Last week, APTMA – the mothership of textile industry associations – endorsed GoPs’ export target of $21 billion for the ongoing fiscal year. Achieving the target would be no small feat, considering it would require 36 percent growth over last year. Can it happen?

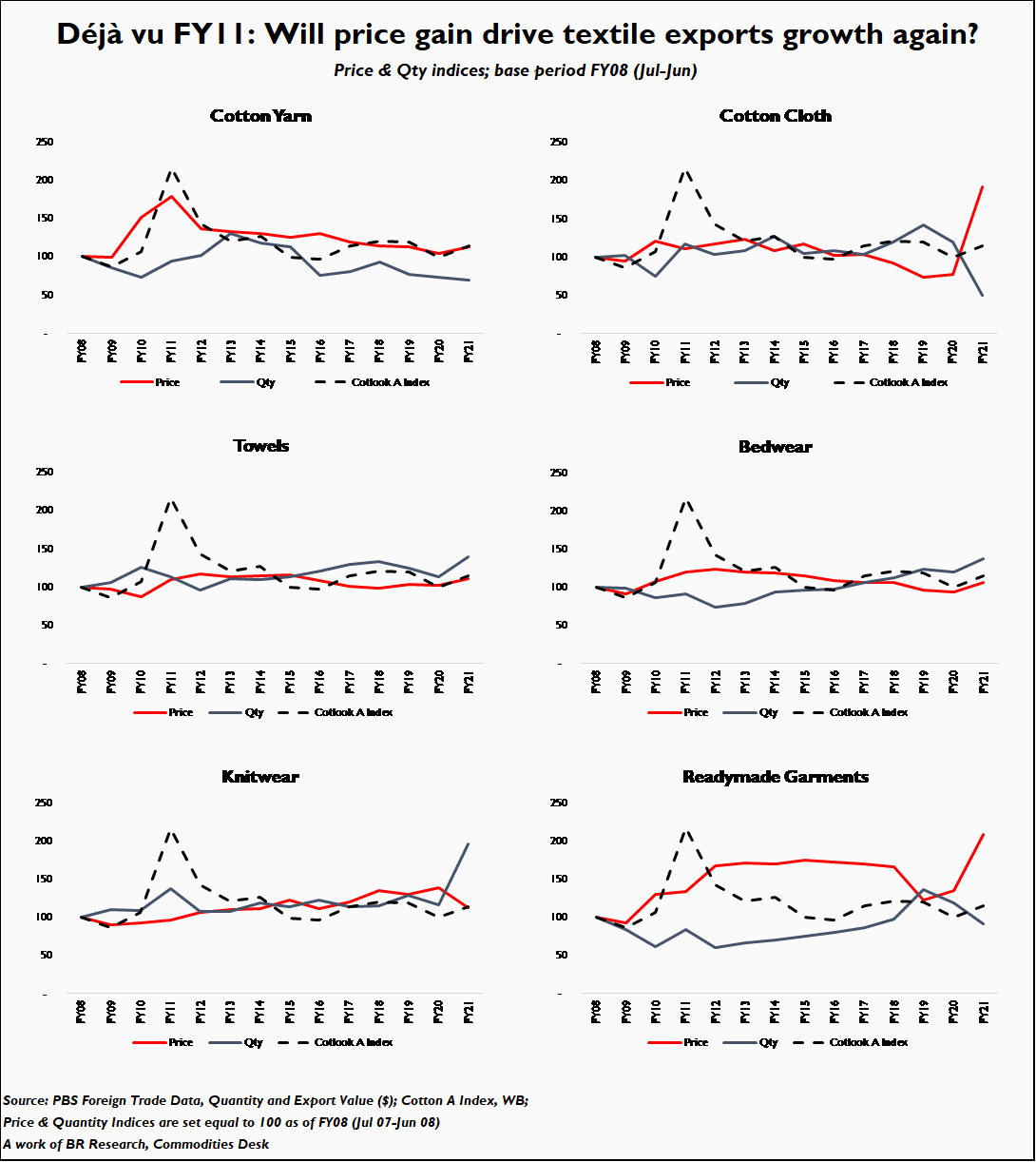

In the past 35 years, textile exports have only grown once before at such a high pace. Back in FY11, industry’s exports grew from $10.2 billion to $13.8 billion, a giant leap of 35 percent. Unfortunately, the growth momentum proved fleeting, as sector exports under-performed over the following 10 years, barely struggling to average at $13 billion by FY20.

So, how did exports grow by over one-third in one year back in FY11? Can it happen again? If it does, will the growth momentum be maintained, or stagnate at the new base? One must step back in time to answer to those questions; and examine Pakistan’s textile exports in the pre-2011 era.

In November 2011, world cotton prices had doubled in less than 12 months on the back of phenomenal rise in global prices, quite like the one we see today. Although world cotton prices have so far not doubled over preceding 12 months, they very much appear to be traveling in that direction, especially with China entering international market as a strategic buyer to build its reserves (refer US ban on Xiangyang cotton).

Naturally, a phenomenal rise in global raw material prices back in FY11 quickly translated into improved earnings for textile exporters. More significantly, it wasn’t just unit prices that improved, but also quantity exported (barring few categories), as industry was able to increase volumes, possibly on the back of better margins (due to cheaper raw material buying, before world prices ran amok).

Why then did the industry not manage to maintain the growth momentum in the following years? Of the $3.4 billion incremental textile export earnings recorded between FY10 and FY11, over half were contributed by low-value add products such as raw cotton, cotton yarn, and cotton cloth exports. When world cotton prices crashed back to pre-2011 levels in the following two years, so did export earnings from low-value add goods; whose unit prices never recovered the peaks witnessed in FY11.

The trend changes for medium value add categories (such as towels and bedsheets), and high-value add categories (such as knitwear and readymade garments). Although bedwear and towels prices also tumbled in the years following FY11 (and never did prices aim for the FY11 peak again), volume exported held on. Within higher-value adds, not only did volume sustain themselves in the following decade, but unit prices also continued to march on (albeit incrementally), only suffering minor hiccups in recent years.

But this isn’t FY11. Back then, high-value adds (knitwear and readymade garments) contributed only one-third of textile export revenue; by FY21 the same has breached over half. Concurrently, contribution of low-value add (cotton yarn and cloth) has fallen from a peak of 41 percent to just 22 percent; with a value decline of $2 billion in absolute terms.

Yet, if FY11 and its fateful commodity price spiral is any guide, lower value-add items will witness the quickest, yet the most fleeting price gains today as well. Once world cotton prices start falling – as they will eventually – yarn and cloth export unit prices will prove to be the most ephemeral, falling faster than they rose.

It remains to be seen whether the rise in global commodity prices will herald a growth in low-value add exports (yarn and cloth) volume. Disturbingly, Pakistan’s total yarn output has recorded no substantial improvement, indicating that the overall raw material available to value-add producers is not growing. GoP may find itself tempted by higher international prices for yarn and cloth. Lobbies may advocate incentivizing a switch to greater share of yarn/cloth in the exports mix, so the FX starved nation may seize on an opportunity to mark quick gains in export revenue. That would be a mistake.

If yarn and cloth export volume grow – even as total yarn output remains static – the situation would translate into lower raw material availability to towel, bedwear, knitwear, and readymade garments producers. Some of these have already been advocating removal of duties on yarn and cloth import (as raw material), which will cancel out any forex gains made from incremental yarn and cloth exports. Given its current account ordeals, GoP may be desperate for quick wins through textile export growth. Rather than seeking the $21 billion target mercilessly, it would be better advised to ensure that export growth is sustainable, and comes on the back of higher value-add volume increase.

Comments

Comments are closed.