Unsustainable fiscal framework: something’s got to give!

The controversy surrounding NFC award has picked up steam. Beyond the centralist versus federalist debate, some hard facts are presented here, as numbers do not lie. And the tale they tell is that current federal fiscal framework has become unsustainable. Something has got to give, if the federal government is to be saved from default.

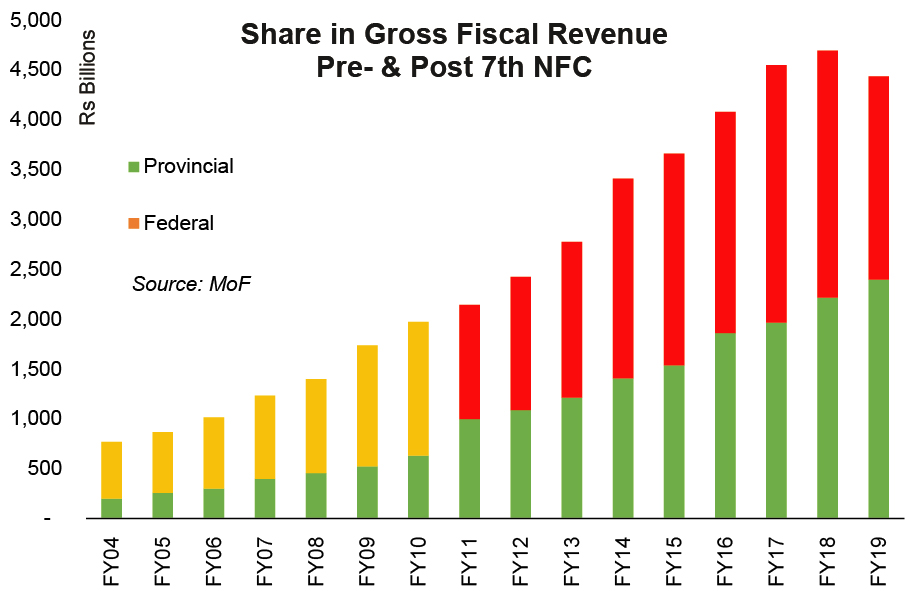

Half cooked NFC award has long lasting fiscal implications, evidenced by the state of fiscal operations at the center that have begun to unravel in recent years. In FY19, debt servicing expenditure exceeded federal’s share in gross fiscal revenues. This means that all other expenses were financed by new debt generation. The accompanying illustrations show various expenditures as percentage of net federal revenues (after deducting provincial share) to depict how the picture has changed post 7th NFC.

For instance, debt servicing to net fiscal revenue ratio was 31 percent pre-7th NFC (average: FY04-10) and that has increased to 65 percent thereafter (average: FY11-19). Increasingly, this is leaving little space for other expenditures. While the debt is growing out of proportion.

The federal government is pushed to raise revenues but only for servicing debt, defence expenditure and pension. Defence spending (on average) was 31 percent of federal revenue share prior to NFC and this has increased to 38 percent thereafter. The ratio was 56 percent in FY19, and every paisa of it was paid through incremental debt.

The story of defence expenditure does not end here. Pension liabilities of retired military officers and rankers are growing at a brisk pace. For instance, government paid Rs253 billion on military pension in FY18. This was higher than other government general expenditure (read federal government employees’ salary bill). Yes, the government is spending more on military personnel pension than the (fat) salaries of all federal government employees. Pension liabilities is a headache. It is unfunded and some estimates suggest that will become 50 percent of federal expenditure in a decade or so. Three fourths of the federal pension expenditure go towards military pensions.

Development spending is growing in proportion to fiscal revenues; but that may not continue for long. It is up from 27 percent of net revenues (pre 7th NFC) to 36 percent (Post 7th NFC). However, that is bound to be compromised in years to come. Federal government should leave the development for provinces which receive lion’s share of gross fiscal revenues.

The argument federalists present is to increase revenues and reduce the fat of the federal government. However, numbers tell there is relatively less fat in federal government service expenditure (barring defence). Centralists say that there should be some mechanism of getting part of revenues back from provinces (not possible under current constitutional arrangement). Even if some formula is devised for emergency purposes, provinces may slack from their much-needed responsibilities.

Federalists have solid reasons to safeguard provincial share. Education, health, policing, clean water and air provision, are all provincial subjects. And the country is significantly lagging in delivering on these developmental goals. Almost half of the kids in Pakistan are out of school. Health indicators are no better. Environmental degradation is a well-known fact. Provinces need to spend more. But they must do it judicially.

For example, under the last regime almost half of Punjab’s developmental budget was spent on projects in Lahore alone. In Sindh, PPP (ruling party for past 12 years) does not have any constituency in Karachi and the spending is miserably low in the city of (so called) lights. Fiscal devolution has not been taken to its logical next step through provincial finance commissions (PFCs), as no progress has been made on same. The essence of fiscal federalism is having a strong center while the power of spending must devolve to the third tier. In Pakistan, provincial governments have become too strong.

The other argument federalists’ present is of jacking up federal revenues. Yes, government must push a bit. Gross fiscal revenues were 12.8 percent of GDP (average FY04-10) and that has marginally increased to 13 percent of GDP after the 7th NFC award. Tax revenue has increased marginally from 9.5 percent to 10.4 percent. Then there is below the line deficit, such as the infamous energy circular debt. The toll is approaching Rs2 trillion and is the one of the biggest fiscal headaches today.

Back in 2017, IMF sat down with provinces and attempted to come up with a resolution of this peculiar fiscal arrangement. As per the constitution, debt and electricity is a joint responsibility of federal and provinces. The responsibility must be shared or else the default on debt is inevitable.

Some say that most of the debt (and its servicing) is domestic and a government cannot default on domestic debt when it can print currency. Yes, it is. But this can result in hyper-inflation. There are precedents in the world (more on this later).

Domestic debt will continue to accumulate, diminishing the real value of existing debt. The time value of money matters. Debt is issued at today’s rate (linked to current inflation), and at maturity the inflation could be much higher. For example, if one buys a 10-year defence saving certificate of Rs1 million today, he shall receive Rs3 million after 10 years at an assumed rate of 12 percent. Today, a small car costs Rs1 million, but in 10 years it may only be enough to buy a motorcycle. This scary hypothetical example could well be real if ‘business as usual’ continues.

Comments

Comments are closed.