Attock Oil Group’s refineries had a good time in FY17 in terms of commencement of long awaited projects. While National Refinery Limited (PSX: NRL) commissioned its Diesel Hydro Desulphurisation unit in June 2017 for producing High Speed Diesel (HSD) meeting Euro-II specifications, Attock Refinery Limited (PSX: ATRL) successfully completed the up-gradation project that consisted of a Pre-flash unit to enhance refining capacity, Naphtha Isomerisation Unit, Diesel Hydro Desulphurization Unit and expansion of existing captive power plant.

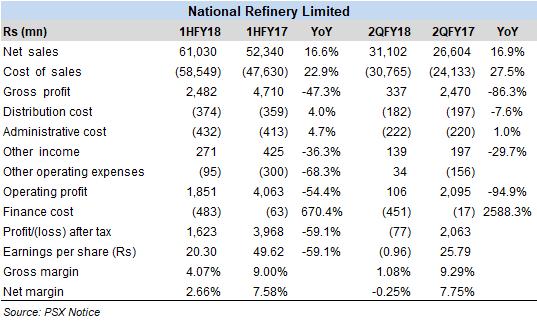

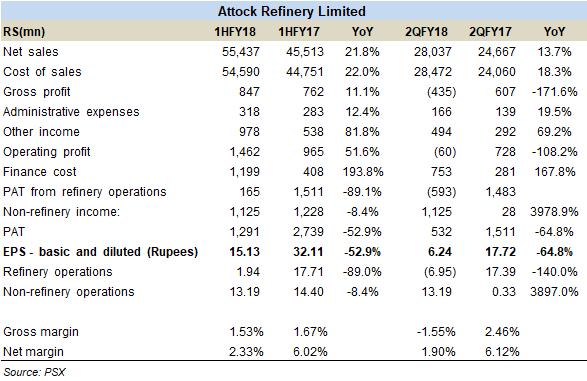

In terms of profitability, NRL’s overall financial performance in FY17 was dampened by the lube segment due to increase in feed cost. However, its fuel segment was able to put forth better earnings on account of better product prices in the international market and tax credit on up-gradation project. On the other hand, ATRL’s financial performance in FY17 was much celebrated as earnings increased by more than 500 percent due to NRL’s up-gradation project completion that increased in the refinery’s throughput capacity as well as increased its volumetric sales.

Moving to FY18, the two refineries seem to be in a little fix as their earnings for the first six months (1HFY18) have more than halved on year-on-year basis. While the first quarter’s earnings were satisfactory, the main culprit for a weaker 1HFY18 performance of the two refineries is 2QFY18.

The Lube segment has been giving trouble to NRL due to higher feed cost and unsymmetrical increase in product prices. While segment-wise details are not available, significantly weaker 2QFY18 could have been due to the continuing weak performance of the lube segment. Moreover, higher cost of sales, lower dividend income and higher finance cost all contributed to lower profit margins. ATRL too saw its earnings weaken in 2QFY18 on account of higher cost of sales and finance cost.

While the new projects have been able to lift the volumetric sales, these projects have also raised the finance cost for the refineries. And besides the increase in crude oil prices, the increase in cost of sales could have come from the closure the refineries in the north faced in November 2017 due to the shutdown of furnace oil-based power plants. A spill over impact of the abrupt closure of FO based power plants was also seen in refineries. During this furnace oil conundrum, it was also reported in the print that ATRL was heading towards a total shutdown.

Comments

Comments are closed for this article.