The Finance and energy ministries ought to have the realization that without fixing energy prices the circular debt issue cannot be resolved. In simple words, circular debt is nothing but the difference between cost and sale price (tariffs), and the anomalies have to be sorted out before it is too late.

Earlier, the circular debt origin was only power sector, with the inclusion of RLNG in the gas system, the gas circular debt is another headache for economic managers. On top of that, the government is busy handling thefts - which is important, but should not be the priority, -it is penny wise but pound foolish.

The government has apparently not understood the issue right, and the problem was even worse in the previous regime. In most cases, demand is ascertained based on subsidized prices and import decisions are made accordingly; but when the subsidies are removed, demand tanks and the circular debt building accelerates as most supply - be it power or imported gas, has guaranteed return irrespective of the consumption.

Gas is a new headache and the problem is the inadequate tariff rationalization. The model of cross subsidy has to be designed with care and it should be equitable across the board. All the variables in energy chain have to be kept in mind is designing policies and setting tariffs. When the decisions are taken in isolation, it becomes more problematic.

There are many such anomalies- the difference between lowest and the highest slab of domestic consumers is 12 times. Yes, it is the right approach to charge higher price for rich consumers (assumption is that rich consumes more units), but the gap has to be realistic. The government has faced the embarrassment on recent gas pricing where the bill amount more than doubled or tripled on a difference of one unit. The pricing formula was approved by the ECC and now the buck of wrath is being swiftly passed on.

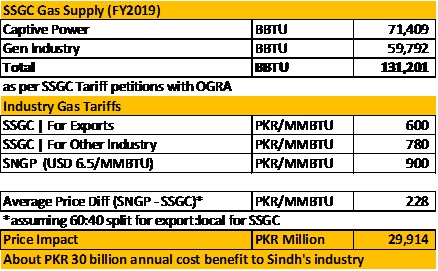

Similarly, there are irrational tariffs on industrial sector. For example, the gas tariff for Punjab exporters is $6.5/MMBTU or Rs900/unit. At this price, the Punjab industry is happy and eyeing expansion. The gas provided for Punjab exporters is mainly RLNG and is subsidized for exporters to make them regionally competitive. In case of industry in Sindh, the rates are even more lucrative -fixed at Rs780/unit for other industries and Rs600/unit for exporters. Since domestically produced gas is a provincial subject, the industries in Sindh are getting gas at better rate. But the question is why Sindh exporters are given the additional benefit as even at Rs780/unit their rates are lower than Punjab. Someone has to pay the subsidy and this will build circular debt further.

The government should put the foot down and have minimum price of Rs900 per unit for any industry anywhere in the country. The difference between Punjab exporters and Sindh industrial gas price comes at Rs30 billion, based on total SSGC gas supply, assuming 60:40 split for exporters and local, within SSGC industrial consumption. This Rs30 billion adds to circular debt.

The other problem of subsidizing gas for industry is to incentivize them to use captive power generation at the expense of grid consumption. The capacity charge has to be paid to all the new IPPs irrespective of the electricity consumption - according to NEPRA, annual capacity invoice is increasing from Rs275 billion in FY16 to around Rs490 billion in FY18 and is expected at Rs664 billion in FY19.

The capacity charge per unit in FY16 was Rs3.4/unit, and Rs4.1/unit in FY17. In order to keep it at level of FY16 in FY19, the energy consumption in FY19 has to increase by 57 percent, but that is not happening, and per unit capacity charge would be over Rs5/unit. Without passing the differential to consumer, it is adding to circular debt. The government has to incentivize higher consumption on grid to dilute the capacity charge, but it is instead making captive generation viable.

Apart from this, there is Rs3/KWh subsidy on electricity for domestic industrial consumers. It makes sense to give subsidy to exporters, but why a subsidy to domestic industries as the buildup of circular debt due to it has to be paid by all. In 2018, 27.5 billion units of electricity were consumed by industry and out of which conservatively 20 billion units were consumed by domestic industry, as exporters are mainly using gas, the annual subsidy of domestic consumer is around Rs60 billion - adding to the circular debt.

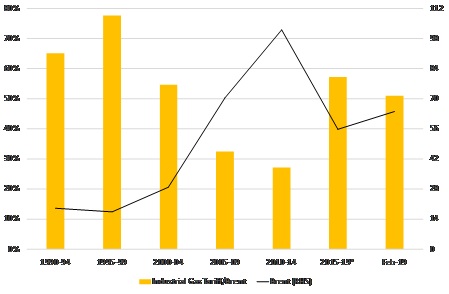

The lessons to learn is to rationalize the tariffs by not subsidizing industry too much as eventually consumers have to pay the price. The other problem is that the domestic energy markets never fully adjusted to the “High Oil Price Paradigm” which dawned in the early-2000s. During the 1990s, industrial gas tariff averaged over 70% of Brent price (in energy value terms). Even after the latest gas price hike, the current (Feb-19) natural gas tariff is only 51% of Brent.

In 90s the Brent average price was below $20 per barrel and that has increased significantly since then, but our energy tariffs never rationalized in accordance, and this largely explains the buildup of around Rs1.5 trillion stock of circular debt.

The economy cannot take any further fiscal shock of irrational energy prices, the government and opposition has to stop this social media war of passing the blame on each other. It’s a national issue and there should be a consensus of taking the bitter pill of revising energy prices up, and more importantly to plug in the anomalies.

Comments

Comments are closed for this article.