The fear of the domestic economic players is that interest rates are kept high to attract the foreign investment in the government papers and that is going to hamper domestic demand and adversely impact the borrowing capabilities of the private sector. The argument is slightly misplaced on two counts – one that Pakistan’s private sector is not highly leveraged to have systematic slowdown due to high rates, and the other is that the market based rates are already falling owing to high demand of government papers due to foreign funds participation amid expectations of interest rates to come down.

The fear of the domestic economic players is that interest rates are kept high to attract the foreign investment in the government papers and that is going to hamper domestic demand and adversely impact the borrowing capabilities of the private sector. The argument is slightly misplaced on two counts – one that Pakistan’s private sector is not highly leveraged to have systematic slowdown due to high rates, and the other is that the market based rates are already falling owing to high demand of government papers due to foreign funds participation amid expectations of interest rates to come down.

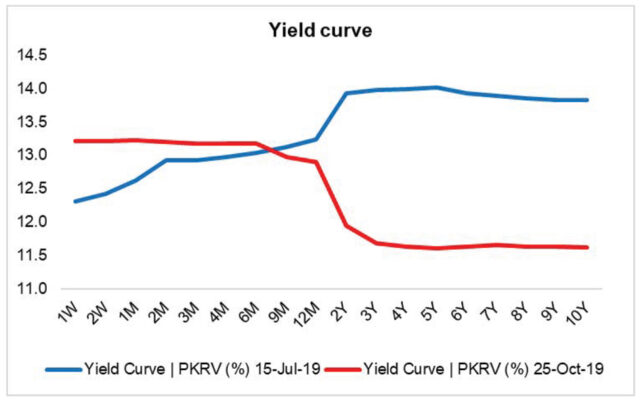

The policy rate was last increased by 100 bps to 13.25 percent in Jul-19 and the discount rate reached 13.75 percent. The 10 year PIBs secondary market yield peaked at 13.9 percent in May-19 and is now down to 11.25 percent in last week before slightly moving up to 11.62 on Friday. In case of 6-month paper – the yield fell from 13.94 percent to 13.18 percent. The government borrowing cost, on incremental basis, is already reduced. The story of KIBOR is no different – rates are coming down and the private sector borrowing cost is to reduce accordingly.

Now the discount rate at 13.75 percent is irrelevant as long as borrowing is concerned; but deposits holder in PLS saving accounts, linked to discount rate, will keep on getting better returns till the policy rate is reduced. Thus the pronounced reason for keeping real interest rates positive to lure savings is still applicable, but borrowing cost is reducing. Similarly, the NSS rates, till these are revised down to adjust to latest PIB yields, are offering mouthwatering returns. The lag of NSS rates peg to PIBs is providing an arbitrage opportunity, as some institutions and all individuals, can invest in these, and this may cause an unnecessary cost to fiscal kitty, and creating an unnecessary distortion. This requires some correction.

Anyhow, the market has already priced in easing monetary policy. However, SBP may not decline rates till Mar-20, as reducing in Nov-19 may show that 100 bps increase in Jul-19 was not called for. According to minutes of monetary policy for Sep-19, for the first time in many reviews, one of the MPC member voted for 25 bps cut while remaining 8 were for no change. This time there will be higher votes for rate cut.

The inflation in Oct-19 is to stand around 10-10.25 percent before increasing to over 11 percent in Nov-Jan, and may start coming back to single digit thereafter. Thus, rate cut is surely on cards by Mar-20. SBP has two option either to go for small successive cuts in Nov-19, Jan-20 and Mar-20 or to go for around 100 bps cut in Mar-20. The chances of second options are high. Anyhow, the short term high rates did not matter much and the issue was hyped. The foreign portfolio investment has to come at market rates. Last week $88 million further came in T-bills to take the year to date flows to $440 million.

The story of stabilization of macros is helping market rates to come down. The currency also appreciated by 5 percent in the past 3 months and that also shows that too high adjustment in Jul-19 was not called for. However, it is now market based, and the market is calling that both monetary and exchange rate tightening was higher than expected. The other angle to look at it is that sudden acceleration of tightening in Jul-19, kicked the speculator out of the equation. The people earlier were accumulating foreign currency and thy are now putting the money in rupees to maximize the benefit of short window of too high rates.

Comments

Comments are closed.