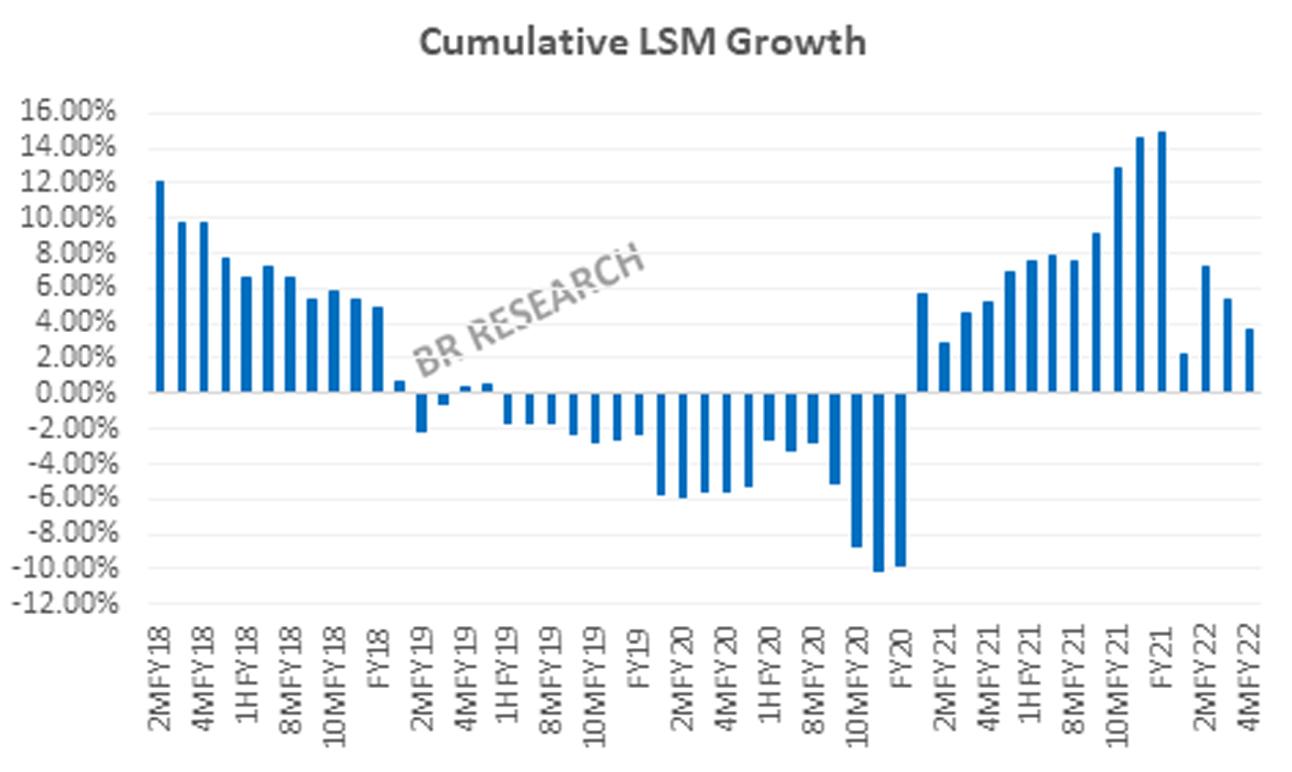

The heat has not lasted long, as the Large-Scale Manufacturing (LSM) growth numbers for October 2021 returned a negative reading. This is the first instance of negative year-on-year growth ever since the Covid-induced LSM readings from March 2020 to June 2020. The low base effect is no more there to mask the numbers, as the cumulative Jul-Oct growth at 3.57 percent is a middling one at best.

Recall that ten of the last twelve months had returned highest-ever monthly LSM index values, signaling there was more to growth than just the low base. To be fair, October 2021 LSM growth is down only by 1.2 percent, and that too comes against the highest-ever October index reported last year. There is not much one should read from a solitary month – it does not become a trend yet. That said, the pace of growth, it seems, will remain checked if the first four months are any guide.

With interest rates jacking up, power and gas tariffs going higher, it is difficult to see LSM growth repeating the heroics of FY21, or even reaching double-digits by the end of FY22. The LSM growth continues to be headlined by the automobile sector, which contributed more than half to the 3.56 percent growth, with less than 5 percent share in the LSM composition.

Sector experts opine the automobile rally is likely to cool down as the interest rate reversal takes full effect. Automobile sales may not necessarily post negative year-on-year growth just yet, but the impact on LSM contribution is likely to be cut to size, much in relation to its proportion, come H2 FY22. Another sector likely to take the brunt of higher interest rates, and reduced PSDP spending is cement, which has already entered the red zone, as cement sales come off the rail.

The food sector growth has also moderated from high teens to just 5 percent in four months, reverting to mean values. Textile never really took off and has constantly returned negligible monthly growth. Combined, these two, account for more than one-third of LSM – and the growth prospects do not look overly promising, given the near-term inflation outlook.

Mind you, the industrial activity is nowhere near the peaks seen in FY17-18, as evidenced from HSD consumption, which is primarily used in goods’ transportation. A large number of large-scale industries continue to produce significantly lower than the peaks of FY18. Surely, there were no signs of heating up in the LSM at least. With external and fiscal challenges back at the forefront, alongside higher inflation, the LSM story in the second half could look more like FY19 than FY21.

Comments

Comments are closed.