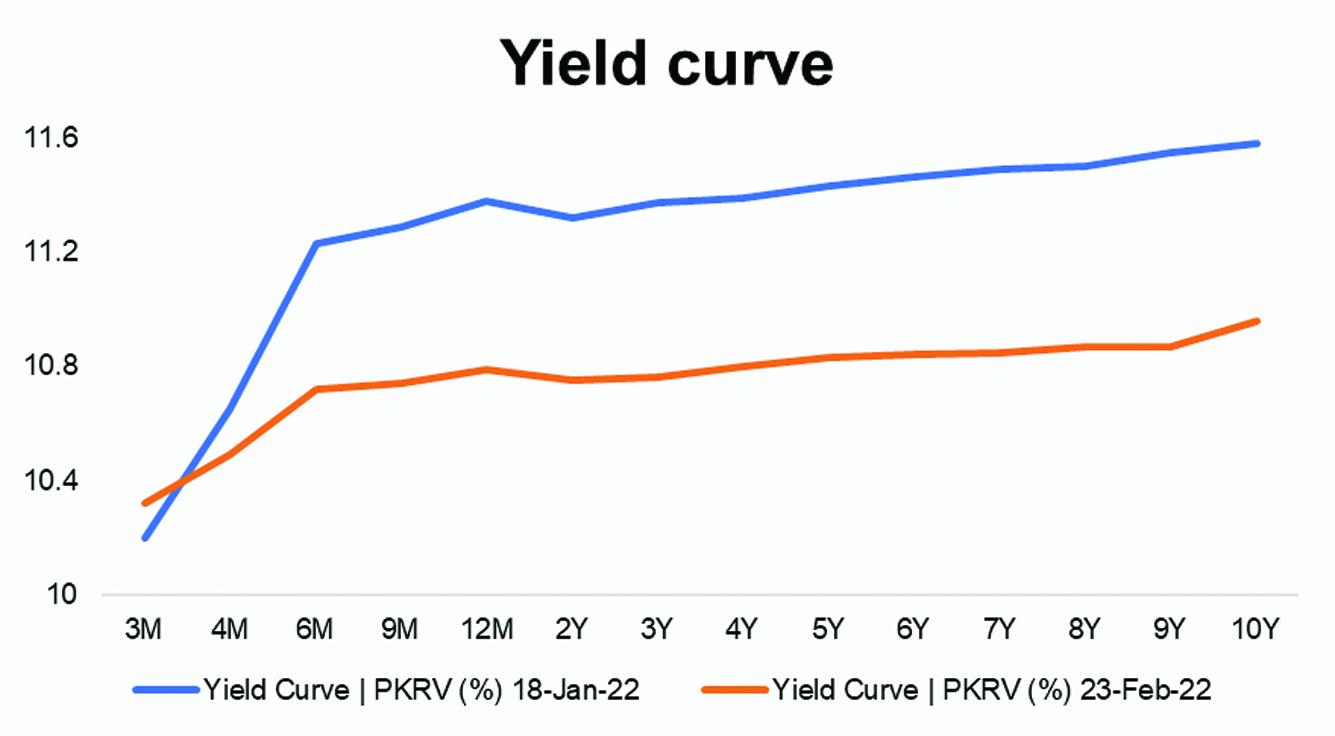

The cat and mouse game is back. With commodities prices touching new highs, increasing quantum of open market operation (OMO) injection, and higher auction targets, the market is demanding higher rates in T-Bills. In this week’s auction, the cut-off yields are up by 12-23 basis points (bps), and the government could only fetch Rs367 billion against the target of Rs800 billion.

The participation was not high – at Rs732 billion (as compared to Rs1,040 billion in the previous auction). This could be due to wait and see approach till the next monetary policy (due a day before the next auction) and low participation in the aftermath of CCP (Competition Commission of Pakistan) intrusion. Whatever the case, since maturities are piling up and oil is crossing $100 mark, the market is expecting higher yields, unless SBP comes up with some nuggets in the upcoming monetary policy.

The situation is becoming like what it was in December 2021 – auction targets were increasing, inflation was soaring, and market was demanding higher rates. SBP came up with fresh forward guidance (in Jan-22) and 63 OMOs (from Dec-21) to calm the market down. Now these 63 days OMOs are maturing, and market is craving more. The OMO net injection has crossed Rs3 trillion – and given such liquidity starved market, the rates can only move north. SBP must use its power of outright purchase in the secondary market to ease liquidity. BR Research is advocating this option for months. It’s about time for SBP to end this permanent liquidity shortage situation.

Anyhow, the government has accepted Rs235 billion (against participation of Rs348 billion) in 3M at the cut-off of 10.49 percent- up by 19 bps from the previous auction. The participation in 3M was similar; but weighted average yield is up by 12 bps to 10.38 percent. The situation in 6M is grimmer. The participation was almost half at Rs228 billion, and the government accepted mere Rs69 billion (previous auction Rs173 billion) at cut-off of 10.89 percent (up by 23 bps) and weighted average yield is up by 21 bps.

The market is clearly asking for more in six months. Market is probably expecting no (or minor) change on 8th March inline with the SBP’s forward guidance. However, seeing two twists in forward guidance in the past six months amid fluid global geopolitical situation, market is not ready to forgo risks for investing beyond 3M. The situation is similar for 12M papers where the government accepted mere Rs31 billion (last auction Rs81 bn) at 11.0 percent – cut-off up by 12 bps.

The next auction is 9th March, and the target is Rs1,000 billion. Moreover, there is shortage of Rs433 billion in this auction. The number is growing, and the government must accept whatever the market offers. And the role of SBP (to be revealed on 8th March monetary policy) could be to curb market’s enthusiasm. Stay tuned.

Comments

Comments are closed.