Oil and Gas Development Company Limited

Oil and Gas Development Company Limited (PSX: OGDC) is the largest E&P company in the country with operations including exploration, drilling operation services, production, reservoir management, and engineering support. It has the largest exploration acreage in Pakistan, covering around 43 percent of the country’s total acreage awarded with net hydrocarbons of oil and gas standing at 43 percent and 36 percent respectively as of June 2021. The company contributed to 29 percent of Pakistan’s total natural gas production, and 48 percent of its oil production, and 37 percent of its LPG production in FY21.

Shareholding Pattern

With over 67 percent, the Government of Pakistan is the largest shareholder in OGDC followed by OGDCL Employee Empowerment Trust and Privatisation Commission of Pakistan. A breakup of shareholding pattern in given in the illustration.

OGDC in the recent past

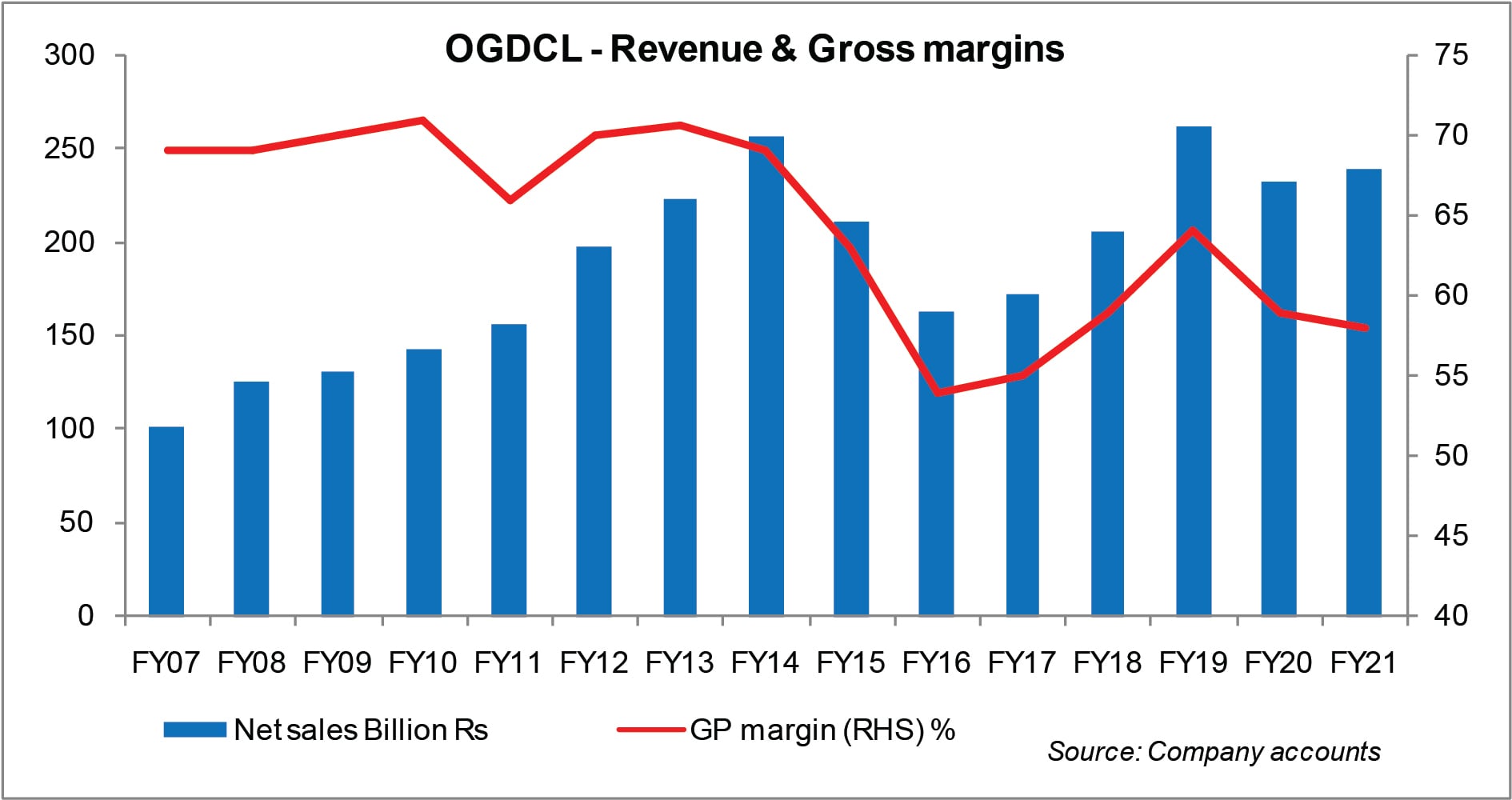

On the operational side, OGDC has been leading the pack of E&P companies not only because of its size, but also its aggressive exploration and drilling activities over the course of its history. Its steady rise in production flows amid depleting country reserves show the strength of the company. Over the years, the company has seen a growth in the total volumes sold of oil gas and LPG along with steady rate of hydrocarbon discoveries.

In FY18, OGDCL’s oil volumes continued to rise, while the company faced a decline in gas volumes sold – which can be taken as a decline in production. Profitability on the other hand continued to improve primarily due modest recovery price of crude oil. Plus, higher LPG production complemented by favourable exchange rate and planned capital spending contributed positively to the financial growth in FY18. Also OGDC made 4 new oil and gas discoveries during the year. However, increase in operating expenses, depreciation and higher cost of dry and abandoned wells owing to 11 wells declared dry and abandoned in FY18 against 4 wells in FY17 were inhibiting factors for earnings.

In FY19, OGDCL’s revenues were seen climbing by 27 percent year-on-year, and botomline expanded by 57 percent year-on-year. The rise in revenues came from higher average realised crude oil prices as well as higher average realised gas prices. On the production side, crude oil production and gas production remained flat, while LPG production increased during the year. The company spud 16 wells in FY19 and it made three new oil and gas discoveries.

Also, rise in average exchange rate, and increase in other income and share of profit in associate accompanied with decline in exploration and prospecting expenditures strengthened the bottomline. However, profitability in FY19 was partially impacted by increase in operating expenses mainly on account of amortization expense.

FY20 was a slow year in general and for the E&P sector too where crashing oil prices along with COVID-19 had key impact on the sector’s financial performance. OGC’s bottomline slipped by 15 percent year-on-year, where most of the decline came from 2HFY20. The squeeze in earnings started from the top as revenues decreased by 6 percent year-on-year. The decline was both due to falling crude oil prices and production levels. Realized prices of crude oil witnessed a drop of around 20 percent whereas LPG realized prices also fell by 11 percent in FY20. Production numbers were also subdued as COVID-19 left many fields in partial shutdown mode. Oil and gas production thus witnessed decline of around 12 percent each in FY20, while LPG production fell by around 11 percent.

The company incurred an increase in operating expenses, which aided the decline in gross profits. Absence of exchange gains restricted other income growth and increase in all expenses including exploration, general administration, and finance cost also impacted the bottomline. Growth in exploration expenses was due significant cost of dry and abandoned wells during the year as 8 wells were declared dry and abandoned in FY20 versus only 2 in FY19.

FY21 was a year of recovery and this was also witnessed across the E&P sector. The trend of falling average gas production continued in FY21 and for OGDCL it was lower by 2.6 percent year-on-year. However, some recovery was witnessed by OGDCL in its crude oil production which increased by 2.3 percent year-on-years. Along with the increase in crude oil and LPG production volumes, average realised prices for natural gas up by 8 percent year-on-year were the driving factors for revenue growth for OGDCL in FY21. However, decline in gas production as well as flat crude oil realised prices offset the gains, and OGDCL’s topline grew marginally by 2.65 percent in FY21.

Earnings for the E&P Company grew by 9.3 percent year-on-year, which was supported by a 5 percent year-on-year decline in the exploration and prospecting expenditure as less number of dry wells was incurred in FY21 versus FY20. However, the profitability during the year was affected by reduction in other income due to exchange loss and decline in interest income, and higher operating expenses primarily due to higher amortization, development and repair cost.

FY22 and beyond

The earnings for the E&P giant continued to be a multiple of 2Ps: price and production. During the 1QFY22, OGDCL’s revenues grew by 27 percent year-on-year, while the bottomline growth stood at 44 percent year-on-year. Topline growth was driven by a whopping 60 percent year-on-year rise in average realized crude oil prices along with a 5 percent rise in average realized natural gas price. Production of crude oil was up by over 3 percent year-on-year too. However, gas production was down by around 7 percent year on year. Along with the increase in crude oil and LPG production volumes, average realized prices for natural gas was also higher by 8 percent year-on-year.

Growth in OGDCL’s bottomline was also lent by lower operating and exploration expenses. Prospection and exploration expenditure was down by 23 percent year-on-year as one well was declared abandoned and dry in 1QFY22 versus three in 1QFY21.

Comments

Comments are closed.