Gharibwal sliding in losses

(PSX: GWCL) is a smaller cement manufacturer; and much like other small and big players in the arena (Cherat and DG Khan Cement for instance) incurred a loss in the first half of the fiscal year. Domestic demand is down, retention prices are more competitive, and costs are up.

Gharibwal’s factory is located in Punjab near the Jhelum river and supplies mainly to markets in the north of the country. This is where competition has grown as more companies have expanded capacity and demand has remained lethargic. Bigger companies have had a better chance at growing their market share then smaller companies.

As a result, prices fetched by cement in the domestic market have been under pressure. Previously, Gharibwal was also exporting to India, but since countervailing duties hit Pakistani cement, that market has also closed doors.

However, the company was never truly export-dependent. In FY18 and FY19, its revenues from exports were less than 1 percent (<2 percent during FY17 and FY16). Since it is operating on a smaller capacity, it supplies mostly domestically and has to deal with the concentration risk associated to it.

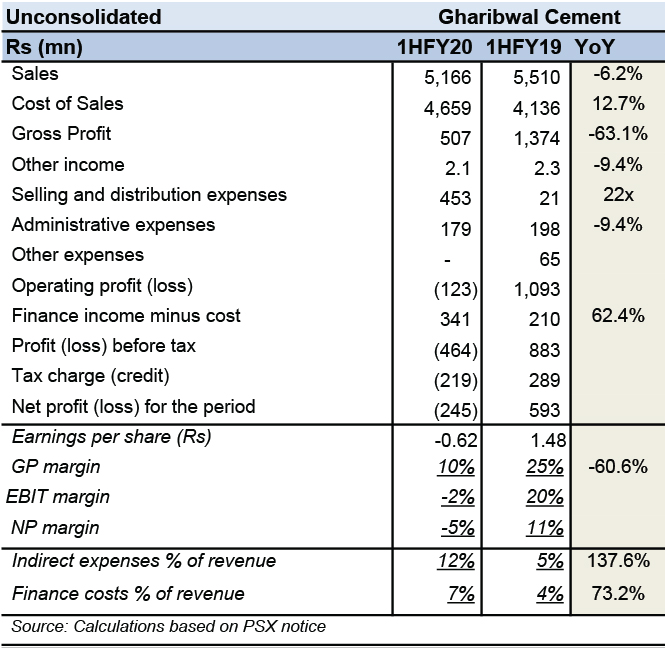

Though coal prices in the foreign markets have been heading south (average coal price were down 32 percent during the Jul-Dec 2019 period against the corresponding period last year) — which cement companies should have leveraged by managing inventory effectively and procuring fuel accordingly —Gharibwal’s margins have fallen to 10 percent (from 25 percent last year).

Low prices are certainly a factor. In the first quarter, revenue per ton sold came down 14 percent. Cost of goods sold per ton meanwhile rose 11 percent. Electricity prices and increase in royalty on the raw material — limestone and clay — (up 160 percent) were also dominant factors.

The company was unable to keep overheads in check. These stood at 12 percent of revenues in 1HFY20, against only 5 percent which is typically an average for cement companies. Higher distribution costs points toward higher transportation costs. Tighter monetary policy has also resulted in higher financial costs for working capital needs, rising from 4 percent to 7 percent of the revenues. The company is spending a lot more than it is bringing in.

Prices in the north market will remain under pressure as new capacities come online and demand remains subdued. This is not a good time for cement firms, particularly the smaller ones.

Comments

Comments are closed.