Currency depreciation has wreaked havoc on Shell Pakistan’s financial performance in the last two years. The oil marketing company announced its financial performance for CY18 last week with earning tainted by staggering exchange losses. The same had dragged earnings in CY17

Along with exacerbated exchange losses, the company continues to face the threat of rising receivables, the effects of which can be seen in 260 percent year-on-year increase in other expenses in CY18. Back in CY17, these expenses grew by 140 percent year-on-year.

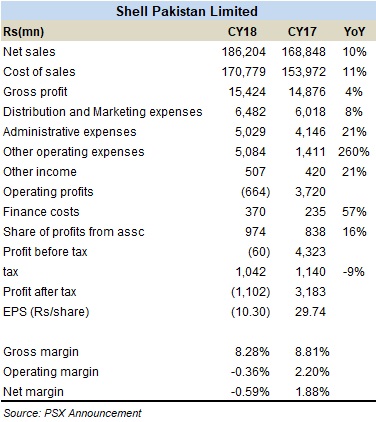

Hence, despite the revenue growth 10 percent year-on-year, and slight improvement in gross margins, Shell Pakistan ended up with a loss of over Rs1 billion in CY18 versus a profit of Rs3.2 billion in CY17. A 57 percent year-on-year growth in finance cost added to the earning squeeze.

However, in terms of operations, CY18 turned out to be a better year for Shell Pakistan. Back in CY17, the OMC also faced dwindling market share amid sluggish performance of the oil marketing sector. In CY18, the company had been making efforts to regain the lost market share as well as increase its retail presence. With recovery in retail volumetric growth, Shell Pakistan’s overall market share for the recent six months from July to December 2018 (1HFY19) stood at around 8 percent, versus 6 percent in similar period last year. Its market shares for the retail fuels like HSD and MS stood at 7 and12 percent, respectively for recent six-month period. The company is also part of the consortium that is planning to the third LNG terminal with 600 mmcfd expected to come online by mid-2020.

Currency depreciation along with the burden of receivables is the biggest threat the company faces; it had also approached the government to allow the downstream industry to secure profit margins in dollar because of the significant exposure of forex affecting earning. Whether that’s workable or not will be picked up by this space later.

Comments

Comments are closed for this article.