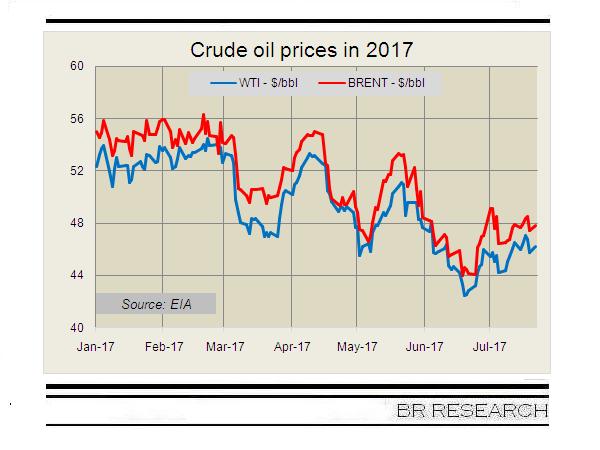

Global crude oil prices are set for their first monthly recovery in 2017 as monthly average prices cross the psychological barrier of $50 per barrel amid demand and supply rebalancing: where market demand continues to be bearish all year round, stronger demand in China and India in the last couple of months shrinking supplies due to large inventory draws recently have got the prices climbing.

The recent supply squeeze came from falling US crude oil stockpiles along with Saudi Arabia’s announcement to further reduce supplies in August 2017. However, a look back at the months of 2017 shows that oil prices continued to face heightened pressure in the ongoing year. Higher than expected Libyan and Nigerian oil production, US shale’s, weakening demand, Iraq’s pledge to boost capacity despite promises to cut production, and OPEC’s failure to match its promise of reducing supplies, all contributed to weak oil prices.

The recent supply squeeze came from falling US crude oil stockpiles along with Saudi Arabia’s announcement to further reduce supplies in August 2017. However, a look back at the months of 2017 shows that oil prices continued to face heightened pressure in the ongoing year. Higher than expected Libyan and Nigerian oil production, US shale’s, weakening demand, Iraq’s pledge to boost capacity despite promises to cut production, and OPEC’s failure to match its promise of reducing supplies, all contributed to weak oil prices.

According to Goldman Sachs, demand growth in Europe, America, India and China is expected to stay strong through the second half of the year along with sustained draws through the third quarter of the year.

However, the investment bank has labelled its stance on oil prices as ‘cautiously optimistic’ despite rebound in oil prices as continued draws will cause short-term tightness in the physical oil market, pushing the prices into backwardation – meaning cargoes for short-term shipment priced higher than those for later delivery.

Nonetheless, crude oil prices are still as precarious as they could be. Royal Dutch Shell PLC has drawn a very bleak picture of crude oil in its recent outlook where it said it is preparing for a world in which crude prices never return to pre-crash levels and petroleum demand ultimately declines.

Comments

Comments are closed for this article.