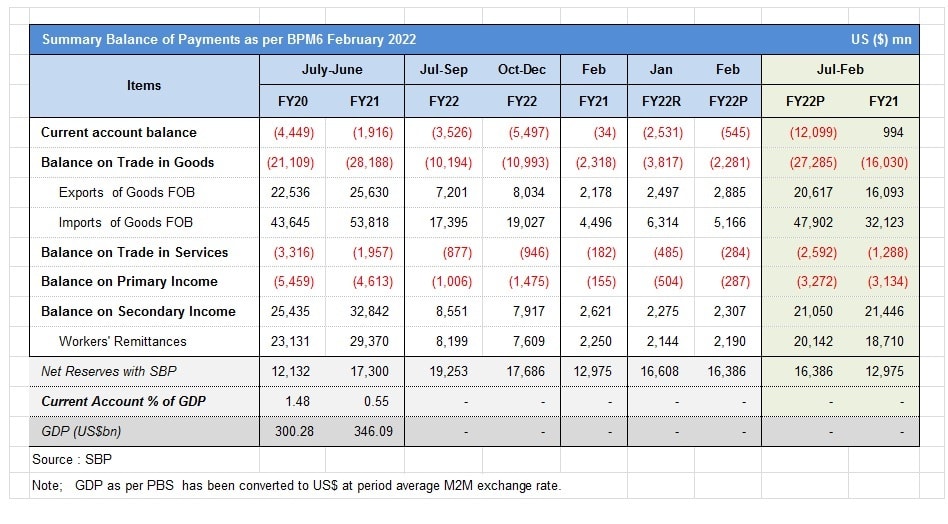

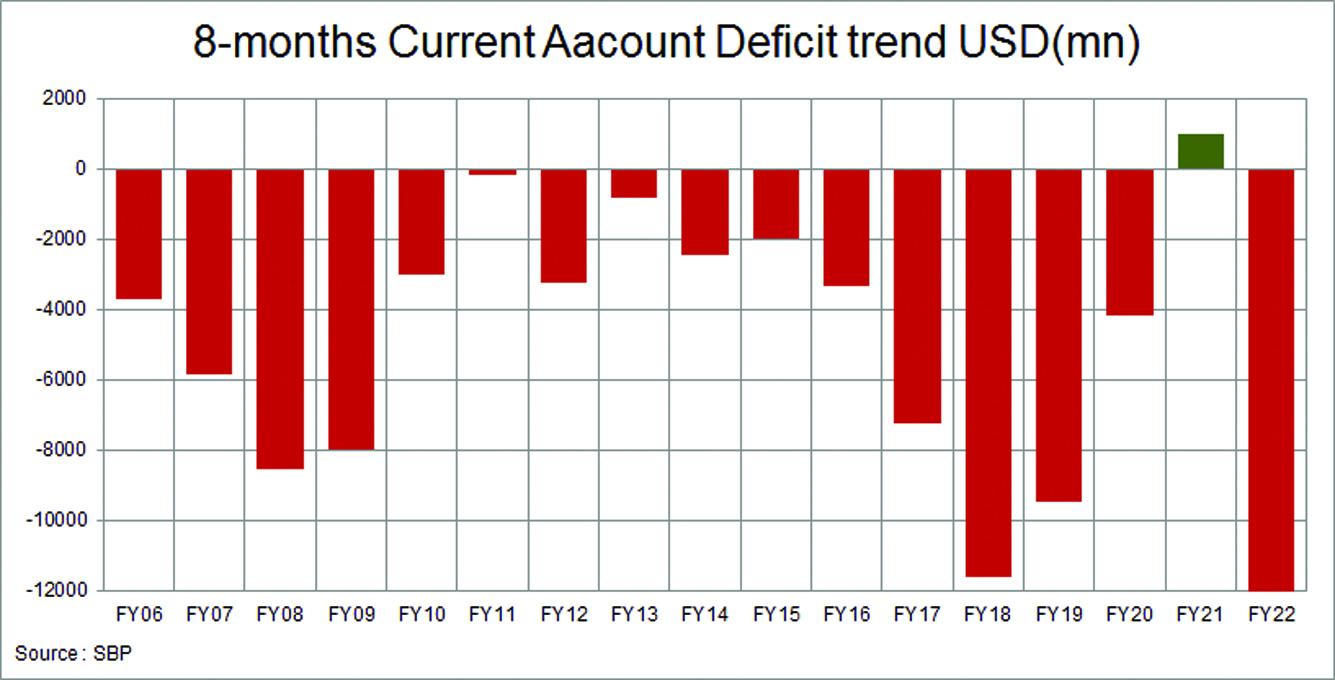

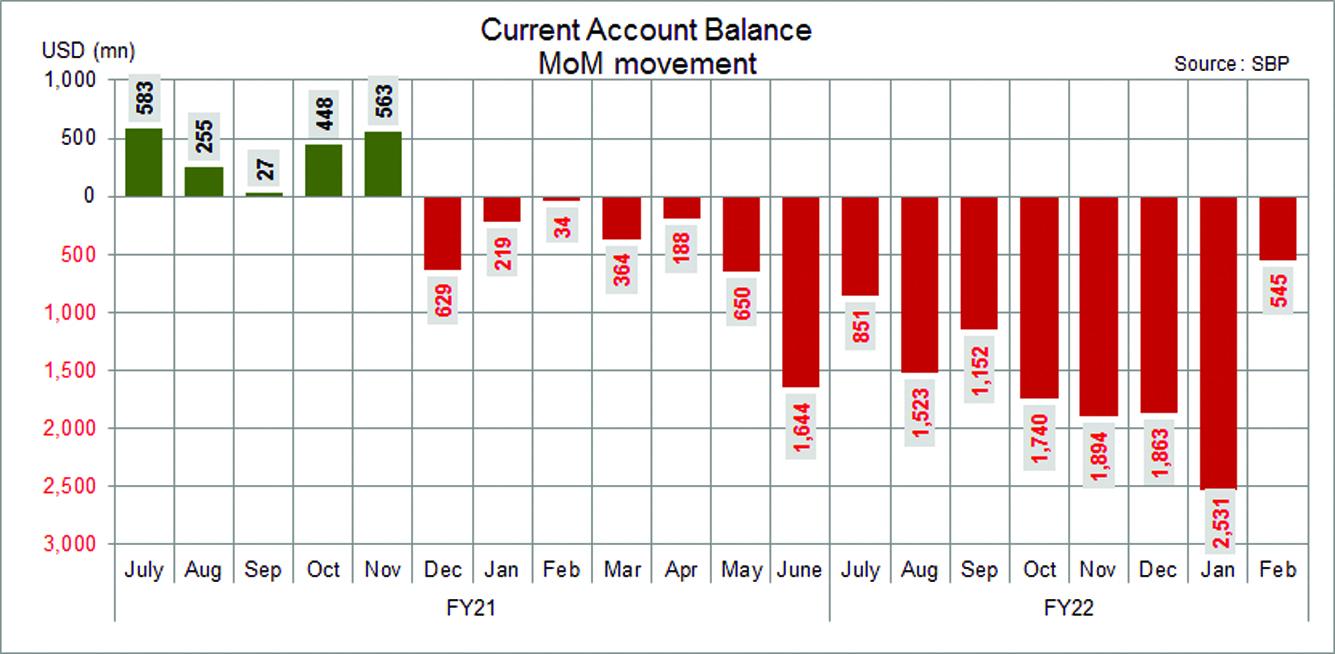

Current Account Deficit (CAD) stood at $0.5 billion in Feb-22 as against $2.5 billion in the previous month – a rare, good news in days of political mayhem where economic decision making is becoming a casualty. The deficit came under control due to fall in the imports while exports growth remains resilient. The CAD toll is at $12.1 billion in 8MFY22 which is in sharp contrast to a surplus of $1 billion in the same period last year – the CAD in 8MFY22 is the highest absolute number for 8-month period ever.

Having said that, it’s not just the higher economic demand that is triggering imports growth the prime reason for higher deficit is COVID and commodity super-cycle in the aftermath of COVID. Pakistan bought 257 million doses (price is approx. $2.5-3 billion) of vaccines in Jul-Feb period. Then virtually all commodity prices are peaking at the same time due to supply disruption followed by sudden jump in demand. Usually, different commodities have different peaking cycle – this super-cycle is unusual. And there is no end to it, thanks to Russia-Ukraine war as both countries are big global supplier of various commodities. Then in the past few months there were some mysterious items imported as well – most probably for defense purposes.

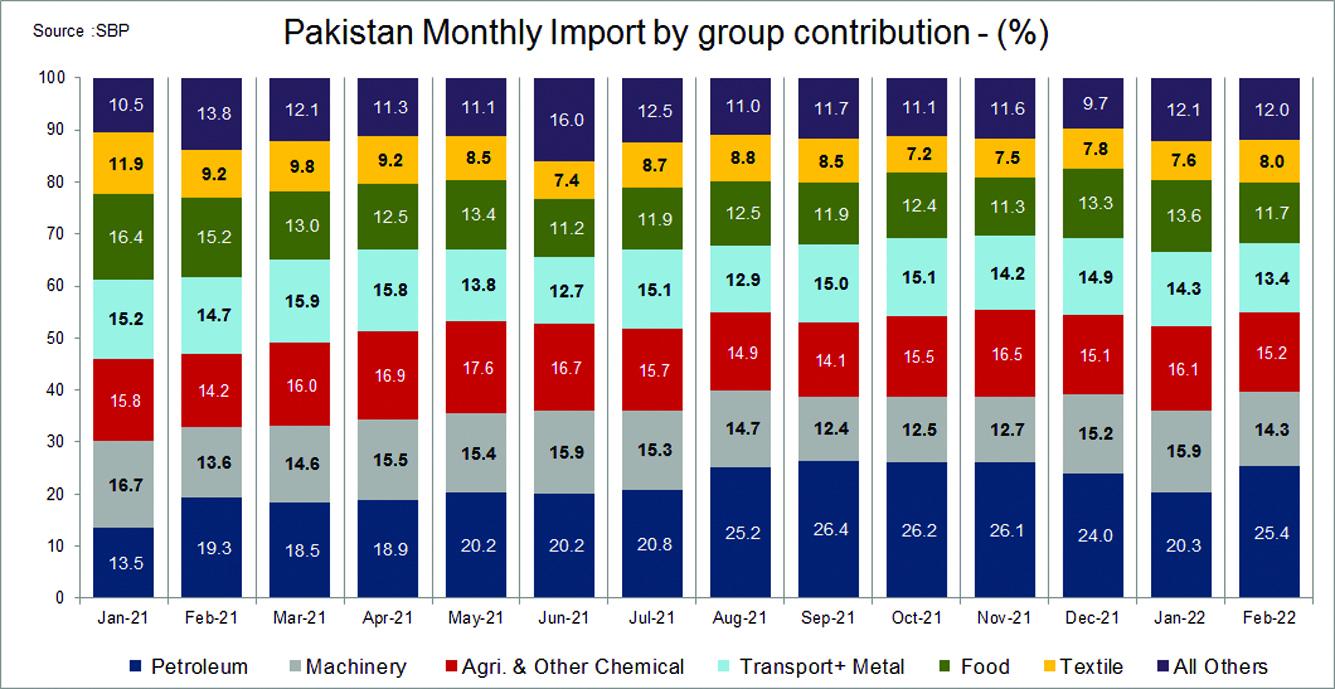

The imports are now likely to normalize, as COVID-related vaccines and other unusual items are seemingly out of the way. Now the only concern is higher commodity prices due to war implications. SBP imports fell by 20 percent or by $1.2 billion in Feb-22 (as compared to Jan-22) to stand at $5.2 billion. Majority of the difference is in imports through non-banks ($933 mn) as majority of COVID and unexplained items are routed through non-banking channels. And since these don’t fall under the ambit of interbank (and are fully financed), there is no impact on currency demand and supply, and hence no effect on the PKR/USD movement. That is why the currency kept depreciating despite the decline in imports in Feb-22.

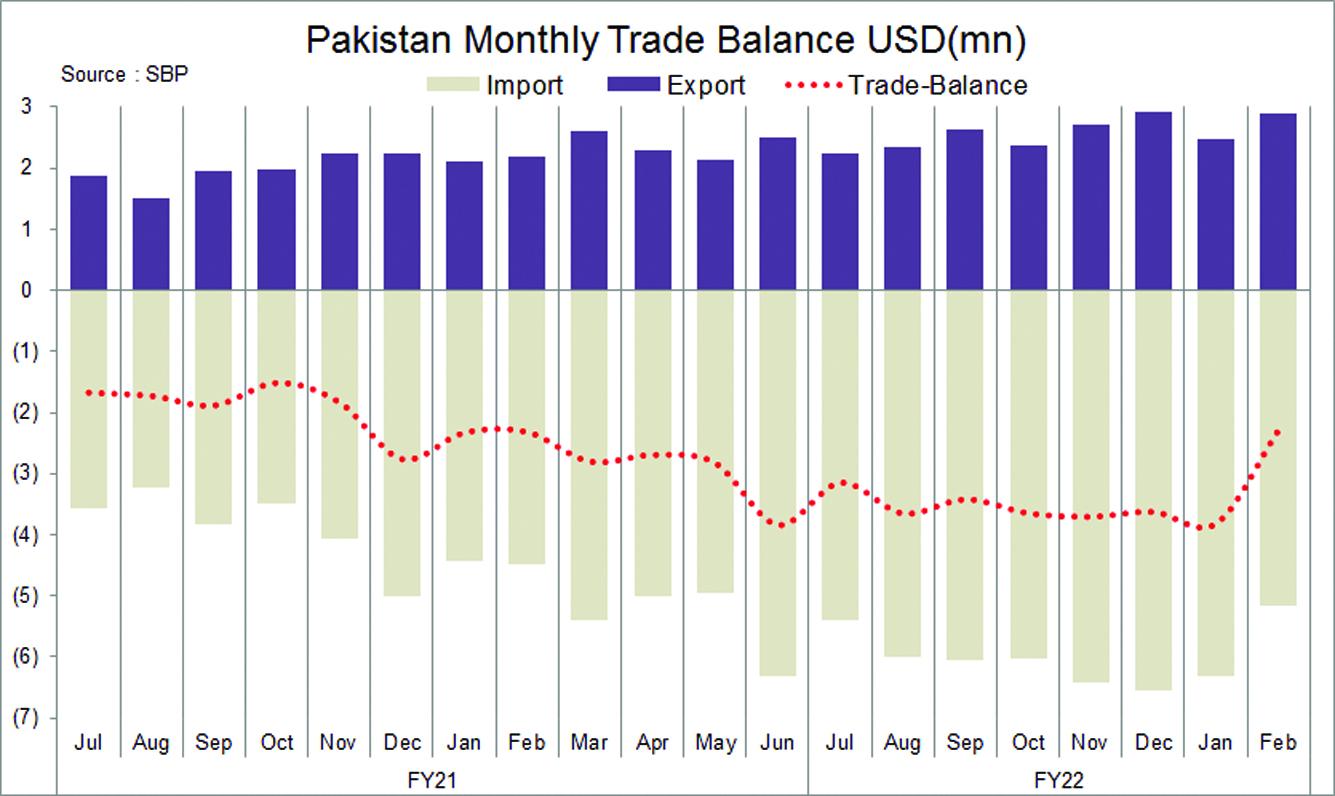

The import bill at $5.2 billion in Feb-22 is the lowest number since May-21. The import bill between June’21 - Jan’22 averaged at $6.1 billion. It is not just vaccines and defence imports that triggered the higher bill. There are elements of demand in it too. The currency appreciated to low 150s in May-21 and the interest rates were as low as 7 percent. Then the fiscal budget of FY22 brought loot-sale with it. Seeing the slippage in the current account deficit, the interest rates moved up (through SBP policy and market own response) and the PKR/USD is now touching 180 mark.

This is now having an impact on demand. There is a decline in imports across various sectors. The fall is slow; and this may continue, as market rates have moved up and the currency is depreciating as well. The only concern is fiscal response of freezing the petroleum and electricity prices and seeing that the currency depreciated further as a first line of defence.

The good news is that the exports are resilient despite the fear that due to low provisioning of gas in Dec-2, exports in Feb and March 2022 may remain low. The Feb-22 toll stood at $2.9 billion – almost the highest ever number. The Jul-Feb exports are at $20.7 billion and at this run rate goods exports shall reach $31 billion in the full year. Sources close to government claim that the daily run rate on PBS is around $100 million a day and that could take the monthly exports to $3 billion.

There are number of factors contributing to higher exports including higher per unit value due rising in the commodity prices. Some argue that growth is due to currency depreciation and other government’s export promoting policies while other negates that. The fact of the matter is that there is visible (if not massive) expansion in the exporting sectors – especially textile’s manufacturing capacity. Since the players now have the capacity, they are finding market to do so. Even if the demand from west slows down or energy prices to exporters is not provided at regional competitive rates. Pakistan’s market share is too small as any global demand dent would have a limited impact. And in case of higher input cost or unfavorable move in currency, only net margins could hurt. The exporters would do what they can to produce and exports.

The government/SBP should get credit for luring the exporters to expand by giving them flexible exchange rate, providing them regional competitive energy, and by generously providing they subsidized long term credit to expand and short credit to fund working capital. Exporters are lobbying for better pricing to fatten their margins and they would keep on doing so. However, despite that they would keep on exporting higher volumes. They may not expand any further for the time being especially if the government changes and Dar-nomics return to action.

Textile exports shall touch $18 billion this year at the current run rate. The number moved up from $5 billion to $10 in Musharraf time. And that remained stagnant around $12 billion for good ten years (barring one or two years of higher commodity prices). Now it has moved up from $12 to be $18 billion in 4 years.

In FY22, both exports and imports are all time high. These are healthy indicators, as the problem of Pakistan is not high imports but low exports and till the time exports/remittances move up, the only viable option to curtail deficits is to curb imports. Nonetheless, higher trade volumes mean higher economic activities and higher employment.

And the growth is not limited to manufacturing sector. The services exports are now becoming a charm. That is the only hope for the future. ICT exports were $1 billion in FY18 and based on 8MFY22 numbers ($1.7 bn) the toll shall reach $2.5 billion in FY22. All these are health indicators.

Nonetheless, the issue of growing trade deficit (goods and services) which has worsened by 73 percent in 8MFY22 to $30 billion in 8MFY22. Remittances are resilient - up by 8 percent (on a higher base) to $20.1 billion in 8MFY22. There are signs of remittances tapering off in the ongoing quarter, as with travel opening, some volumes are perhaps moving back towards hundi hawala and that is also contributing to some decline in imports as well – as remittances through gray channel must net off with something.

Going forward, the challenge is to keep growth in remittances intact, slowdown in imports and keeping growth momentum in exports. The run rate of imports and exports in the first two weeks of March is encouraging and it seems the PBS trade deficit shall be lower in March. Let’s see how long this momentum continues – key risks are global commodity prices and domestic politics – both remain highly fluid.

Comments

Comments are closed.