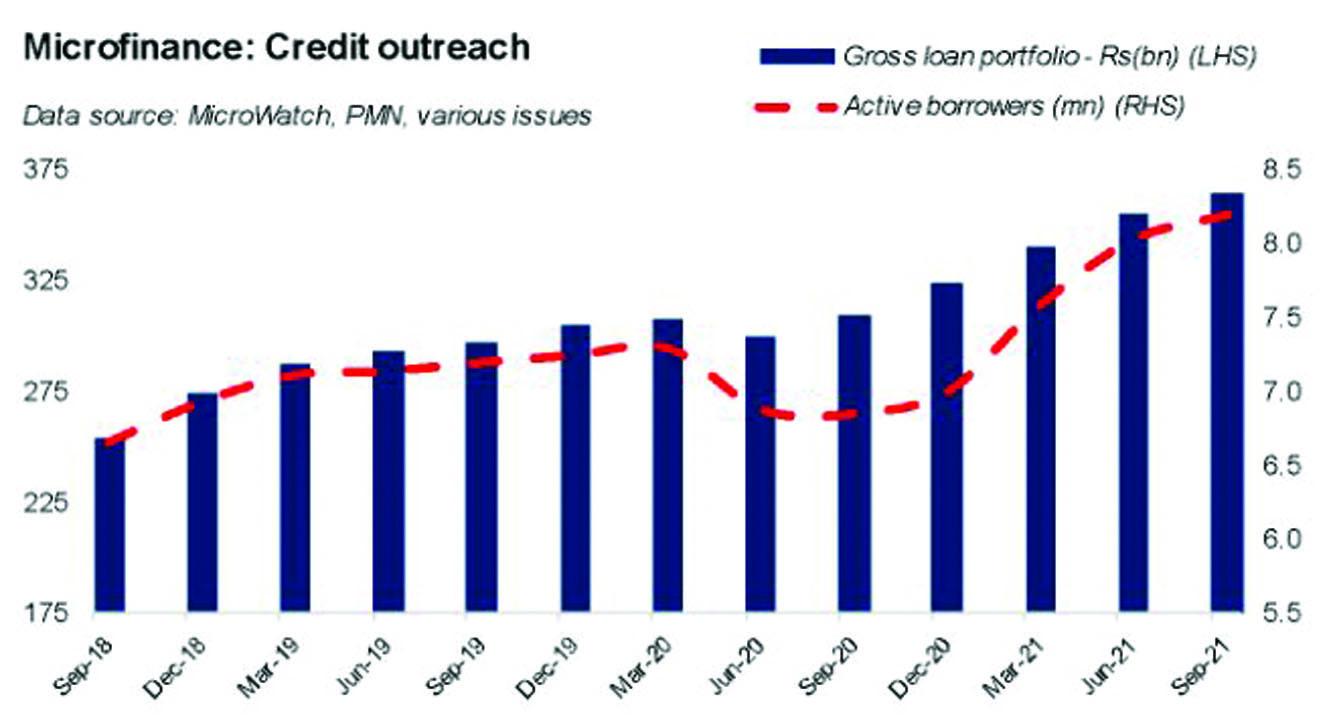

About a year and a half since the pandemic, the country’s microfinance sector is presenting a steady picture, as per the latest quarterly data released by the sector association Pakistan Microfinance Network (PMN). At the top, the number of active microfinance borrowers had reached almost 8.2 million in the quarter ended September 30, 2021 – which translates into 2 percent growth over the previous quarter and 20 percent growth over the same period last year. (The latest aggregated sector figures are reported by nearly three dozen microfinance providers (MFPs) to the PMN).

The net addition of some 1.4 million borrowers since September 2020 manifests in the expansion of the credit portfolio. As of September end 2021, the gross loan portfolio (GLP) had reached nearly Rs366 billion, exhibiting 3 percent quarterly growth, with a much higher 18 percent year-on-year growth. These numbers suggest that credit was, fortunately, not frozen in the microfinance system, despite the liquidity challenges arising out of the Covid-19 pandemic. The sector is now well past the dip in credit outreach numbers those were seen in the first six months of the pandemic.

The savings department, meanwhile, continues its ascent, equipping the MFPs (essentially microfinance banks) with a relatively low-cost source of financing to fund their credit operations. As of September end 2021, the value of savings had crossed Rs384 billion, showing 1 percent quarterly growth and 20 percent yearly growth. The number of savers grew by 24 percent since September 2020 to cross 72 million – an addition of almost 14 million. Since the onset of the pandemic, the number of savers has increased by a whopping 23 million! However, there is a visible slowdown in growth during the ongoing calendar year.

In short, in the year until September 2021, the MFPs had collectively raised the size of sector GLP by Rs56 billion, whereas their deposits in the same period had increased by roughly Rs63 billion. While this gives an impression that credit growth was financed by deposits, it is applicable more to microfinance banks than microfinance institutions, as the latter (which include rural support programs, grassroots organizations, and non-profits) do not have a banking license and as such cannot take public money. As a result, microfinance banks have had a major role in expanding credit outreach in recent quarters.

The sector’s infection ratio – which is measured as the portion of the loan portfolio at risk for more than 30 days – stood at 5.9 percent as of September 2021, up from 4.8 percent a year ago. The jump in infection ratio is presumably due to the previously-restructured/deferred loans that have been becoming due. Breaking it down, the infection ratio increased from 5 percent to 6.4 percent for microfinance banks in this period, whereas the infection ratio had a comparatively lower increase from 4.2 percent to 4.6 percent for microfinance institutions, indicating caution in the face of a difficult operating environment.

Recent amelioration in statistics is clouded by the fact that there is a growing concentration of small-ticket digital loans on the credit front and low-value mobile wallets on the saving front. While using digital means is key to expanding the sector's outreach, real microfinance requires hard work to assess client needs and fulfill them while maintaining diligence. In that respect, the sector has a long way to go to provide coverage to a large addressable market that was previously estimated at 47 million micro clients and enterprises by the PMN.

Comments

Comments are closed.