Minimum support price on cotton, but for whom?

Prologue

The Economic Coordination Committee of the federal cabinet in its meeting on Monday reportedly considered fixing an intervention price for cotton to improve falling area under its cultivation. This decision follows other recent developments, beginning with a statement by the new finance minister that ‘price control regime on agricultural commodities needs to be reinstated to improve agricultural output’.

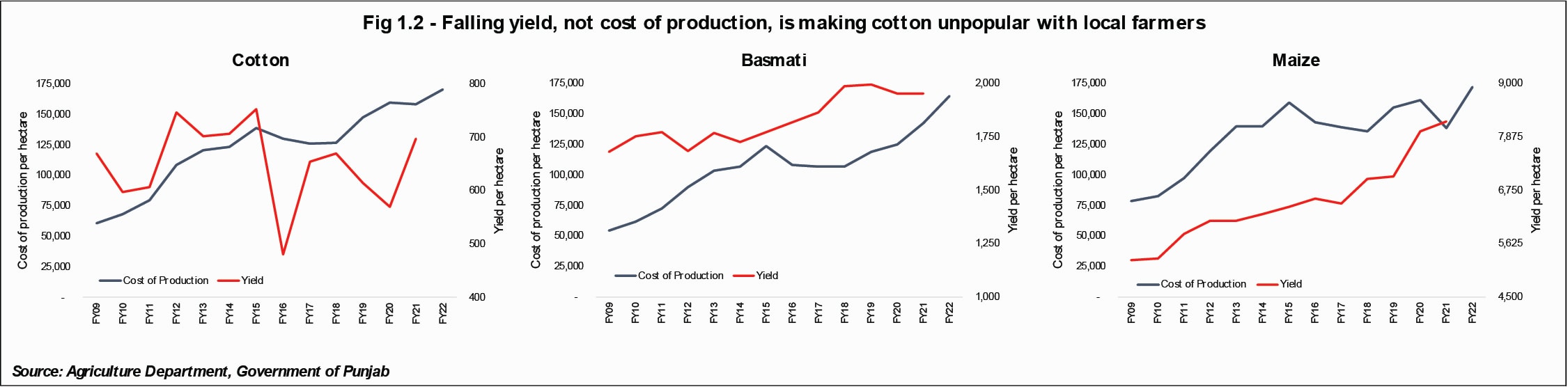

That Pakistan’s cotton output has fallen precipitously off a cliff needs no demonstration. According to official statistics, between FY16 and FY21, output fell by exactly half, barely retaining country’s slot among top five global producers. Although area under cultivation also fell by a quarter during this six-year period, it is a common mistake to blame the falling output on acreage.

Across the globe, leading cotton producing regions have increased cotton output not on the back of cultivated area, but by improving crop productivity, measured in yields per hectare. Over the last three decades, global cotton output has increased by over 50 percent as yields have made dramatic gains – increasing by over 5 times for Brazil, and by twice in China. In fact, productivity improvements have freed up land for plantation of other important competing crops, leading to hard won surpluses in global grain production.

So, does Pakistan need more area under cotton?

If estimates released by Pakistan Central Cotton Committee are to be believed, area sown under cotton during ongoing kharif season (2021 – 2022) stands at less than 1.85 million hectares, lowest since 1972. Clearly, cotton is no longer popular among local farmers - but fixing a minimum support price cannot help in reversing its fortunes.

According to estimates released by Punjab government, per hectare cost of production for cotton is at par with other competing kharif crops. Yet, lost cotton acres in the province have been the gain of competing crops such as basmati rice and maize. Over the last decade, cotton has lost 1 million hectares in the province alone, while cultivated area under both basmati and maize in the province has doubled. Interestingly, neither basmati nor maize enjoy any intervention or support price from federal or provincial government.

It is not hard to understand why. Competing crops have made impressive gains in productivity during the intervening period, while cotton yield has been on a downward spiral. Yes, competing crops offer higher per acre profitability, but not by virtue of higher prices, rather, because cotton farmers have faced crop failures, year after year.

If the produce never makes it to the seller due to failure of crop, does it make any difference whether price is set by the government or by market forces?

Cotton and other crops compete for the same parcel of land; have similar access to irrigation and groundwater; are tilled by the same farm hands; and use fertilizers manufactured by same corporations. Unlike sugar mills, cotton ginners are not accused of exploiting growers or fleecing them off fair price. In fact, as per news reports, half of over 1,200 cotton ginning factories in the country have closed operations during past two years due to falling output.

So, what plays the decisive role in the diverging trends between cotton and competing crop yields in the country? Briefly: poor seed quality.

While maize has grown in popularity due to impressive yields unlocked by imported hybrids seeds, yield improvements for basmati have also been made through quality seed and extension services offered by private sector rice processors. In contrast, cotton seed supplied locally is of dubious quality, a result of poor administration by seed control authorities, allowing illegal seeds to flourish in the local market.

Anecdotal evidence suggests that samples of Bt. – or seed with genetically modified attributes - imported through grey channels during early 2000s, were multiplied and marketed by local seed companies. Back then, first and second Bt, generation seeds - crossed with local varieties - gave remarkable results upon commercialization, allowing their murky origins to escape administrative scrutiny.

Soon after, because the seed had not received stewardship and support by patent owning biotech companies, pink boll worm and other pests began exhibiting resistance to its charms. In less than 10 years, use of pirated biotechnology resulted in tragic consequences, relegating cotton to its ongoing unpopular status.

In the past two years, the current administration has made flurry of attempts to revive cotton, with zero results to show. Not only is the crop fast losing its popularity, national yield refuses to inch forward. Common sense demands that dramatic reduction in area of any crop must lead to improvement in average yield, as only those farmers able to achieve competitive productivity may show resilience and stick to the crop. Yet, counter-intuitive results shown by cotton yield indicate that the quality and vigour of the seed is fast deteriorating, and may not improve unless the quality of available seed changes radically.

Does that mean Pakistan should import cotton seed varieties from other countries such as China, Brazil, and USA where average yield is double that of ours?

That mistake has already been made once, and must not be repeated. Foreign seed – whether Bt., organic, or hybrid, - may show wonderful results overnight, but unless regional, and national levels trials are run for the requisite 5 to 7 years (or as mandated by the prevailing seed regime globally), threats to its suitability in local environment may remain unmasked in the short term. Once any seed variety is commercialized, it is very hard to purge it from a country with over 5 million small farmers.

So, how can Pakistan provide feedstock for its export-oriented textile sector if its cotton output continues to decline at an exponential rate? To answer that question, a different question must first be asked:

Is the textile sector worse off due to non-availability of local cotton?

Over the last two decades, global fibre industry has undergone a fast-paced evolution. Not only has the share of man-made fibres increased from 30-70 to 40-60, quality of cotton fibre used has also improved drastically. Across the world, commercialization of third and fourth generation Bt. cotton seeds means that average staple length of cotton filaments has graduated from 24” to 28” and even 32” inches in many places. Mechanized crop picking in several countries has allowed production of cotton that has very low adulteration percentage, and is not contaminated during the picking process. Fibre produced as a result allows improved production of higher and finer count cottons, even though price of cotton has been on a secular decline globally due to advances in productivity that have reduced production cost.

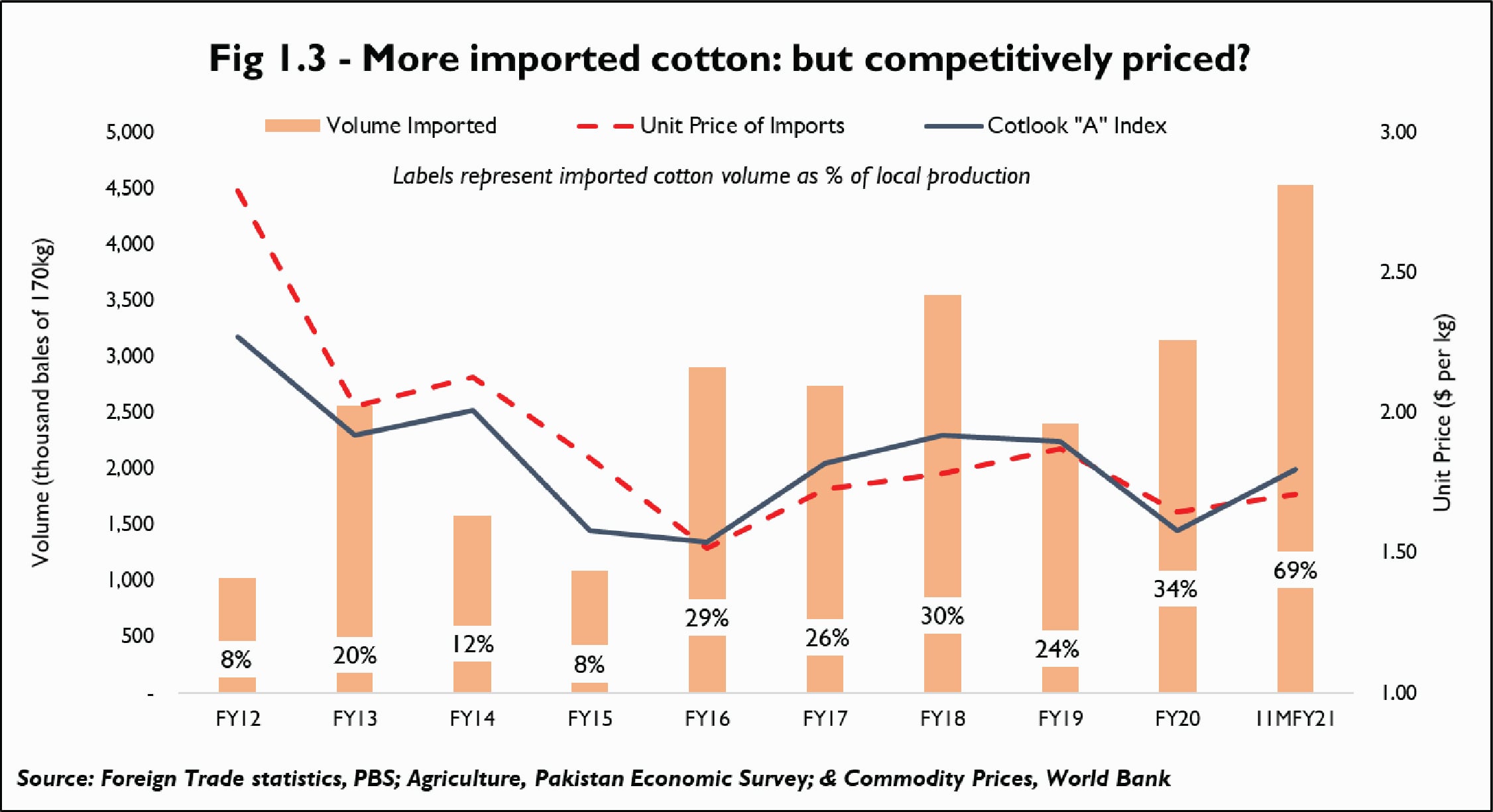

Meanwhile, according to Textile Commissioner’s Organization - a division of Commerce ministry - while local cotton production may have very well declined, domestic cotton consumption has not. TCO reports that annual cotton consumption by spinning mills continues to average between 13 to 15 million bales (of 170kg) annually. Thus, Pakistan is increasingly fulfilling its cotton requirements through imported raw cotton, but is it worse off as a result?

A comparison of unit prices of imported cotton over the past decade shows that as Pakistan’s appetite for imported varieties has increased, average unit price of imports has declined. Moreover, average unit price of import is no longer higher than the prevailing international prices during the corresponding period as had been the case in the past. As Pakistan becomes a bigger player in global cotton import and its spinners place purchase orders for bigger volumes than before, is our bargaining power as buyers improving?

While it is hard to make any conclusive remarks in absence of more evidence (a comparable analysis with other importing nations for the same period may be useful), it is equally hard to miss other obvious trends. Predictably, because most of Pakistan’s cotton imports originate from Brazil and USA, imported cotton is of better quality and higher staple count than locally available varieties. Another indirect way to measure the effect of cotton imports is to look at industry’s value-added output and analyse whether it has suffered due to higher reliance on imported feedstock.

Although total output of domestic textile value-adding industry is unavailable, exports serve as a useful proxy. Barring the exchange rate anomaly during FY14 – FY17, Pakistan’s value-adding export volume has remained resilient through the years. Moreover, unit price of value-added goods has improved not only in absolute terms, but also when measured as a multiple of unit price of imported cotton during the corresponding period.

Clearly, then, average textile exporter is in no way worse off due to higher use of imported cotton as raw material. In fact, an argument can be made that use of improved quality imported cotton may in fact help textile manufacturers break into newer value adding categories and attract buyers higher on the fashion and textiles ladder. Whether it has improved or hurt the profitability margins of value-added exporter is best left for textile analysts to comment on.

Thus, before government of Pakistan reinstates intervention price on cotton, it might help to contemplate ground realities:

a- Domestically produced cotton is competitively priced and is pegged against global cotton price indices that are reset on daily basis. Cotton – both domestically and globally – is priced based on its staple length, quality, micronnaire, and other standardized technical attributes. Cotton growers are paid competitive prices, which are only lower in the domestic market (when compared to unit price of imports) due to lower quality of the product. Can fixing higher-than-market-price for cotton help improve its quality?

b- In fact, imposition of intervention price will in no way improve the yield or quality of cotton, which is predicated on improvement of seed quality. Meanwhile, since minimum support price will be set above market rate, it will only lead to increase in price of raw material for domestic textile value-adding chain, rendering it uncompetitive in the global textile export market. Unless government also plans on banning imports, will textile industry be interested in paying a higher price for low quality local cotton?

c- Meanwhile, minimum support prices have a history of skewing the marketplace, as they offer abnormal returns (as price is set above market clearing level). This has already been advised by the SBP and CCP in the case of sugarcane. Meanwhile, it provides no guarantee on yield, which may or may not revive in absence of quality seed.

d- GoP insists that farmers have been better off in 2020-2021, backed by remarkable successes of competing crops such as rice and maize. By its own admission, these competing crops – together with wheat – have recorded highest ever output in country’s history. If farmers are already better off due to record profits thanks to their preference for competing crops, does it make sense to create interventions that skew them away from more profitable choices?

e- To rephrase the above argument, if farmers are better off financially growing competing crops, why must they be forced to grow cotton that is vulnerable to frequent failures due to environmental factors beyond GoP’s control? Will GoP offer insurance to 1.8 to 2.5 million hectares of cotton plantation in case cotton productivity continues to suffer in coming years?

f- In case GoP plans to procure cotton through TCP at higher prices and supply to spinning mills at lower, market-competitive prices – ala wheat/flour market – it must ask itself for how long does it have the fiscal space required to run this electoral gimmick? At 7 million bales, Pakistan’s current cotton output is valued at Rs 134 billion.

g- Lest GoP has forgotten, world’s second largest exporter of readymade garments is a country which has little to no indigenous production of cotton. Clearly, if textile export is to be revived, Bangladesh model, and not 20th century interventions such as minimum support price, is the way to go.

GoP must take pause and reconsider its decision to fix a minimum support price on cotton. Before a nationalistic urge to restore past glory turns into a death nail for cotton’s future.

Comments

Comments are closed.