Pakistan is adding around 21000MW between FY17-22; and all the additions are in better fuel options than existing heavy reliance on furnace oil; plus, the efficiency of new plants are much better. Isn’t it just great? Hold your horses! What is the demand forecast? Will the new additions be completely utilized? Or will the capacity payments become a pain? What about the local refining of FO if we do away with all furnace oil-based plants?

These are some punching questions, the answers to which are hard to find from any document produced by government authorities. Well, the response that usually comes from the government is that they are producing clean and cheap energy and that they’ve struck the best deals. That might be the case; but you won’t buy more than what is required on a discount; would you?

Is this sheer incompetence? Or lack of coordination? Forming an integrated energy ministry was part of PMLN government’s manifesto for 2013 election; it took them over four years and a change of Prime Minister to make this happen. Is this too late?

Let's run through the brief history of energy management by the PMLN tenure. It started from 13,200 MW coal plants at ports, but soon the plan was shelved and replaced by CPEC projects and RLNG plants by Punjab and federal governments.

Once a few projects reached financial close, the then Water and Power Secretary, Younus Dhaga, put his foot down to not let any more imported plant be approved, and made a policy for having indigenous fuel plants (Thar coal, renewable and hydel) for medium to long term. But that was against the liking of a few in the power lobby, and Dhaga was removed from the ministry.

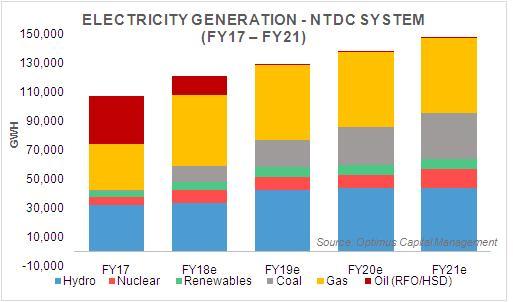

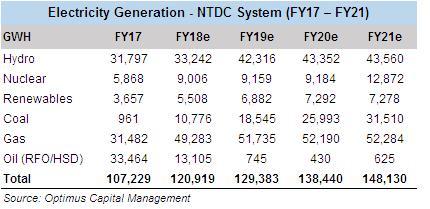

Now without any sophisticated demand analysis, a plethora of plants are coming online, making the power generation capacity to reach 42,640MW in FY22 from 25.983MW in FY17. A few new plants have been commissioned and rest are coming on gas (RLNG), coal, nuclear, hydro and wind. With every new megawatt being added, RFO is intended to be replaced. The electricity generation from NTDC system was 107.2 billion units in FY17 out of which 29.7 percent share was of FO. Out of 33.5 billion units produced on FO/HSD, 14.5 billion units were generated by plants that could run on gas. With the second RLNG terminal in effect, there is definitely a case of excess supply of gas, and wherever the generation is possible on gas, will be implemented.

According, to Optimus Research estimation, the FO/HSD electricity production will reduce to 13.1 billion units in FY18 and virtually to none thereafter. This is a good way of fuel saving as thermal efficiency of new plants is better; and based on current pricing, RLNG and coal are cheaper - FO costs at USD8.44/MMBTU in Karachi versus RLNG (USD7.35/MMBTU) and coal (USD4.0/MMBTU).

However, the catch is what to do with domestic refineries’ furnace oil production capacity and the capacity payments on new plants in case they are not used. For FO production fiasco, read “Dumping Furnace Oil” published on Nov 28, 2017". Let’s deliberate the capacity payment issue here. Optimus Capital Management’s calculations show that the increase in capacity payments due to new plant on coal and RLNG would be around $2.5 billion over the next five years.

If FO is replaced by RLNG and coal, the fuel savings would be around Rs3.1/KWH or Rs90 billion, and adjusting additional capacity payment the negative savings would be Rs1.8/KWH or Rs174 billion. Yes, that has to be recovered from consumers by increasing tariff by the same amount.

The point here is that under the current tariff structure, any new plant would have a capacity charge. The additional capacity cost can be justified only if the power being added is consumed. Else, it’s a problem. The energy pundit thinks that the new capacities are a little too much relative to the demand; and this may result in supply glut in years to come. The problem is compounded by incorporating the weak distribution and transmission system of the country. Can 42,000MW be handled by the system by 2022? Would there be demand to meet such capacity? How would local refineries operate in the absence of any demand? What are the political difficulties in retiring old GENCOs? These are the questions that had been dealt with in the drawing board meetings prior to committing too many power generation plants. But there was no coordination or competence of various department linked to energy. We now have an integrated energy ministry; but is it too late?

Well, it’s never too late. The energy minister happens to be the Prime Minister, and he probably has too much on his plate to carefully and deeply analyze the energy demand supply dynamics. The need is to slowdown in allowing new plants to come online before it’s become too late to handle.

Comments

Comments are closed for this article.