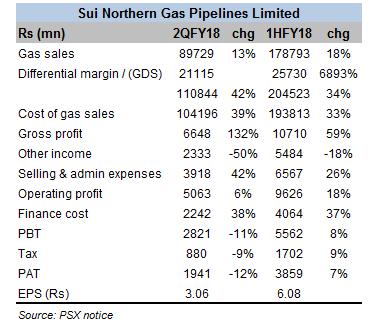

Pakistan’s largest state-owned gas company SNGPL sold more gas and earned more profits in the 1HFY18 over the same period last year. Rejoice if you are a shareholder. Or don’t, as the company stopped short of announcing the second interim dividend despite record high sales and a decent after-tax profit growth.

The mammoth increase in gross profit could not translate into a proportionate rise in bottom-line, as the drop in other income and rise in finance cost proved enough to trim pretax profits. Such is the nature of SNGPL’s returns that it can sway heavily on account of changes in such variables. But the elephant in the room is the differential margin, which may not be truly reflected in the profit and loss numbers.

The differential margin in the second quarter alone amounted to Rs21 billion, versus Rs4 billion in the previous quarter, and a Gas Development Surcharge (which is deducted from gas sales to arrive at net sales) of Rs1.6 billion. Gas prices in Pakistan have long been a dichotomy, and much has been written about the inefficient consumer pricing mechanism of natural gas.

The disparity between prescribed prices and consumer tariff is such that it creates huge receivables for SNGPL. The receivables on account of differential margin had soared to Rs70.4 billion by the end of September 2018. The last quarter saw higher sales and a massive credit on account of differential margin, which suggests these receivables would not stand north of Rs80 billion. The pace of growth in differential receivables has hastened over the past few quarters.

The settlement of this outstanding amount hugely depends on increase in gas prices. With the general elections around the corner, there are no marks for guessing that government is less likely to tinker with consumer gas tariffs. The differential receivables alone are responsible for below par cash flow from operations. And the pace at which it is growing is soon going to start reflecting in profit and loss account.

What options is the government left with? Well, not many. Continuing to deprive SNGPL of payments is going to create more trouble in the entire energy chain, as already evident from high payables at SNGPL’s end. To continue subsidizing SNGPL at the cost of other paying customers to a few already paying much lower rates, would certainly be a disservice to taxpayers ‘money.

The only way is to increase prices. Do it in phases, if you do not have the political will to increase rates at once. With more LNG coming in the system – the differential is only going to increase. The average price has to be increase in order to avoid more trouble, if current situation is not already alarming enough.

And we have not even talked about the infamous UFG losses. SNGPL is reported to have recorded UFG losses in excess of 10 percent during 1HFY18. This is well over the Ogra’s allowance of 6.3 percent and a vital reason why SNGPL faces such profitability pressures. Mind you, 6.3 percent UFG allowance is already considered to be on the higher side, whereas the company had demanded to be allowed UFG at 9 percent. Surely, the consumers must not be burdened to pay for sheer inefficiencies of a company.

Comments

Comments are closed.