Pakistan’s power generation crossed 14000 GwH in August 2018. This was the highest ever electricity generation in the country’s history. The dependable capacity has now crossed 31000 MW, 25 percent up from last year. The power generation, though, has increased by 10 percent in the same period. This shows how all capacity addition does not necessarily translate into generation of the same magnitude.

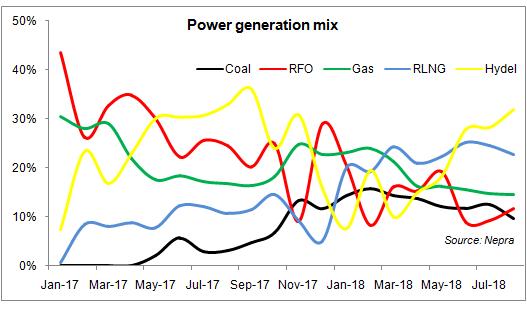

The real story, however, remains the continued improvement in power generation mix. Luckily, the contribution from hydel generation has increased, and is back to the old-days share of one-third in total generation. The hydel power generation in absolute terms over 4400 GwH is also the highest ever.

The FO based power generation continues to decline, having halved to 12 percent from last year. Even when the water levels went down in the last few months, improved availability of RLNG based plants ensured that the FO power generation did not reach alarmingly high levels.

The growth story of the dependable capacity may soon come to a halt – the signs of which are already here, looking at the import number from the last few months. Pakistan seems to have entered the consolidation phased, having added over 11000 MW in the last four years. It is now a matter of keeping the plants available at full steam, and ensuring smooth supply of requisite fuel sources. In the months to come, expect the share of LNG based generation to go up from the existing 24 percent – as a couple of sizeable RLNG plants are expected to be running at full throttle.

Having made energy available, it is now time to look at the other and equally more important part of the equation, energy affordability. The average fuel cost has gone up by 14 percent from last year, and the total fuel component bill for August 2018 was 35 percent higher year-on-year, with 10 percent more generation.

With revised gas prices for power producers, expect the fuel price component in the power tariffs to go further north. Power plants will now be paying 40 percent additional for natural gas, and if the share of gas based power generation stays around 15 percent – this alone will account for 6 percent increased in the fuel price component. Oil prices have also stayed north of late, and this will add more to the fuel cost – meaning more rounds of monthly adjustment to the fuel component of the tariff in the months to come.

The ECC is also expected to raise the base power tariff by another Rs2/unit. Truth be told, this is long due. But when the cornerstone of the energy policy has been providing affordable energy, this may not continue forever. One would argue that with a much improved fuel mix – the tariffs should rather come down. But the health of affairs in the power sector dictates that tariff rationalization is a must.

All the megawatts in the system have not come without a cost – that of capacity payments. Meanwhile, the average fuel cost of various fuel types has also gone significantly higher in the last 12 months – making matters more difficult. It is time to strengthen the reliability aspect of the overall chain – both financial and physical – so as to minimize the impact of oil price increase to the overall tariff.

The tariff increase may well be much needed right now and will fall under the ‘stabilization’ mode of affairs. But ‘reforms’ have to start now.

Comments

Comments are closed for this article.