Sunrays Textile Mills Limited

Sunrays Textile Mills Limited (PSX: SUTM) was set up as a public limited company in 1987 under the Companies Ordinance, 1984. It is part of the Indus Group of Companies. The company essentially trades, manufactures and sells yarn. Its mill is located in Dera Ghazi Khan Division, Punjab.

Shareholding pattern

As at June 30, 2020, majority of the shares of the company, over 87 percent, are owned by the directors, CEO, their spouses and minor children. Of this, a major chunk, over 21 percent, is owned by Mr. Kashif Riaz, the CEO of Sunrays Textile Mills. Over 5 percent shares are held by individuals followed by close to 5 percent held in mutual funds. The remaining 3 percent shares are with the rest of the shareholder categories.

Historical operational performance

The company has mostly seen a rising topline, with the exception of FY15 and FY16. Profit margins bottomed out in FY16, before rising again until FY20.

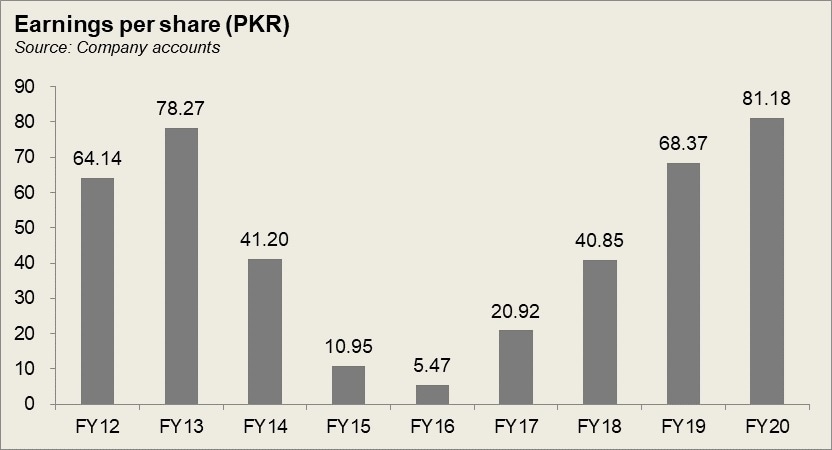

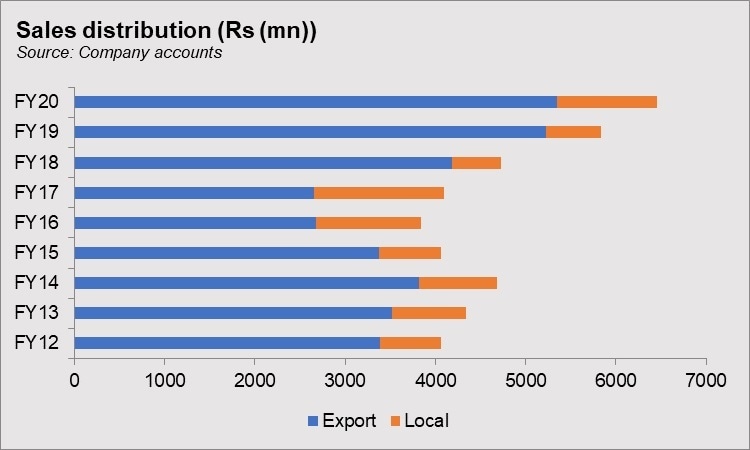

After contracting consecutively for two years, topline grew by over 10 percent in FY17. Although export sales still dominated the total revenue pie, most of the topline growth was seen in local sales; the latter registered a nearly 24 percent growth. This was due to better demand and margins in the local market compared to the global market. On the other hand, although cost of production still exceeded 90 percent of revenue, it was lower from previous year’s over 94 percent. This was in part attributed to raw material procurement planning. As a result, gross margin improved to 8.7 percent. With other operating expenses remaining more or less similar, net margin also improved to over 3 percent, compared to nearly 1 percent in FY16. In value terms too, bottomline was substantially higher year on year at Rs 143 million versus Rs 37 million in FY16.

In FY18, Sunrays Textile Mills witnessed the highest growth seen in topline thus far at 16.3 percent. Export sales grew considerably by 57 percent, while local sales shrunk by more than half. While currency devaluation allowed for better exports, yarn prices also increased that helped to raise revenue and margins. Cost of production also went down to 87 percent of revenue, allowing gross margin to reach a high of nearly 13 percent. Although finance expense grew significantly primarily due to short term borrowings, it was offset by the gain in revenue. Thus, the higher gross margin also translated into a higher bottomline, with net margin recorded at 5.7 percent.

The company witnessed the highest growth in topline at almost 23 percent during FY19, with most of the increase seen in export sales; the latter grew by 25 percent, while local sales inclined by 11.5 percent. Cost of production further went down to 84 percent of revenue which was the lowest seen in the last five years. As a result, gross margin reached yet another high of 15.7 percent. With most other factors remaining unchanged, the higher gross margin also trickled down to the bottomline, that grew to Rs 471 million; net margin also increased to a five year high of 7.7 percent.

Topline growth in FY20 at over 6 percent was relatively subdued in comparison to the double-digit growth seen in the last three years, consecutively. While both, local and export sales grew, local sales saw a bigger increase by 81 percent, while export sales grew by a marginal 2.3 percent, although export sales did continue to make a significant contribution to the total revenue pie. Cost of production, on the other hand, increased slightly to nearly 86 percent, reducing gross margin to 14 percent. However, the abnormal growth in other income combined with the drop in finance expense due to lower short-term borrowing allowed net margin to increase to 8.6 percent, with bottomline recorded at an all time high in value terms at Rs 560 million.

Quarterly results and future outlook

Revenue in the first quarter of FY21 was lower by 11 percent year on year. Given that majority of the revenue is earned through export sales, and with the country under a lock down, revenue most likely suffered. Cost of production was also significantly higher in 1QFY21 year on year, therefore net margin was lower at 3.45 percent compared to 9 percent in 1QFY20. The increase in cost of production was due to an increase in cotton prices without a corresponding increase in yarn prices.

The second quarter some improvement in revenue as business activities resumed and the lock down eased; revenue was higher by 21.7 percent year on year in 2QFY21. Cost of production was slightly higher in 2QFY21 owing to high cotton prices that were not matched by a rise in yarn prices. In addition, other expenses were also higher in the current quarter therefore net margin remained lower year on year at 9.8 percent compared to 11.7 percent in 2QFY20.

The third quarter of FY21 saw revenue higher by 31 percent year on year. demand in the global market had been high while Pakistan’s textile industry had the production capacity to cater to the higher demand. This was also furthered by the fact that lock downs in other countries led to orders being diverted to Pakistan. Cost of production was also considerably lower in 3QFY21 at 79 percent of revenue. This also translated to a higher net margin of 14.5 percent compared to 5.9 percent in same period last year. Cumulatively too, owing to other income bringing in additional support to the bottomline, profit margins were better in 9MFY21 year on year.

Apart from the risk of Covid-19 wave and its adverse impacts with the simultaneous vaccination drives, the industry also faces risk due to the cotton production of the country that was recorded at its lowest in the last three decades. Having to import raw material brings in considerable risk and uncertainty into the equation

Comments

Comments are closed.