The biggest economic problem in Pakistan is persistently high fiscal deficit and within it the narrow tax base and low tax collection. The tax collection has increasingly become indirect in the last decade and within it the reliance is tilting towards collection at import stage - 43 percent of FBR net tax collection in FY18 was collected at imported stage.

This is creating a dilemma for policymakers on how to deal with taxation mess. The need is to go back to the drawing room to run the basic analytics to ponder on why 20,000 FBR work force is needed - collection on demand was a mere 7 percent of total direct taxes and 3 percent of overall FBR revenues in FY18.

The other paradox is delinking the tax policy from trade policy as the taxes on imports are used for revenue purposes, while the tariff policy is supposed to be used for improving trade balance, and bringing competitiveness in the domestic economy.

The policies ought to be dynamic as there are interdependencies of fiscal, trade and investment policies; as revenue considerations are paramount in the short run with an objective to lower the fiscal deficit to bring macroeconomic stability. In the medium to long term, the taxation ought to be linked to improving trade balance, competitiveness and bringing investment for optimal resource allocation and efficiencies.

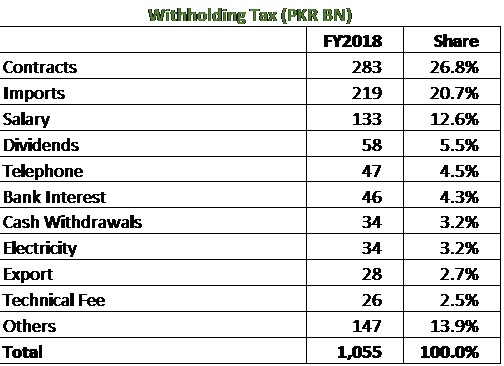

The FBR’s 20,000 plus workforce has to be evaluated against the direct tax it collects. Out of Rs1,537 billion direct tax, which is two fifth of FBR revenues, Rs1,055 billion (69% of direct tax) are withheld at source and Rs336 billion (22% of direct tax ) are advance taxes - mainly coming from banks and large firms.

In FY18, a mere Rs42 billion were raised from filing returns (3% of direct tax) and Rs104 billion (7% of direct tax) collected on demand. This raises serious doubt on the efficacy of the FBR team as two percent increase in GST rate from 17 to 19 percent would yield Rs175 billion on FY18 numbers - higher than on demand and collection from return, cumulatively.

Thus, hypothetically, sending the FBR workforce packing, would have no impact on overall collection, if GST is raised by 2 percent. The policy in the past ten years has been to increase the GST - the rate is to increase by one percent in five years, and to lower the income tax rate - reduced from 35 to 30 percent for corporate. However, the FBR work force did not shrink correspondingly.

The expected minibudget in Jan19 may increase the GST further by one percent to 18 percent, and maintain the policy of reducing income tax rate from 30 to 25 percent in five years. It should come up with shifting excess manpower of FBR to some other jurisdictions.

That is one leg of the problem that the policymakers have implicitly given up on the FBR for collecting direct taxes. The other interlinked problem is that taxation is skewed towards a few sectors as majority of sectors are either exempt or simply not paying their due share of taxes. In direct taxes, banking companies take the lion’s share while the rest is primarily contributed by handful of companies in fertilizer, automobile and other big sectors.

Textile, IPP and a few others are exempted while majority of modern services pay income tax indirectly. The wholesale and retail trade, whose contribution in GDP is equal to agriculture, are contributing almost nothing as income tax. The other services like private health, education, legal consultancies and food outlet are not taxed enough. The income tax is mostly withheld at contract stage- Rs283 billion (18% of direct taxes).

The indirect taxes, 60 percent of total, are concentrated in oil and gas, telecom, cement and tobacco. The biggest sector contribution is coming from POL (petroleum) products - 32 percent of GST at import stage and 42 percent of domestic GST, collectively Rs547billion are collected from POL GST i.e. 15 percent of total FBR collection.

In the last few years, the import stage taxes have been imposed on even essential raw materials and intermediate goods which has created an anti-export bias, and reduced the ability for domestic sectors to expand which paves way for reverse of import substitution.

The other unintended consequence of higher taxes at import stage is creating incentives for under invoicing and smuggling. The undocumented trade related payments are routed through grey channels which are settled against inward remittances without money crossing the border - fueling money laundering.

The government has to move away from taxation at imported stage. The problem is that direct tax collection has limited potential, especially with the existing FBR force. Since many sectors are either exempted or the FBR is incapable of bringing them in the net, the onus of taxation ought to fall on existing players. This may further exacerbate the problem of tax compliance - one major disincentive for investment.

The government has to turn the tables to solve the puzzle. The FBR’s role has to be minimized and new tax agencies should be formed to deal with various form of taxes. The most important is to replace custom wing of FBR by a port agency to deal taxes at import stage. On direct taxes, a new tax agency needs to be formed specializing in services income tax and should be independent of FBR.

Comments

Comments are closed.