FPCCI also appreciated the economic performance and emphasised that the government must take effective and long-term measures to further accelerate economic growth.

He praised overseas Pakistanis for their contribution to the economy, stating that they have sent more than USD 38 billion in remittances during the first eleven months of the fiscal year, playing a vital role in strengthening the economy and improving the country’s external accounts. He described the increase in remittances as a highly positive development for Pakistan.

Mansha also welcomed the nearly 6 percent growth in Large-Scale Manufacturing (LSM), describing it as an encouraging sign. However, he said that this growth rate can be further improved through long-term industrial policies. He stressed the need to reduce electricity, gas, and other utility tariffs to enable Pakistani industries to compete effectively in international markets.

ISLAMABAD: The Economic Survey 2025-26 has warned that increasing demand, coupled with evolving climatic and hydrological conditions, is exerting significant pressure on Pakistan’s water resources, posing serious risks to economic growth and social wellbeing.

According to the survey (July–March FY2025-26), per capita annual water availability has declined to below 1,000 cubic meters, highlighting the urgent need for sustained and coordinated water resource management.

The report underscores that irrigation remains critical for enhancing agricultural productivity, ensuring food security, stabilizing farm incomes, and reducing vulnerability to monsoon variability and river flow fluctuations. Given agriculture’s key role in employment, rural livelihoods, and national output, the performance of the irrigation sector is vital for macroeconomic stability and long-term growth.

Pakistan receives, on average, 138.4 million acre-feet (MAF) of water annually from its western rivers—Indus, Jhelum, Chenab, and Kabul—and eastern rivers—Ravi and Sutlej. The Indus Basin Irrigation System (IBIS), ranked as the fourth largest contiguous irrigation network globally, forms the backbone of the country’s agricultural economy.

The system comprises three major reservoirs—Tarbela Dam, Mangla Dam, and Chashma Barrage—with a combined live storage capacity of about 13.44 MAF. It also includes 19 barrages, 12 link canals with a total capacity of 143,000 cusecs, an extensive network of main and branch canals, and two siphons. Spanning nearly 64,000 kilometers, the system irrigates approximately 47 million acres, supporting national food security and agricultural production.

Seasonal rainfall, including hill torrents and intense storm events, serves as an important supplementary water source. The survey notes that effective utilization through small dams, watershed management, and aquifer recharge can significantly enhance water availability and strengthen the resilience of rain-fed agriculture.

Groundwater remains another crucial source, contributing around 50 MAF annually, particularly in regions with limited surface water. However, its sustainability is becoming a major concern. In Sindh, aquifers are largely brackish, limiting their usability, while across the Indus Basin, groundwater extraction increasingly exceeds natural recharge rates. As a result, the aquifer system is now among the most stressed in the world.

The survey identifies multiple factors contributing to water stress, including limited storage capacity, transboundary water challenges, gaps in water accounting and allocation, conveyance losses, rapid population growth, climate change impacts, glacier melt, water pollution, rising urban demand, waterlogging and salinity, and financing constraints for major infrastructure projects.