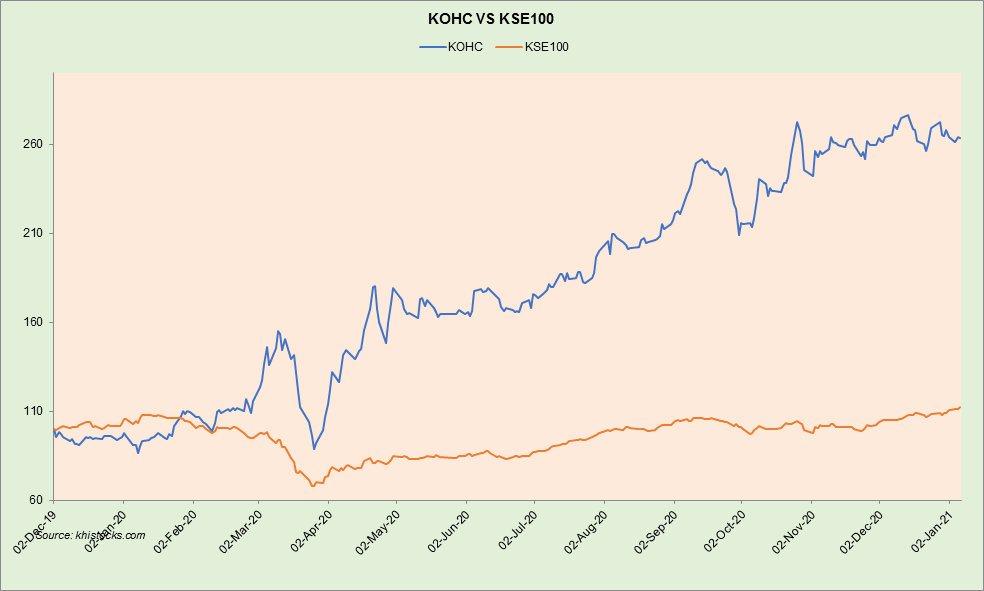

Kohat Cement Company Limited

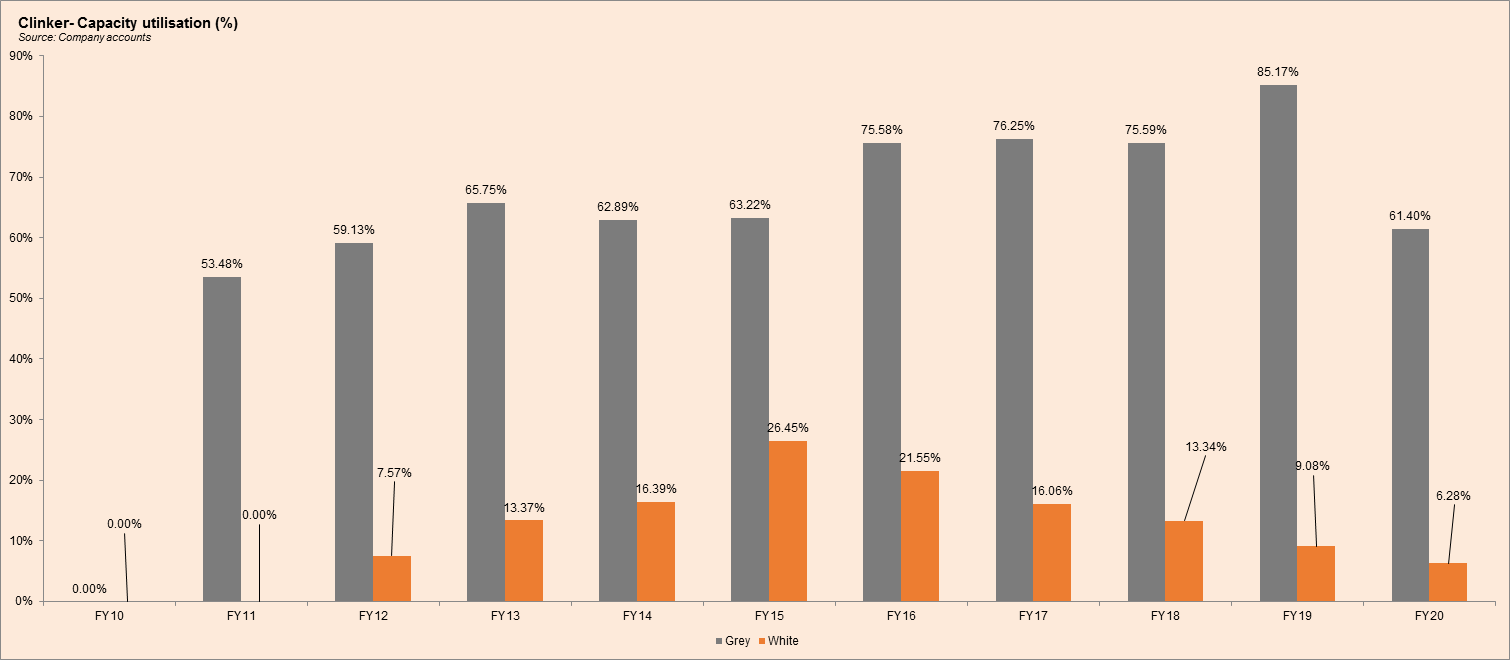

Kohat Cement Company Limited (PSX: KOHC) was established in 1980 under the Companies Act, 1913. The company produces and sells cement. In 2002, it entered the export market as well. As of June 2020, the company has a production capacity of 3.5 million metric ton grey clinker and 135,000 metric ton white clinker.

Shareholding pattern

As at June 30, 2020, about 55 percent shares of the company are held under the category of associated companies, undertakings, and related parties. Within this, 55 percent is held by ANS Capital (Pvt) Limited. The directors, CEO, their spouses, and minor children hold a little over 17 percent, of which Mrs. Hijab Tariq, a non-executive director, is major shareholder owning 16.74 percent of the total shares. Some 11 percent are with the local general public, followed by 10 percent in mutual funds. The remaining 7 percent shares with the rest of the shareholder categories.

Historical operational performance

The topline of Kohat Cement has been fluctuating over the past decade, while profit margins are on a decline after reaching a peak in FY16.

There was a 3.4 percent decline in sales revenue during FY17. While local dispatches saw a 4 percent rise, export dispatches fell by 41.5 percent. This was attributed to lower exports to Afghanistan due to slow demand as well as order closure for a significant period of time. On the other hand, cost of production was higher at 57 percent of revenue, up from 54 percent in FY16. Most of this increase was seen in coal, gas, and furnace oil expenses. Coal prices, particularly in the last quarter increased, combined with lower cement prices. With little changes in other factors of the financials, the effect of this was also reflected in the bottomline; net margin decreased to 26 percent, from 31.4 percent in FY16.

In FY18 there was a marginal decrease in sales revenue by less than 1 percent. The overall cement industry of Pakistan saw a volumetric increase of almost 14 percent with domestic consumption increasing by 15.4 percent, to 41.15 million metric tons. For Kohat Cement, local dispatches registered a 10 percent growth, while export dispatches reduced by 16 percent. This was due to transit problems between Pakistan and Afghanistan, and availability of cheaper cement from Iran entering into Afghanistan. Cost of production went up significantly during the year to consume nearly 68 percent of revenue. This was a result of currency devaluation coupled with a rise in coal prices. Thus, net margin fell to 22 percent.

Revenue increased by 16.4 percent in FY19, after witnessing negative growth for two consecutive years. Local dispatches for the company grew by 4 percent; export dispatches by 17 percent whereas the cement industry’s dispatches saw a volumetric growth by 2.13 percent; domestic consumption however had contracted by almost 2 percent. Cost of production, on the other hand, rose to over 73 percent of revenue. This was due to a combination of currency devaluation that caused prices for imported coal to increase; there was also an increase in prices of packing materials and electricity. In addition, cement prices reduced, particularly in the last quarter, negatively impacting profitability. Net margin decreased to almost 16 percent.

During FY20, Kohat Cement saw the biggest decline in its revenue by close to 28 percent. Local dispatches saw a less than 1 percent reduction, while export dispatches fell by 16.6 percent. Apart from a volumetric decline, a decrease in cement prices further reduced the topline. There was 9 million tons of additional capacity in the overall cement sector that reduced cement prices by 24 percent. With such a significant decline in topline, the company was unable to cover costs, resulting in a gross loss. although coal prices reduced in the last quarter, volumes were low due to the lock down in place in the wake of Covid-19. Therefore, net margin was recorded at a negative 4 percent. During the year, the company also started its new production line of 7,428 tons per day.

Quarterly results and future outlook

Topline grew by 73 percent during 1QFY21 year on year. While the overall cement industry saw a 21.88 percent increase in total dispatches, the company saw a nearly 71 percent increase in local dispatches and similar in export dispatches as well. This improvement was attributed to stimulus packages by the government to revive the economy after the lock down imposed towards the end of March 2020. The increased cement offtake has also resulted in a stop in the trend of falling cement prices. Cost of production was also lower year on year at 81.5 percent (FY20: 96 percent) of revenue. Therefore, net margin was better at 9.8 percent in 1QFY21 compared to 2.9 percent in FY20.

The key drivers for the cement sector are the infrastructure projects and housing. The company foresees increase in consumption coming from these two factors due to CPEC projects that includes economic zones, hydro power projects and government’s Naya Pakistan Housing Scheme.

Comments

Comments are closed.