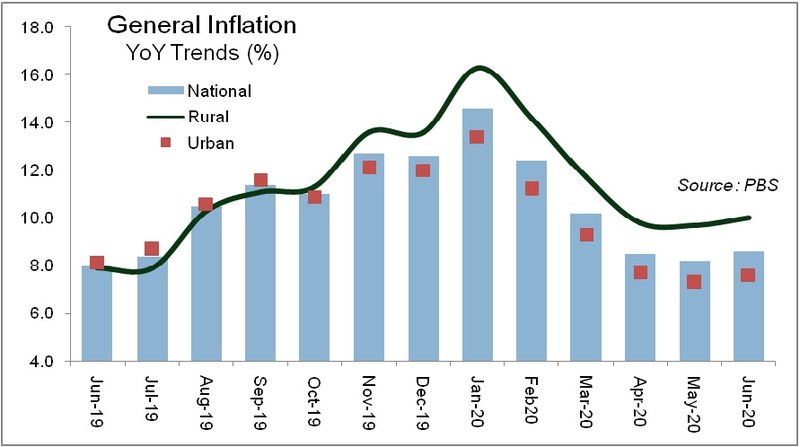

The inflation easing pace has eased out. Monetary policy gurus would be better advised to keep a close eye on monthly inflation and adopt a wait and watch strategy till September. CPI clocked at 8.6 percent in June, and FY20 headline inflation averaged at 10.74 percent - a little less than SBP’s earlier estimates of 11-12 percent. COVID surely eased some pressure on CPI. But now there are some signs of inflation resurgence. Although the base effect will keep the yearly inflation tamed in the next few months, higher monthly numbers is a point of concern.

In June, it is again the food inflation that is driving the headline. But there is a big difference from the pressures earlier this year. Back then, the perishable (such as tomatoes) and cyclical (such as broiler) prices were driving the food inflation high. Now it is wheat. The price impact of wheat is not going to be diluted that easily. This can push a pressure on inputs of milk and overall food supply chain. Milk is one fourth of food basket. Back in 2008, it all started with wheat that took food prices uptick to over 20 percent. On the mystery of wheat price increase – read “Wheat: from mishandling to the next crisis”

On monthly basis, CPI increased by 0.82 percent. Food group increased by 2.1 percent despite a decline of 2.3 percent in perishable food items. Non-perishable food prices increased by 2.88 percent – wheat and wheat flour in urban CPI increased by 10-12 percent in just a month. This is concerning. Wheat is a major input for livestock feed. While milk is the single biggest item in food inflation – if milk prices go up, the food CPI may well stay in double digits on yearly basis. In June, food inflation is up by 14.6 percent.

The impact of low petroleum prices (down by 7.3 percent on a monthly basis) is more than offset by increase in food prices. Not to mention, the low petroleum prices were not of much benefit to masses as supply was short most of the time. The so-called petrol bomb is to explode in July inflation. The prices of petrol and diesel are up by 25-35 percent and will ensure that the monthly inflation in July is north of 1 percent.

In July, the quarterly revision of house rent is due as well. That will add further to the CPI rise. The food inflation is not tamed as SPI data suggests further increase in food prices to be recorded in July. Thus, the inflation in July could be up in the range of 1.2-1.5 percent – on yearly basis, it will be around 8 percent. In view of this, there is little sense in any further monetary easing in July. But businessmen are confident that rates shall be reduced to 6 percent in July.

All these unknowns should keep hawks in control of the MPC. The inflation may hover over (or around) 7 percent till September. After that, the base effect will bring it lower; but by how much? There are some unknowns which must be considered by the monetary policy committee. What is the circular debt reduction plan? What will be the extent of increase in electricity tariffs? What will be the effect of any further increase in fuel prices? What will be the indirect impact of these on overall inflation? What will be pace of growth in money supply due to fiscal expansion? How shall increased demand for imports be affected by excessive monetary easing?

The June CPI has left some tough questions for the next monetary policy committee to mull over.

Comments

Comments are closed.