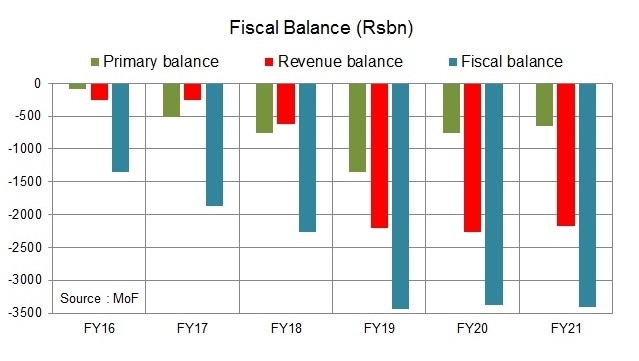

The fiscal performance in FY21 remained largely in line with expectations – the consolidated deficit stood at 7.1 percent of GDP in line with what was budgeted, and a slightly higher against provisional deficit (7% of GDP). However, having three consecutive years of over 7 percent fiscal deficit is not good news – it’s happening the first time since 1980s – during FY85-93, eight out of nine years had over 7 percent of GDP deficit.

Controlling the deficit is of utmost importance to curb inflation and keeping current account deficit tame, as with higher deficit, money supply increases more relative to the supply of goods and services and this tends to create demand pull inflation. Running high deficit during the 80s/90s had higher inflation in subsequent years – during FY89-97, seven out of nine years had double digits annual inflation.

The key indicator (under the IMF programme) is the primary fiscal balance- the deficit stood at Rs654 billion (1.4% of GDP) as against the IMF target of Rs246 billion. The slippage is mainly in the last quarter, as the deficit in the 4QFY21 stood at Rs1.1 trillion washing away Rs454 billion surplus in the 9MFY21. In 4QFY21, the overall fiscal deficit stood at Rs1.8 trillion (3.5% of GDP) – it is 4 percent higher than Rs1.7 trillion (4.3% of GDP) in the same period last year.

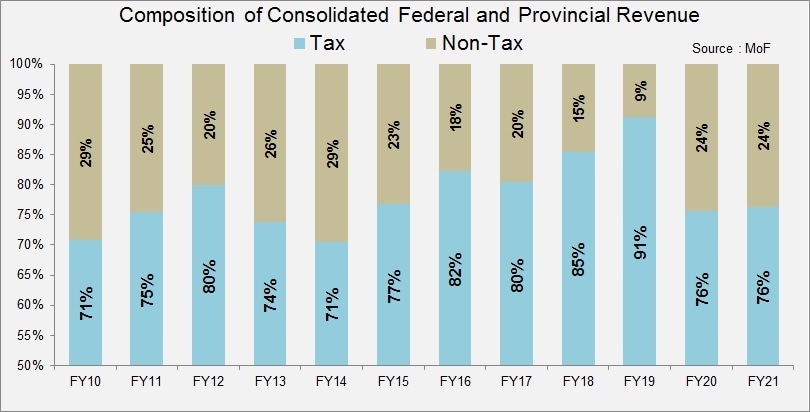

The fiscal revenues – especially tax revenues—performed better in FY21 as pickup in economic activities (along with growth in imports) resulted in the FBR meeting its target of Rs4.7 trillion. Overall tax revenues are up 11 percent to Rs5.3 trillion and the growth in the fourth quarter stood at 31 percent – previous year 4th quarter was slow due to lockdowns.

Within taxation, FBR revenues are up by 19 percent to Rs4.8 trillion. Direct taxes are up by 14 percent to Rs1.7 trillion while the growth in indirect taxes stood at 23 percent to Rs3.0 trillion. The highest growth is in federal sales tax (on goods) at 25 percent to Rs2.0 trillion and the custom duties collection are up by 22 percent to Rs765 billion.

Non-tax revenues are up by 7 percent to Rs1.6 trillion. Barring petroleum levy (PL) which is now classified as non-tax revenues, the non-tax revenues fell by 21 percent in FY21. PL collection stood at Rs425 billion – up by 45 percent. However, by now passing on the oil prices to consumers, the revised target of Rs500 billion for FY22 is elusive. The reason for non-tax revenues (barring PL) remaining short in FY21 is the fall in SBP profits by 30 percent to Rs635 billion as FY20 higher numbers were one-offs.

The overall fiscal revenues are up by 10 percent in FY21 to Rs6.9 trillion. On the other hand, the overall expenditures growth is curtailed by 7 percent to Rs10.3 trillion. Still the deficit in absolute terms marginally grew by 1 percent to Rs3.4 trillion.

The current expenditures are up by 6 percent to Rs9.1 trillion. Within expenditure, the biggest item is markup payment – debt servicing, which is up by 5 percent to Rs2.75 trillion. The domestic debt servicing is up by 9 percent to Rs2.5 trillion while foreign debt payments are down by 26 percent to Rs226 billion. The growth in markup payment is even though interest rates are down to almost half at 7 percent. The reason is locking in a higher rate for PIBs in 2019 which start to mature in 2021-22 to lower the impact of high-rate fixed bonds servicing. But the question is at what rates would banks be willing to buy new bonds?

The defense expenditure is up by 9 percent to Rs1.3 trillion and in the fourth quarter, the defense expenditure grew by 30 percent to Rs532 billion. Pension spending is becoming significant with every passing year – though the expense is curtailed by 2 percent in FY21, the pension spending by the federal government is now equal to the federal PSDP. Just four years ago, federal pension spending was less than half of the federal PSDP.

The overall federal and provincial development spending and net lending grew by 9 percent to Rs1.3 trillion. The overall provincial revenues grew by 15 percent to Rs 3.7 trillion and out of it Rs2.7 billion (up by 10%) are from the federal divisible pool. The provincial tax revenues grew by 23 percent to Rs508 billion. The GST on services is standing at 58 percent of provincial tax revenues and are up by 26 percent to Rs294 billion. The highest gain is in motor vehicle taxes – up by 49 percent to Rs27 billion.

Overall provincial expenditure is up by 8 percent to Rs3.4 trillion – within it, Punjab and Baluchistan expenditure growth remained almost flat while the growth in Sindh and KP stood at 20 percent and 15 percent, respectively. Total development expenditure of provinces increased by 24 percent to Rs770 billion. The provincial budget surplus came at Rs314 billion which is 4 times the surplus in the last year. This implies that provinces got the money transfer on the very last dates and didn’t have time to spend. It is likely that provinces will accelerate spending and may not give similar surplus in the last two years of this term.

The overall fiscal budget deficit at Rs3.4 trillion in FY21 is primarily financed by the domestic banking sources with 61 percent of financing is relied on domestic sources – and within it, 91 percent is coming from domestic banking sources. However, the reliance on external sources has increased in FY21 as the financing mix was 61:39 in favor of domestic finances as compared to ratio of 73:27 in FY21.

The government needs to control the fiscal deficit going forward to reduce the growth of debt. The domestic debt is alarmingly high and with growing current account deficit, government would look forward to having fiscal financing more from external financing. For both debt accumulation and to curb future inflation, government must end this streak of 7 percent deficit in the next two years. However, with lower expected collection on PL, the chances of having another 7 percent or greater deficit in FY22 are high.

Comments

Comments are closed.